Momentum across precious metals gathered pace this week as markets increasingly price a return to U.S. Federal Reserve easing. While recent data still point to a broadly resilient U.S. economy, pockets of softness—most notably in the labour market—have sharpened attention on the upcoming jobs report. For gold and silver, a lower-rates backdrop is supportive, and geopolitical uncertainty is adding an additional layer of demand.

Recent inflation prints and sentiment surveys suggest the U.S. economy remains on reasonably firm footing. Even so, markets are now positioned for the Fed to begin cutting rates this month. The magnitude of easing will hinge on data over the next couple of weeks, with non-farm payrolls and unemployment front and centre. For non-yielding assets like gold and silver, falling real yields are a tailwind.

Gold: policy support meets geopolitical hedging

Beyond rates, lingering geopolitical risks—from Middle East tensions to tariff uncertainty—continue to underpin strategic demand for gold. Technically, gold has broken out from a multi-week consolidation. The move above the widely watched $3,400 level (after several failed attempts) has shifted the near-term bias higher. With spot now eyeing the $3,500 area—just shy of record territory—a sustained close above resistance would confirm upside momentum. Failure there could invite a pause as dip-buyers and late entrants tussle for control.

Key watch points for gold

- Follow-through above ~$3,500 to confirm the breakout.

- U.S. jobs data and any fresh guidance on the Fed’s path.

- Headline risk around tariffs, geopolitics, and Fed governance.

Silver: a cyclical squeeze on top of the precious-metals bid

Silver’s surge to $40/oz—its highest since 2011—reflects both the rates-driven bid for precious metals and genuine supply-demand tightness. On the demand side, expanding use in technology, EVs and AI-related hardware has lifted industrial consumption. On the supply side, mine output has struggled to keep pace, and long lead times for new projects limit near-term relief. That combination has amplified price responsiveness as investors rotate into the complex.

Why silver’s set-up stands out

- Structural demand from electrification and AI hardware.

- Constrained supply and slow project pipelines.

- Sentiment spillover from gold as rate-cut odds rise.

Policy risk: Fed independence and the dollar

Markets are also parsing a more contentious policy landscape. Debates around Fed independence—alongside personnel headlines—have mapped onto rates and the dollar: softer front-end yields on perceived near-term cuts, but stickier long-end yields as investors price inflation and governance risk premia. For gold, that mix typically resonates as a “there is no alternative” (TINA-style) hedge.

The evolving legal scrutiny of proposed U.S. tariffs adds another layer of uncertainty. A material rollback would likely be risk-positive—potentially pressuring gold and supporting Treasuries and equities as trade frictions ease. Until clarity emerges, though, prolonged uncertainty tends to keep a safety bid under precious metals and complicate the dollar’s path.

