Over the coming weeks, Schroders will be sharing its investment and market outlooks for 2023. From Sustainability to Private Assets, Schroders’ investment experts provide their forecasts for the year ahead.

Today, Sue Noffke, Head of UK Equities, and Andy Brough, Head of Pan-European Small and Mid Cap Team, explain how UK small and mid caps are currently pricing in a lot of bad news.

Sue Noffke, Head of UK Equities:

UK equities have been more resilient than many other world markets in 2022. This has occurred as inflation has hit multi-decade highs in the major economies such as the UK, US and Germany and interest rates have risen sharply. Equity investors showed a clear preference for the more international, largest FTSE 100 companies. Banks and the oil majors, for instance, have increased dividends and bought back considerable volumes of shares as strong commodity markets and rising interest rates have driven strong earnings growth.

Both sectors conduct much of their trade in US dollars, being the preferred currency of international commodity markets and international banking. The extraordinary run in the US currency has therefore been a further translational boost to their sterling earnings, and created even more financial headroom for these companies to return cash to their shareholders.

UK quoted small and mid cap equities (smids) have not had such a good year (see comment from my colleague Andy Brough, below) and this is piquing the interest of a variety of investors as they look to 2023. Price paid is one of the most important determinants of long-term investment returns and the current yield of around 3% offered by the FTSE 250 index – the most established group of UK quoted smids – speaks of mispriced opportunities not present at the start of 2022. Some of the domestically focused UK smids in particular look to be pricing in a lot of bad news. As a UK citizen it certainly feels like economics and politics are well below optimal at a time when our personal finances are being beaten up by inflation.

As an investor, however, I realise that it’s during the more challenging and uncomfortable periods that opportunities can be most plentiful. We’re a world away from the buoyant sentiment at the start of 2022. At that time the world was re-opening, money was flowing freely and a US investor had recently bought Morrison’s, the UK’s fourth largest supermarket, for £7 billion following a bidding war

So what of the opportunities now? We know that investing in smids over the long term can be very rewarding. They have a lower base from which to achieve growth, and if they can harness opportunities in a way which generates value for all stakeholders then the investment returns can be spectacular for the shareholder. Today, however, this strong growth potential is coming at a very attractive price. My colleagues across various investment teams at Schroders, whether they follow a “growth” or “value” style of investing, are seeing opportunities in the UK smids for a reason. I blend both styles and the portfolios run by me and my direct team are as exposed, or ‘overweight’ UK smids as we’ve ever been in 16 years running these funds.

Like me, my colleagues see opportunities in both the ‘domestics’ serving the UK consumer and business end user, and the many internationally focused smids. There is no silver bullet to the issues facing the UK economy, where more than 20% of the working age population is economically inactive. Valuations, however, are very beaten up and the market does not seem to be discerning between the good and less good companies.

We’re certainly wondering if some of the good smids might be vulnerable to bids should we see a resumption of inbound merger and acquisition (M&A) activity. US buyers paying in dollars continue to have a currency advantage, although higher interest rates make it harder to put together financing packages like that use to fund large deals for a FTSE 100 company in the mould of Morrison’s.

We are not complacent at a time when companies tell us they are now seeing inflation all the way through their supply chains, from transport costs to materials prices as well as higher wages. A very strong dollar has aggravated cost inflation for the domestics. Even the best companies are struggling to pass on their own higher transactional dollar costs to a UK consumer facing a cost of living crisis of historic proportions. There is certainty plenty to be fearful of economically, especially in Europe and the UK where the energy and cost of living crises seem likely to have already tipped, or will imminently tip, many economies into recession.

Higher interest rates could be a major issue for companies with high levels of borrowings, especially if that debt needs to be refinanced over the next 12 months. However, many of the best companies have made it through the pandemic and are well prepared to weather the storm ahead with the support of strong balance sheets.

