AJ Bell’s latest Dividend Dashboard report shows:

- Aggregate dividend forecasts for the FTSE 100 in 2024 and 2025 are holding firm, even if they leave 2018’s all-time high of £85.2 billion just out of reach

- Analysts expect 1% dividend growth in 2024 to £78.6 billion before a 7% increase in 2025 to £83.9 billion

- FTSE 100 firms have already unveiled plans for £49.9 billion in share buybacks in 2024, after £52 billion in 2023, with £3 billion in special dividends from HSBC on top

- Add in £11 billion of forecast dividends from the FTSE 250 and £47.2 billion of live or completed takeover offers and the FTSE 350 is offering £189.7 billion in total cash returns (dividends plus buybacks plus takeovers) on its £2.5 trillion market capitalisation, for a ‘cash yield’ of 7.7%

- That figure compares very favourably to the 5.00% Bank of England base rate, the 10-year gilt yield of 3.92% and the prevailing rate of inflation of 2.2%, based on the consumer price index

AJ Bell’s investment director Russ Mould comments:

“Any investor who sold in May, went away, and came back on St Leger day did not miss much, but they did not accrue any great benefit either, even allowing for August’s brief stock market squall. The FTSE 100 has broadly gone sideways, having set a new all-time high in May, as investors have considered the implications of the general election result and a move to lower interest rates from the Bank of England as the UK has tried to pull out of the shallow recession which characterised the second half of 2023.

“Equity and bond markets in the West are still embracing the narrative that inflation will cool, economies will enjoy a soft landing (if any landing at all) and that central bank interest rate cuts will support asset valuations and output alike. Any divergence from that path could lead to increased volatility and some doubts regarding the health of the US economy are creeping in, especially as it feels overdue a downturn, given that the last one (with the exception of 2020’s pandemic panic) was 2008. Much may depend on the outcome of November’s US presidential election, although the reality is that candidates often find it easier to make promises than to squeeze legislation through Congress.

“China, the world’s second-biggest economy, is not providing much by way of additional economic impetus, while its third, Japan, is raising interest rates and not cutting them. The fourth biggest is Germany and that is going nowhere fast after four negative quarters of GDP growth in the past seven.

“Any marked deterioration in the US could have an additional impact and this may help to explain why profit and dividend forecasts for the FTSE 100 are flat to down.

“Aggregate dividend estimates for the FTSE 100 are unchanged at £78.6 billion and £83.9 billion for this year and next, based on consensus analysts’ forecasts for all the index’s members.

Source: Company accounts, Marketscreener, consensus analysts’ forecasts. Ordinary dividends only.

“That still leaves the FTSE 100 on a forward dividend yield of 3.7% for 2024 and 4.0% for 2025, based on ordinary dividend payments. HSBC is offering a special dividend, FTSE 100 firms are buying back stock at a rapid clip and takeover activity across the UK equity market is also putting cash back into investors’ pockets, even if some deals have fallen by the wayside and some feature an element of stock in the offer price.

“This matters, if you believe the old adage that bull markets only end when the money runs out, because investors are currently receiving more in cash than they are being asked to pay out, given the relative paucity of new floats and the limited number of big cash raisings. Data from the London Stock Exchange group states that companies had tapped investors for just £10.2 billion as of the end of July, via either primary or secondary offerings.

Slump in profit forecasts continues

“Analysts are still expecting a new all-time high for aggregate FTSE 100 pre-tax profits in 2024, at £237.3 billion, 4% less than the £247.4 billion expected three months ago. Downgrades at oils and miners cover nearly all of the £10.1 billion downgrade, thanks to lower commodity prices, amid renewed, but as yet unsubstantiated, fears of a harder-than-expected economic landing. A further 8% improvement is expected in 2025, to another fresh peak of £257.3 billion when healthcare is expected to be a key source of earnings growth, alongside more cyclical elements such as mining, industrials and beneficiaries of consumer discretionary spending, such as retailers and travel and leisure companies.

Source: Company accounts, Marketscreener, consensus analysts’ forecasts.

“This defensive contribution from healthcare could be valuable if GDP growth proves hard to come by, but for the moment company boardrooms seem confident in the outlook and that record profits will indeed continue to flow. No fewer than 43 current members of the UK’s elite stock market index have already sanctioned share buyback programmes in 2024, compared to 42 across the whole of 2023 and 45 in 2022.

“The value of the buybacks announced in 2024 stands at £49.9 billion, to perhaps give the FTSE 100 a platform for a crack at 2022’s all-time high of £58.2 billion, or at least 2023’s total of £52.1 billion, with three months still to go.

“Such bumper returns supplement dividend payments. Add together ordinary dividends, special dividends and buybacks and FTSE 100 firms are expected by analysts to return £131.5 billion to their shareholders in 2024 and £85.7 billion in 2025. The all-time high figure was £137.5 billion in 2022.

Source: Company accounts, Marketscreener, consensus analysts’ forecasts. Ordinary dividends only. *Announced in aggregate as of 19 September.

“Merger and acquisition activity is also boosting investor returns and shining a spotlight on how the UK equity market may be cheap after a long period in the doldrums. Four FTSE 100 firms, DS Smith, Rightmove, Hargreaves Lansdown and Darktrace, are the current target of bids, with the approach for the last-named closing at the end of September, when trading in its shares ceased. A fifth member, miner Anglo American, fended off a bid from BHP and a sixth name, non-life insurer Hiscox, has been the subject of a rumoured approach, although that has yet to materialise.