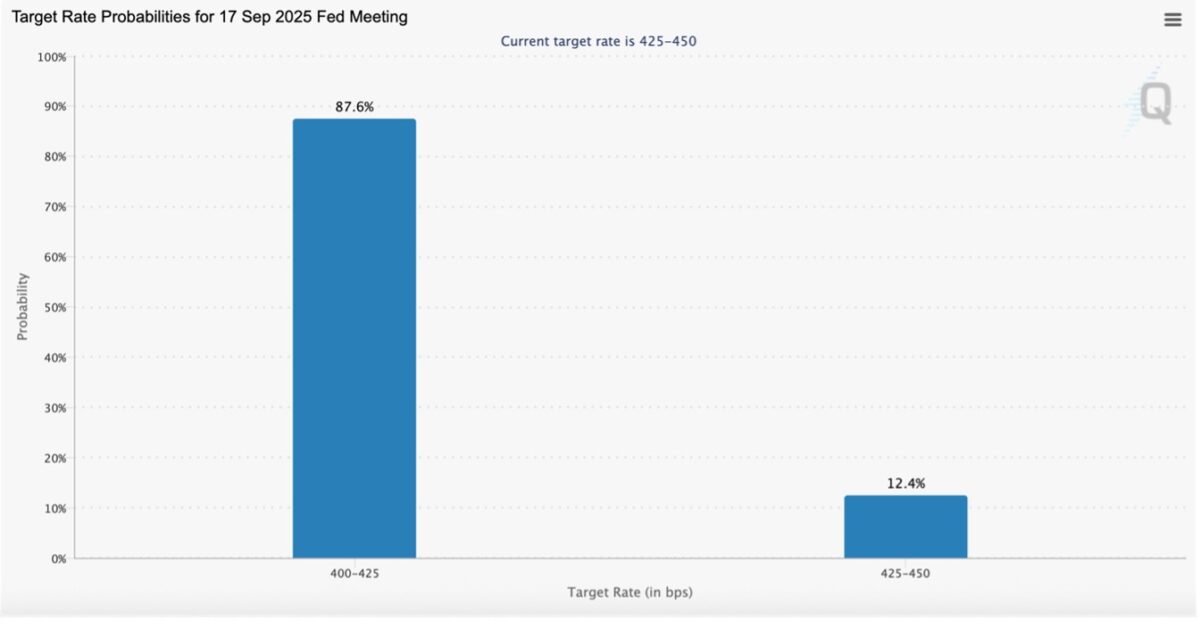

Market-implied odds point to a high probability of a September rate cut, with the pace thereafter contingent on labour data. Last month’s softer headline and downward revisions rattled confidence in the “strong labour market” narrative; consensus now looks for roughly ~75k jobs in August and a modest uptick in the unemployment rate. In the near term, an inline print probably preserves the easing trajectory; a significant miss could accelerate expectations for additional cuts.

Equities and earnings: strong, but priced for perfection

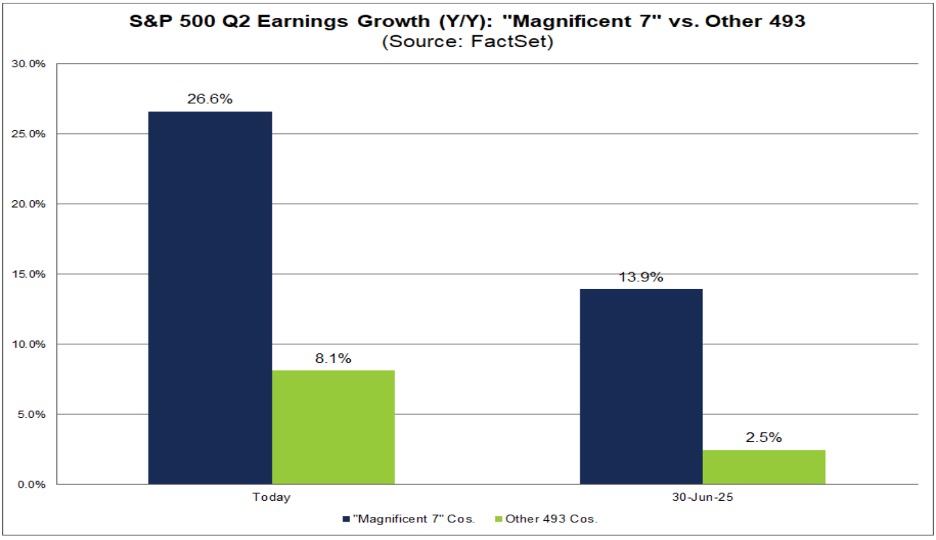

U.S. earnings season delivered broad double-digit growth. The “Magnificent Seven” posted ~26% year-on-year gains, while the remaining S&P 493 advanced ~14%. Yet valuations are stretched: forward P/Es have retraced to levels seen before the last correction, leaving equities sensitive to disappointment. Nvidia’s recent results illustrate the point—solid beats on most metrics met with a cautious reaction amid questions around data-centre growth and the China outlook.

Nvidia as a bellwether

- Short-term: momentum is moderating; $185 is a bullish break level, while $165 is a support zone to watch.

- Medium-term: China is largely excluded from current guidance; any reopening of that channel would be upside optionality not fully reflected in the tape.

Bottom line

- Gold: Breakout bias with $3,500 the near-term pivot; supported by falling real yields and geopolitical hedging.

- Silver: Tight fundamentals magnify the rates-driven tailwind; momentum strong but prone to squeezes in both directions.

- Rates & Dollar: High odds of a September cut; labour data will steer the path beyond. Governance and tariff headlines inject risk premia.

- Equities: Earnings solid but valuations rich; sensitivity to macro and policy surprises remains elevated.

By Daniela Sabin Hathorn, senior market analysts at Capital.com