It may come as a surprise, for instance, that FTSE 100 budget hotels group Whitbread is now enjoying yields on its rooms, or revenue per available room (RevPAR), well above pre-Covid levels. Supported by us and other investors who backed an emergency cash call in 2020 this domestic continued to invest during an extremely difficult period. It is now in a much better position to manage the supply chain constraints in the UK hospitality sector which are driving independent rivals out of business.

If Whitbread can be a leader in the UK, then it has the potential to be a leader on the wider stage too, and patient investors might also have an eye on German business. While currently loss-making, there is good scope to scale up these operations by taking share from struggling independent operators, which make up an even bigger part of the market in Germany.

And there are plenty of examples of smaller domestics with sufficient cash to grow their businesses and deliver good investment returns. Companion animal services specialist Pets at Home, for instance, has delivered consistent same store sales growth over the past five years. Reflective of this success Pets increased its full year dividend by 48% in the 2022 financial year.

A dividend yield around 4%, however, suggests investors may be putting too much emphasis on the short term cost inflation challenges currently facing the business. Also, it may not be as vulnerable to the squeeze on consumer spending as the market expects given the veterinary sector’s status as an essential service.

Looking ahead, the current challenges will eventually abate as inflation eventually eases and the forthcoming recession eventually passes. When this point in time comes into better view we expect the market to refocus on the long-term opportunities enjoyed by the business.

Looking at the bigger picture, we think it’s open to debate how companies and consumers react to this recession. Will businesses be as quick now to cut their workforce as in past recessions? The recent experience of skill shortages in a pandemic scarred economy and a structurally challenged labour market may cause them to pause. Will older cohorts dip further into their pandemic savings, now feeling that life is too short not to be enjoyed in the present? From the very gloomy point of where we stand today it might not take much to lift sentiment and valuations.

Conversely, should matters turn our worse than expected the dividend cover for UK equities is stronger than it has been for a decade, comfortably above two times (including for the FTSE 250). As the ratio of a market’s earnings over dividends, cover indicates the margin of safety to maintain dividends should earnings be cut more than expected during this recession. It is another important measure of financial resilience we’re looking at very carefully alongside balance sheet strength.

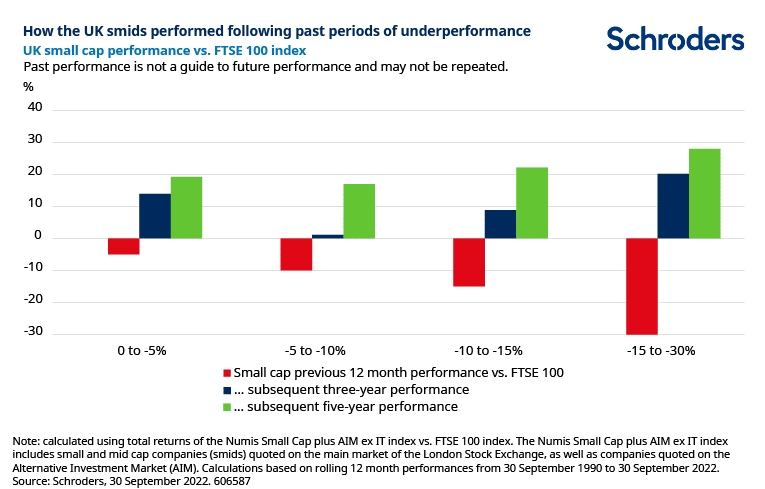

Andy Brough, Head of Pan-European Small and Mid Cap Team: The resilience of the broader UK equity market over the past year has masked a sharp underperformance from the small and mid cap equities (smids). The extent of the underperformance is rare in history, and in the past such periods have usually been followed by outperformance over three- to five-year time frames (see bar chart, below). UK quoted smids are home to many fast-growing companies in new and emerging industries whose valuations have come under intense pressure due to rising interest rates, akin to what we’ve seen happen with the US technology stocks this year.

