BullionVault’s Adrian Ash looks back at the performance of gold throughout conflict. Adrian reflects on the performance of gold during certain world events, leading up to today’s conflict in Iran.

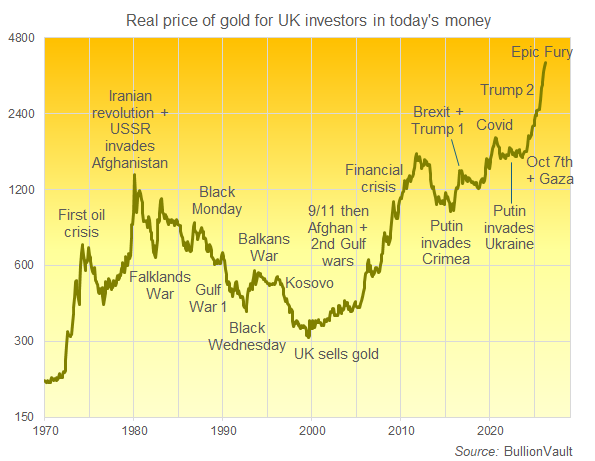

Look at gold’s real price for UK investors across the last 50 years and a stark pattern appears. Gold tends to revalue when the world becomes more dangerous, more unstable or less predictable.

The first dramatic surge came in the 1970s. Oil shocks, the Iranian revolution and the Soviet invasion of Afghanistan shattered confidence in economic stability and sent gold sharply higher in real terms.

Prices cooled through the 1980s and 1990s as inflation fell and the Cold War ended. But gold’s role as crisis insurance reasserted itself after the 9/11 attacks and the wars that followed. The real turning point for modern investors was the global financial crisis, when confidence in banks and the financial system evaporated almost overnight. That moment reminded investors why gold exists in portfolios in the first place.

Since then, the shocks have come thick and fast. Brexit, the pandemic, Russia’s invasion of Ukraine and now renewed tensions involving Iran have kept geopolitical risk firmly on investors’ radar. The uncomfortable truth the chart highlights is that gold’s strongest periods tend to coincide with moments when the global outlook is deteriorating. In other words, gold does best when the world looks its most fragile.

What the latest tensions around Iran underline is investors are once again confronting the possibility of wider geopolitical disruption, higher energy prices and renewed inflation risks. When several of those pressures appear at once, geopolitics, inflation and economic uncertainty, gold historically doesn’t just rise. It reprices.

For UK investors, the long-term message is that gold isn’t about chasing returns in calm markets. It’s about holding something that tends to come into its own precisely when confidence in everything else is under strain.