“Add in the forecast £11.0 billion in dividends from the FTSE 250 and £47.2 billion in successful or ‘live’ takeover offers and investors could be set for a £189.7 billion inflow from the FTSE 350 overall in 2024, thanks to the combination of dividends, buybacks and takeovers. That figure equates to 7.7% of the FTSE 350’s current £2.5 trillion market valuation, a ‘cash yield’ which compares favourably to the 5.00% Bank of England base rate, the 3.92% yield on a 10-year UK government gilt and the 2.2% headline rate of inflation.

Concentration of dividend growth a potential risk

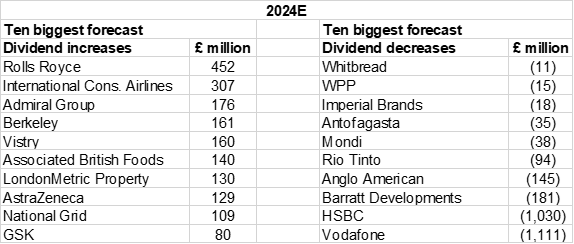

“The FTSE 100 forms the bedrock of those figures and investors must be aware of the relative degree of concentration risk within the UK’s headline index. Just 10 companies are forecast to pay out 55% of the total for 2024, at £42.9 billion, while the top 20 are expected to chip in £56.0 billion, or 71%, of the total.

“The top 10 list includes two oil majors, drug developers, banks and consumer staples players, and one apiece from the mining and utility sectors. This again highlights the importance of the miners, oils and financials to the overall trajectory of the FTSE 100’s profits and dividends.

“Vodafone’s well-trailered, £1 billion-plus dividend cut for 2024 weighs heavily and the biggest forecast increases, expected to come from International Consolidated Airlines, Rolls-Royce and Admiral, pale by comparison. The forecast drop in HSBC’s payment is not a cut, but the result of a lower share count (thanks to buybacks) and currency movements and buybacks account for a few of the very modest reductions expected by analysts. At least this provides a better spread to the modest anticipated increase in dividends from the index in 2024 and helps to reduce concentration risk to some degree.

Source: Company accounts, Marketscreener, consensus analysts’ forecasts. Ordinary dividends only.

Dividend cover expected to fall to lowest since pandemic in 2024 but remains solid

“At least dividend cover may provide some sort of buffer against any unexpectedly hard economic landing. Dividend cover is much better than it was ahead of the mid-cycle growth bump of 2015-2016 that promoted a rash of dividend cuts and, for that matter, the entire stretch from 2014 to 2020 when earnings never once covered payouts by a factor of two or more.

“As a result, shareholder distributions may not be quite the same hostage to fortune that they proved to be in 2016, or 2020, should there be another nasty surprise awaiting the economy and markets in 2024 or 2025. It also seems reasonable to assume that share buyback programmes will be halted before dividends are cut.

Source: Company accounts, Marketscreener, consensus analysts’ forecasts.

“That said, forecasts for the aggregate earnings cover ratio for the FTSE 100 are moving lower, as profit forecasts slip and estimates for dividend payments hold firm. Cover in 2024 is expected to come in at 2.07 times according to analysts’ consensus earnings and dividend forecasts. This is down from the 2.57 times on offer in 2022 and would be the lowest outturn since the Covid-affected year of 2020.

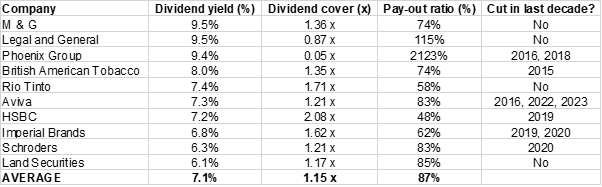

Many dividend yields compare well to gilts

“At the time of writing, the fund manager M&G is the highest-yielding stock in the FTSE 100, followed by the life insurers Legal & General and Phoenix Group, with British American Tobacco and Rio Tinto next on the list.

“BAT has never cut its dividend and can even point to a streak of increases in its annual dividend payment that stretches back to 1998. The fat yield at the tobacco giant may raise the question of whether that streak is about to end, even if its cashflow remains robust, and the firm is even cannily selling assets in India to buttress its finances.

“There have been 137 dividend cuts across the current crop of FTSE 100 members in the past decade and even if 74 of those came in the Covid-blighted years of 2020 and 2021 there were still eight in 2023. There are 10 more on the cards for 2024, if analysts’ forecasts are correct.

“As such nothing can be taken for granted and investors need to look at the balance sheet and cash flow – and not just the profit and loss account and earnings cover – when assessing how safe a dividend may be. They will also need to assess the volatility of profits and, in the case of cyclical stocks whose earnings and cash flow are subject to the vagaries of the economic cycle, look at average earnings over a full cycle to see what degree of cover that provides.

Source: Company accounts, Marketscreener, consensus analysts’ forecasts, LSEG Datastream data. Ordinary dividends only.

“A further rule of thumb states that any dividend yield which exceeds the risk-free rate by a factor of two may turn out to be too good to be true. The 10-year gilt yield is a good proxy for the risk-free rate. A dozen years of interest rates at near zero rendered the rule pretty useless but now monetary policy is returning to something akin to ‘normal’ it may regain some of its former relevance.

“For the record, just four FTSE 100 firms currently offer a forecast dividend yield of 7.8% or more, or twice the 3.92% 10-year gilt yield that prevails at the time of writing.”

DIVIDEND DASHBOARD EXPLAINED

Each quarter, AJ Bell takes the forecasts for the FTSE 100 companies from all the leading City analysts and aggregates them to provide the dividend outlook for each company and the entire index. The data relates to the outlook for 2024 and in some cases 2025. Data correct as of 19 September 2024.