Now we have something new to worry about, because real pay (after inflation) is falling. In the three months from November to January, after inflation, total pay is up 0.1%, but regular pay is down 1% (inflation over the three months averaged 4.8%). Falling real wages is nothing new, we lived through 12 months of it after the financial crisis. However, falling real wages at a time of rising inflation and enormous pressure on the cost of essentials is going to put huge pressure on those whose finances were already close to the edge.”

6) Lockdown savings are being eaten into

Sarah Coles, Senior Personal Finance Analyst at Hargreaves Lansdown:

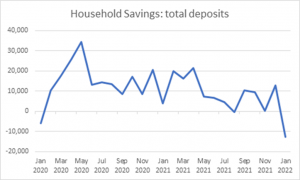

“Overall the pandemic has seen millions of us build up savings, with £278.8 billion added to the coffers between February 2020 and January 2022. The trend was most striking early in the pandemic and during subsequent lockdowns, and peaked in May 2020 when £34.4 billion was squirrelled away in a single month. In more recent months, savings have tailed off, and in January we actually ate into savings. We may well be moving into a period where higher prices mean people are forced to spend their lockdown savings.

Of course, throughout the past two years, people’s experiences have varied dramatically. While some people were able to work from home and cut their costs to build up savings, others lost work and ended up borrowing to make ends meet. A survey by the FCA in February last year found that while 26% of people had saved more money, 34% had eaten into any savings that they had. Anyone whose financial resilience has taken a battering during the pandemic faces horrible challenges now that prices are rising ahead of pay again.”

7) Annuity rates are on the increase

Helen Morrissey, Senior Pensions and Retirement Analyst at Hargreaves Lansdown:

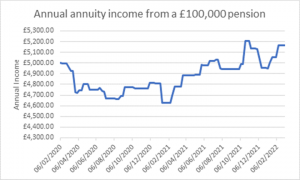

“Two years ago, concerns about a possible no-deal Brexit and worries about the scale and severity of the COVID outbreak sent long-term gilt yields crashing. As these yields are a major factor in determining annuity rates, we saw the income you can get from an annuity following a similar downward trajectory. In March 2020 a 65-year-old retiring with a £100,000 pension would only receive around £4,700 per year from a single life level annuity.

However, since then rates have been on the increase and the same person purchasing an annuity today can expect to receive closer to £5,200 per year. If we see further interest rate rises throughout the year, we could well see annuity incomes rise further. While these increases are no doubt welcome it is worth bearing in mind, they are coming off the back of near-historic lows. The incomes generated from annuities today still pale in comparison with what could have been purchased before the Global Financial Crisis for instance.”