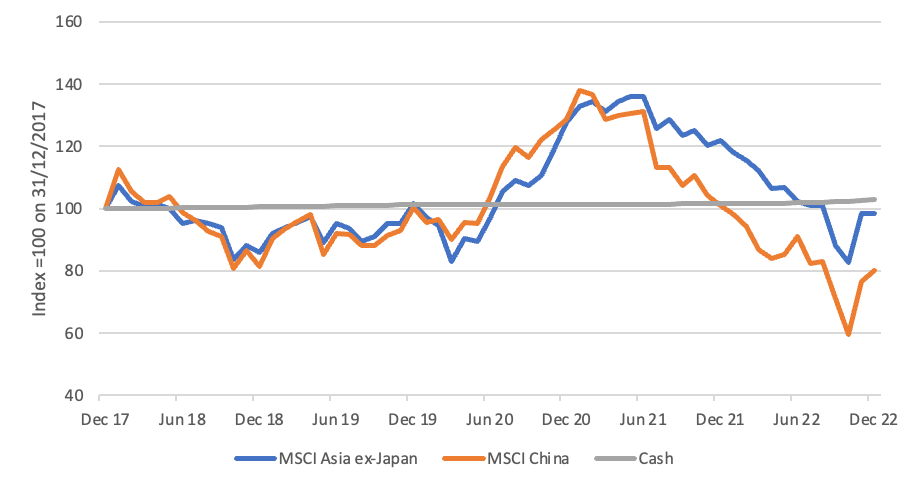

Investors may have been better off holding cash rather than buying shares in Chinese companies – but Chinese New Year could mark the beginning of a turnaround for the country and the wider continent, according to RBC Brewin Dolphin.

The wealth manager found that the MSCI China index has made a negative return of -19.83% since 2018, compared to +2.94%% from holding cash. The MSCI Asia excluding Japan index has performed better with a negative return of -1.69% but was still beaten by cash.

However, with China easing out of Zero-Covid restrictions and interest rates in the USA expected to peak this year – which typically has a knock-on effect for emerging market currencies and debt – there could be brighter skies on the horizon.

Janet Mui, head of market analysis at RBC Brewin Dolphin, said: “China has doubled down on a swift reopening, despite the first wave of Covid sweeping across the country. The impact on growth in the near-term is likely to be negative, as people become sick or shy away from going out.

“After better vaccination efforts and as more people gain immunity against the virus, economic activity from the second quarter is likely to rebound sharply. The overall direction is constructive, as China normalises which has important implications for the global economy.

“China’s reopening will provide incremental support to global growth at a time when major western economies are expected to be in recession. Asian countries with heavy tourism links with China may benefit as they embark on ‘revenge travelling’. The concern is that rising Chinese demand may drive commodity prices higher, which may lead to higher inflation in the West.

“Markets will remain sensitive to the progress of reopening in China. Chinese markets, in particular technology giants, have enjoyed a strong rally in the latter part of 2022 after a horrendous year. Short-term momentum in Chinese stocks is likely to remain positive as sentiment recovers and the government has pledged support on growth. But a lot of optimism has been reflected in the recent rally and valuations are no longer as cheap.

“The medium to longer-term picture is more ambiguous. We think investors are likely to remain concerned about the political, geopolitical, and regulatory implications after the cabinet reshuffle by President Xi at the National Party Congress.”

John Moore, senior investment manager at RBC Brewin Dolphin, said: “We tend to favour investing in funds that cover Asia or sub-regions within Asia, rather than specific nations. As we have seen over the past couple of years, China can be volatile and prone to government action, while currency fluctuations is another factor – particularly for some of the smaller Asian nations.

“A spread of investments is one of the best ways of mitigating against the risks associated with investing in emerging markets. A professional financial adviser will be able to guide you through the potential pitfalls and how much you should allocate to China or Asia within a balanced portfolio.”

Fidelity Asian Values – John Moore said: “The Fidelity Asian Values investment trust is managed by Nitan Bajaj and takes a contrarian/value approach to the region. At the same time, it prioritises good businesses run by good people, with a bias towards small and mid-cap companies. This approach has helped the trust to avoid some of the challenges of government intervention, which have affected larger technology companies and others. The China weighting is currently around 31%.”

Pacific Assets – John Moore said: “First Sentier managed, Pacific Assets Trust typically finds more opportunities in India – which represents nearly 50% of the trust – and southern Asia before Northern Asia and China, but has flexibility to change its focus as opportunities arise. The managers put a lot of emphasis on company stewardship, through a desire to have this mindset rather than treating it as a tick-box exercise. There are few well-known names among its holdings, with priority given to mid-sized companies that can compound returns and grow into tomorrow’s leaders.”

Schroder Oriental Income – John Moore said: “Schroder Oriental Income Fund, as the name suggests, is very much an income and large-cap play. Traditionally, it has been underweight China with, say, 10-15% weighting – but it has the scope to increase this should the opportunities arise. The fund is well spread by geography and investors will recognise most of the top 10 – Samsung, Telstra, BHP, and Taiwan Semiconductor Manufacturing Company (TSMC) included.”