In this week’s Fidelity Chart Room, Salman Ahmed, Global Head of Macro and Strategic Asset Allocation at Fidelity International, explores how central bankers seeking to deploy rate hikes in their battle against inflation risk triggering collateral damage as tighter monetary policy threatens to exacerbate already swollen debt servicing costs.

Inflation in advanced economies could be near its peak, and while it’s a matter of some debate, some of last year’s pandemic-produced price pressures could yet prove to be transitory. So what could be the downside for central bankers in taking away the punch bowl? This week’s Chart Room looks at the potentially painful sting that rate shocks could have on the cost of debt servicing for major economies.

Don’t do too little, too late

Inflation continues to surprise to the upside and shows no sign of peaking just yet. US data released on Thursday showed inflation in January accelerated to a 7.5 per cent annual rate, a four-decade high. But even if inflation in major economies does plateau in the near term, as some expect, its downward adjustment from here is likely to follow a long and sticky trajectory.

A more fundamental worry stalking markets and large swathes of the global economy, is that policy makers will under- or over-tighten policy given the delicate balance between growth and inflation, with large debt burdens constraining room for policy manoeuvre in the aftermath of the pandemic.

Take the US. Aggravated by spending to combat the pandemic, the US national debt last week surpassed $30 trillion for the first time, or nearly 130 per cent of GDP. This mountain of federal debt coupled with multidecade inflationary highs raises the prospect of systemic destabilisation that could spiral into a policy-induced slowdown for the global economy if the Fed and other major central banks tighten too aggressively.

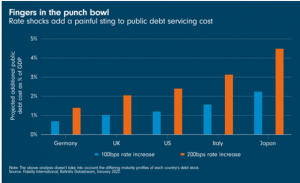

Don’t do too much, too soon

This systemic cost of hiking can be seen in this week’s chart. Our calculations suggest that, should the US policy rate rise by 200 basis points (two percentage points), the additional debt cost will amount to 2.4 per cent of gross domestic product. For Italy, the corresponding level of servicing would rise by 3 per cent of GDP. In Japan, such a move in its government bond yields would lead to an increase to its debt burden of around 4.5 per cent of GDP.

For policymakers, the trade-off spells pain both ways. An excess of tightening risks triggering problems of debt sustainability. A slower pace, however, could let macro excesses linger, though it would also allow inflation to lessen the debt burden over time. Striking the right balance is arguably going to be the biggest challenge policy makers face in this cycle.