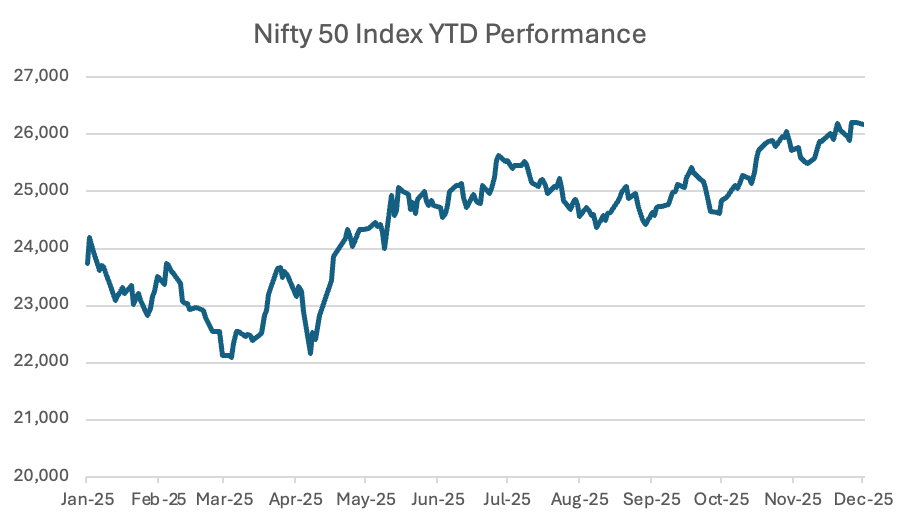

India is heading into 2026 with momentum building. After the early months of this year were shaped by a continuation of 2024’s post-election correction, amplified by US tariff shocks and geopolitical tension, the market has staged a decisive, sustained recovery through the better part of 2025.

Domestic reforms, resilient consumption, and improving earnings have helped the Nifty 50 reclaim lost ground and return to all-time highs. Foreign investors are now beginning to re-engage as valuations recalibrate and macro uncertainty looks set to ease.

Source: Bloomberg as of 01/12/25

With key headwinds fading, the outlook for the next 12 months looks meaningfully stronger. Against this backdrop, there are four key dynamics we expect to shape India’s equity market in 2026…

1) Resolution of US Tariff Negotiations

The most significant external drag on India this year has without doubt been the nation’s ongoing tariff dispute with the United States. The imposition of import duties of up to 50% in August, higher even than the levy on China, has added uncertainty and weighed on international demand.

But we view this as transitionary.

For one thing, India’s trade secretary has stated publicly that he expects a deal before year-end and President Trump recently confirmed that discussions are progressing well.

More to the point, though, the US needs India far more than current tariffs imply.

Beyond India’s political role as a counterweight to China and Russia, Indian talent and supply chains are embedded across the US economy – from tech platforms like Amazon and Microsoft to major financial institutions.

Realistically, this makes a 50% tariff rate difficult to sustain, and we expect a negotiated move back toward a more normalised 15–16% range.

Renewed optimism can already be seen in the latest figures, with India’s US exports jumping 14.5% between September and October, their first rise in five months. Getting a deal over the line would ensure this is sustained, easing uncertainty for exporters and restore visibility for earnings models that were disrupted this year.

2) Continuing Domestic Economic Momentum

India’s domestic economy continues to play an important role in India’s growth model.

With roughly 60% of GDP driven by consumption, the government has meaningful capacity to support growth when global conditions turn uncertain. Faced with the US tariff shock, policymakers have made great use of this in 2025.

The combination of income tax cuts in March and significant reductions in Goods and Services Tax in September has had rapid, visible impact. Indian households are feeling wealthier and pent-up discretionary spending has been released after two years of subdued growth. Rising credit expansion and a re-acceleration in government expenditure have amplified these effects.

The Nifty 50’s return to all-time highs and the recent news that the Indian economy posted its fastest growth in six quarters in the July-September period are two visible markers. Another is the re-emergence of corporate profitability from cyclical lows, signalling the early stages of an earnings upturn.

Crucially, much of the stimulus introduced in 2025 will flow through the economy gradually.

S&P Global Ratings is already projecting 6.5% economic growth for India in the current fiscal year and 6.7% in the next. But with additional fiscal and labour reforms recently announced, and more expected, we wouldn’t be surprised to see the country surprise on the upside.

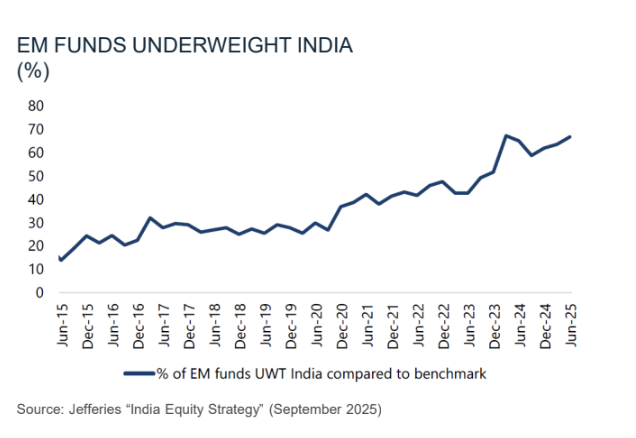

3) A reversal of long-term foreign outflows

Since 2018, foreign institutional investors have cumulatively sold roughly $30 billion of Indian equities.

The outflows have been driven by a combination of concerns over valuations and shifting allocations towards China. And this year, they’ve contributed to a rare period of underperformance for India relative to wider emerging markets.

But this dynamic now looks stretched.

Close to two-thirds of EM funds are now underweight India. And with domestic investors continuing to buy steadily, a structural imbalance has emerged, with FII ownership now at a 13-year low of 17%.

We believe a turning point has begun to emerge.

The compression in valuations through 2024–25, combined with improving earnings visibility, is already prompting foreign investors to re-evaluate their stance. Outflows have begun to slow in recent months, and several months of net inflows throughout the year suggest sentiment is shifting.

Foreign inflows/outflows into India over the past 14 months (Source: Reuters)

A successful resolution to US-India tariff negotiations could accelerate this reversal. In that scenario, 2026 could see FIIs become consistent net buyers rather than periodic sellers, marking an important tailwind for the nation’s stocks.

4) Meaningful Valuation Re-ratings Across Key Sectors

The broad de-rating seen during the period of foreign selling has resulted in valuations in several of India’s growth sectors moving below their historical averages.

These opportunities are most visible in areas where penetration remains low and structural growth is high; in particular, private sector banks, residential real estate developers, and consumer-tech platforms.

Within this group, companies we see as high-quality have delivered strong operational performance yet continue to trade below their long-term median valuations.

For example, recent data suggests that Godrej Properties’s latest performance trends have coincided with increased urban housing demand and a rise in project launches. Industry sources suggest that Swiggy remains one of the major leading participants in food delivery and quick commerce. Likewise, Kotak Bank is currently trading at valuation levels below some historical averages.

These businesses are gaining share in markets that are far from saturation. As foreign outflows slow and domestic liquidity remains robust, we see scope for sustained outperformance – not only in 2026, but across a multi-year horizon as penetration increases and earnings compound.

A Market Positioned for Upside

After a period of adjustment, India enters 2026 with strengthening domestic demand, improving earnings visibility, normalising valuations, and the prospect of foreign outflows slowing.

With external risks easing and reforms gaining traction, the opportunity set for long-term equity investors is arguably the most compelling it has been in several years.

Andy Draycott is portfolio manager of the Chikara Indian Subcontinent Fund