Ben Russon and Will Bradwell in Franklin Templeton’s UK Equity team provide their investment outlook for UK equities in 2022, covering key themes such as the economic recovery from COVID-19, inflation and the state of the consumer.

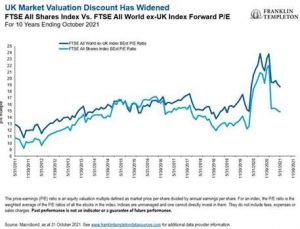

“Inflation, energy prices, interest rates, wage pressure, supply chains, COVID-19 third wave—there are a number of issues weighing on investor sentiment in the United Kingdom. However, we believe there are several positive indicators that counter these headwinds, such as a well-capitalised consumer with pent-up household savings, a sharp rise in initial public offerings (IPOs) and merger & acquisition (M&A) activity, and attractive valuations compared to the rest of the world.

“As we move past what is likely the most acute stage of the COVID-19 pandemic, the second-order effects of this recovery are beginning to cause concern for investors.

“Stagflation (high levels of inflation but low economic growth) has become a potential scenario. As economies have reopened, supply-chain bottlenecks and rising commodity prices have caused pockets of severe inflation (such as used car prices rising 18.3% year on year)1 as supply has not been able to keep up with excessive demand. In the United Kingdom, rising energy prices are likely to drive inflation higher into next year.

“A specific point of contention is the increase in the energy price cap in spring 2022, which could see energy prices rise by 30%-40%, adding as much as 1% to inflation. We see this, along with higher levels of taxation through national insurance contributions, as examples of how the potential exit rate of growth from the pandemic may not be fully achieved.

“Labour costs are undoubtedly the greatest challenge to our view of inflation. The unemployment rate at 4.5% (as of August 2021) is testament to the effectiveness of government policy during the pandemic, but we remain vigilant as to how the employment backdrop evolves going into 2022 as the furlough scheme is wound down.

“Amid firming prices, central banks globally have taken a more hawkish tone, though this may not translate into policy changes. The Bank of England (BoE) has a somewhat different policy framework than the US Federal Reserve (Fed) and European Central Bank (ECB). The Fed and ECB target an average rate of inflation of 2% over the cycle, whereas the BoE targets an explicit 2% level, making it more justifiable to raise interest rates in the United Kingdom. As of October 2021, the market-implied base rate a year forward is around 80 basis points, from a current level of just 10 basis points. With UK gross domestic product 3% below its pre-pandemic peak, and with a raft of fiscal tightening measures on the horizon, we see considerable risk that simultaneous monetary tightening may derail any further recovery.