The defining story of the week was a historic rout in software stocks, triggered by fears that AI will disrupt rather than enhance the sector. The software industry suffered its worst week since April last year and its worst relative performance since the tech bubble burst 25 years ago.

Many leading software stocks were punished as though they are no longer relevant in the AI age. The catalyst was AI startup Anthropic’s release of new tools designed to automate work tasks across industries, from legal and data services to financial research. This reignited concerns that AI could bypass traditional software altogether.

The key risks are twofold. First, AI-driven efficiency threatens the user-based pricing models that underpin much of the sector if fewer employees are required. Second, AI makes it easier for firms to build their own internal workflows, potentially reducing reliance on third-party software. While there will inevitably be winners and losers, particularly where specialised software and deep data moats exist, the current sell-off has been widespread and indiscriminate. That is unlikely to persist as the market begins to differentiate.

AI-related concerns erased approximately $300bn of market value from software firms on Tuesday alone. The contagion spread beyond pure software into the broader tech complex and even into private credit stocks that lend heavily to software companies.

Despite this, broader equity markets proved resilient. Global equities closed the week up 0.7%, with defensive and cyclical sectors, as well as smaller companies, performing well. Consumer staples led the way, rising 6.5%, as investors rotated toward steadier cash flows and more attractive valuations.

US manufacturing gets a boost while labour market concerns rise

The January ISM Manufacturing PMI smashed expectations, rebounding sharply to 52.6 from 47.9 in December and marking the first expansion in a year. The scale of the surprise coincides with a major fiscal shift: the reopening of the 100% bonus depreciation window under the “One Big Beautiful Bill”.

Immediate full expensing has materially improved the economics of capital investment, encouraging manufacturers to pull forward spending plans. This fiscal impulse is now feeding through to the survey data and raises the likelihood that stronger activity will begin to appear in the hard data over coming months.

In contrast, the labour market painted a far less reassuring picture. Challenger, Gray & Christmas reported that US employers announced over 108k job cuts in January, the highest figure for the month since the Global Financial Crisis. This represents a 118% year-on-year increase and a 205% rise from December. Hiring intentions also fell 13% from a year earlier, the weakest January reading since 2009.

ADP employment data was also softer than expected. Both series are volatile, and attention now turns to the official Bureau of Labor Statistics release later this week.

Commodities and currencies

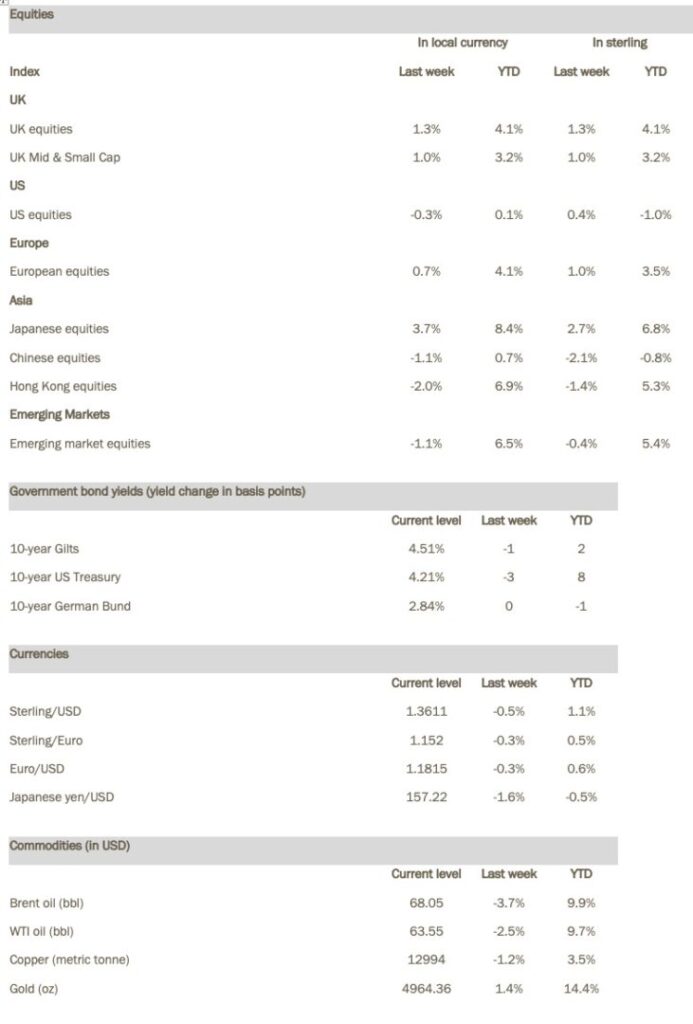

Treasury Secretary Scott Bessent cited Chinese traders as a key driver of recent volatility in precious metals, describing the moves as a “classical, speculative blow-off”. In another volatile week, gold ended slightly below $5000, up 1.4%, while silver finished at $78/oz, a return of -1.8% for the week.

The dollar posted its first weekly gain since early January, supported by haven demand amid the software-led turmoil. The yen, typically another haven currency, fell sharply, touching 157 versus the dollar as markets priced in a decisive election victory for Japanese Prime Minister Sanae Takaichi. Her win delivers a two-thirds majority and grants her mandate for an expansionary policy agenda. Japanese equities have rallied in response, while the yen’s reaction has so far been relatively muted.

The week ahead

Wednesday: US labour market data

This is a crucial report given the weakness shown in the private data last week. It will be a difficult report to decipher given the technical adjustments being made this month however expect job growth at 69k for January with the unemployment rate remaining at 4.4%.

Thursday: UK GDP

Economists expect growth to remain tepid but steady at 0.2% in the fourth quarter. With the budget now behind us and the Bank of England having cut rates there is a good chance that activity picks up a little this year. That said it’s hard to get too excited about the UK which still faces a long-term productivity challenge.

Friday: US Consumer Price Index inflation

US inflation is expected to slow to 2.5% although there are conflicting pressures under the bonnet. Truflation, a private data set that tracks over a million real prices, sees inflation falling below 1% while the Adobe Digital Price Index is expected to show particularly high goods inflation.

by Tom Hibbert, Chief Investment Strategist, Canaccord Wealth