These trends explain why the share price of a company such as hobby and crafting specialist Games Workshop has fallen by a quarter in 2022 (at the time of writing) despite it reporting another year of record results. The de-rating has been the result of a shift in market mindset alone. It should not deter investors who are best served focusing on the fundamentals which influence a company’s ability to grow profitably, make superior returns on capital and create economic and shareholder value.

The domestically exposed UK smids, or ‘domestics’, have been doubly exposed to rising rates, which are squeezing consumers already struggling to cope with inflation. The effect has been to further crimp discretionary spending on non-essential items such as clothing, holidays and meals out, negatively affecting the UK’s quoted retailers, travel and leisure companies and other sectors exposed to the domestic consumer. Meanwhile, many domestics (whether serving the consumer or business sectors) with supply chains overseas can’t get away from the impact of an exceptionally strong dollar on cost inflation.

Dollar strength has driven sharply higher import costs for all variety of sectors from consumer discretionary areas to manufacturing. These pressures have come at a time of unavoidably higher energy bills, increases in the national minimum wage, raw material price increases, freight cost increases and rising taxes increasing the cost of doing business in the UK.

In contrast, the internationally diversified large caps (82% of FTSE 100 revenues are derived from overseas markets versus 57% for the FTSE 250 – FTSE Russell, 30 September 2022) have benefited from the relative weakness of sterling to the dollar, and to a lesser extent the euro. On the positive, household energy costs have been capped easing fears around some UK consumer-focused areas of the market, and businesses have their own package to help get through the winter.

The future path of inflation and interest rates, and the potential depth and duration of the next recession, however, are all unknowable. And at a time when it might feel like the war against inflation in the UK is far from over, UK smids are not a particularly comfortable place to be.

Despite all these challenges, however, we’re more focussed on the degree to which bad news has already been priced in, and discerning between different companies with differing abilities to cope with the challenges ahead. In the travel and leisure sector reduced profitability could prove particularly problematic for equity investors as these companies have also had to issue new shares in order to shore up their balance sheets. This will have the effect of diluting returns for shareholders going forwards. But let’s not forget that the UK consumer is still spending, as confirmed by resilient results from luxury to sportswear retailer Frasers (recently promoted to the FTSE 100 from the FTSE 250), Pets at Home and Watches of Switzerland.

The latter’s luxury markets should enjoy strong long term growth and its Rolex business may prove particularly resilient during the recession. Resilience, however, is just half the story as the leading companies can capitalise in periods such as these, increasing their market share as less well equipped competitors struggle. And there are many UK smids out there to choose from.

UK quoted smids encompass more than 1,000 companies and that many may be less well-known than the FTSE 100 household names doesn’t mean they’re not world-leading companies capable of generating superior returns. There are plenty of these well-run businesses with market-leading positions in new and emerging industries from cyber security to fintech and data analytics – it’s just that the market is struggling to see them objectively at present.

The decline in the share prices of world leading companies such as Games Workshop suggest a lot of bad news is already factored into valuations. More broadly, the UK smids have fallen by 21% in the year to date (Numis Small Cap plus AIM ex IT (investment trusts) index to 30 November 2022, on a total return basis). In comparison, the FTSE 100 has returned more than 6% with the largest of its constituents perceived as safer propositions in a world of great uncertainty.

Over the past three decades, however, for UK smids to have underperformed to the extent they have in the past year is statistically rare. A period of strong outperformance versus the FTSE 100 has, usually, followed. And if we look at the period since 1999 the FTSE 250 ex IT index has risen almost six fold (from 31 December 1999 to 30 November 2022, on a total return basis), versus an equivalent near 150% total return from this FTSE 100.

Should we see a resumption of bids for cheap UK companies, mid cap companies can be the target of choice – not too big, but sufficiently large to make a difference for the acquirer. As companies are taken out it helps make room for the next tranche of exciting FTSE 250 companies (remember, only around 20 of the original constituents from 1999 are in the index today) helping to create a dynamism perhaps not there in other areas of the market.