By Katharine Neiss, chief European economist at PGIM Fixed Income

After a Covid-related delay, last week’s publication of the European Central Bank’s (ECB) monetary policy framework review arrived several months earlier than anticipated and to a less-than enthusiastic reception. The revised framework has naturally drawn comparisons to the Fed’s recently implemented strategy of flexible average inflation targeting (FAIT), thus the initial critiques have claimed that the ECB’s revised framework has not gone far enough to address the weak inflation that has plagued the euro area for more than a decade.

Yet, the resolve of European policymakers since the start of the pandemic should not be underestimated. The following outlines why we believe the revision is the appropriate one for Europe and the rationale behind the policy steps that may follow – possibly as soon as the ECB’s late-July policy meeting. Coupled with tailwinds provided by the recent rebound in activity and improving sentiment, such action could return inflation to target more quickly than expected. However, if significant action fails to materialise, the ECB may have opened a new window for participants to question its credibility and policy effectiveness.

When established best practice is radical

The ECB’s framework revision adopted established practice with a traditional 2% target – one that is symmetric and flexible over the medium term – hence underwhelming those calling for a regime similar to FAIT. Yet, the latter approach may be ill-suited for the challenges facing the ECB.

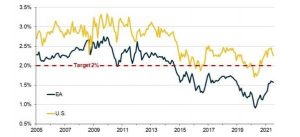

First, such a strategy requires market participants to form different inflation expectations depending on the time horizon – one over the near term and another over the medium term. For the Fed, this is a surmountable challenge as medium-term inflation expectations are well-anchored and rarely drop below 2%.

While euro area inflation expectations traded above 2% before the global and sovereign debt crises, they subsequently fell below 2% and were on a downward trend, reflecting a de-anchoring of inflation expectations in Europe (Figure 1). Furthermore, these expectations are increasingly influencing actual inflation outcomes given that the passthrough from wages to inflation has weakened in recent years.

Rather than a flexible average strategy that seeks to lift inflation expectations that have already de-anchored, the ECB’s Governing Council decided on a clear, fixed inflation anchor via a symmetric 2% target.

Second, given the scale and longevity of the euro area’s inflation undershoot, adopting FAIT would have implied inflation outturns of close to 3% over the next decade. Therefore, such a change could be viewed as implicitly raising the inflation target, a prospect that would be unlikely to garner consensus support among the Governing Council.

The new inflation target, alongside an explicit recognition of the asymmetry of monetary policy at the zero-lower bound, suggests a more radical shake up to ECB monetary policy. Given the Governing Council’s assessment that medium-term inflation is ‘well below’ its objective, the new framework points to comprehensive and sustained policy easing with a willingness to tolerate – if not target – inflation overshoots. While we’re encouraged by the ECB’s direction, its talk now needs to be backed by decisive policy action.