Emerging markets are navigating a material supply-side shock following the escalation of conflict in the Middle East, which has disrupted energy flows, increased geopolitical strain and pushed up prices. Against this backdrop, long-term investors will need to look beyond the immediate noise and focus on the fundamental forces shaping markets over time.

Fidelity International’s 2026 Analyst Survey*, offers that lens, drawing on global, on-the-ground insights to identify the sector and regional dynamics driving long-term investment prospects.

The survey captures insights from more than 120 equities and fixed income analysts, based on over 20,000 meetings with company management teams worldwide.

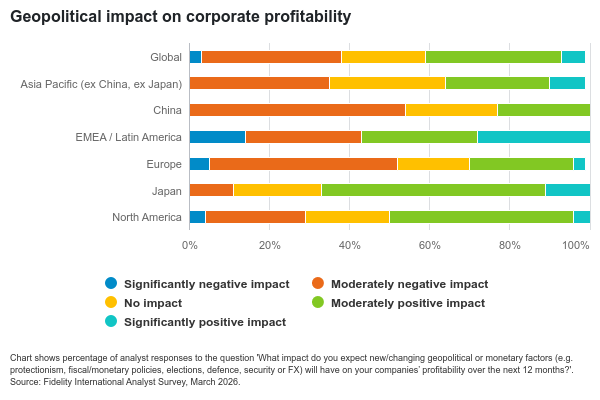

Geopolitical shocks remain a headwind

Unsurprisingly, analysts covering Europe and parts of Asia increasingly expect geopolitical or monetary factors to weigh on corporate profitability over the next 12 months. Europe appears particularly exposed, with most analysts expecting a moderately or significantly negative impact, and a notable share anticipating a significantly negative outcome. Asia Pacific (ex China and Japan) shows a similar pattern, with negative impact expectations exceeding positive responses.

China analysts also remain cautious, with 54% expecting a moderately or significantly negative impact on profitability.

By contrast, EMEA and Latin America show a more polarised picture, with analysts expecting both significantly positive and significantly negative impacts on profitability. This reflects the diversity of the region, where some countries and sectors are exposed to policy and demand risks, while others, particularly resource-linked economies and companies, may benefit from higher commodity and energy prices.

In addition, nearly two-thirds of analysts say they continue to factor shifting trade policies into their fundamental analysis, underscoring the lingering impact of last year’s tariff shocks.

Niamh Brodie-Machura, CIO, Equities at Fidelity International comments: “Geopolitical developments are again influencing the outlook for emerging markets, both directly through trade and policy uncertainty, and indirectly via energy prices and inflation. The sharp moves in energy markets are adding a new layer of complexity, particularly for regions more exposed to energy supply shocks. While a stabilisation could ease near-term volatility, the balance of risks has shifted toward a more prolonged disruption, intensifying inflationary pressures, particularly for energy-importing economies.”

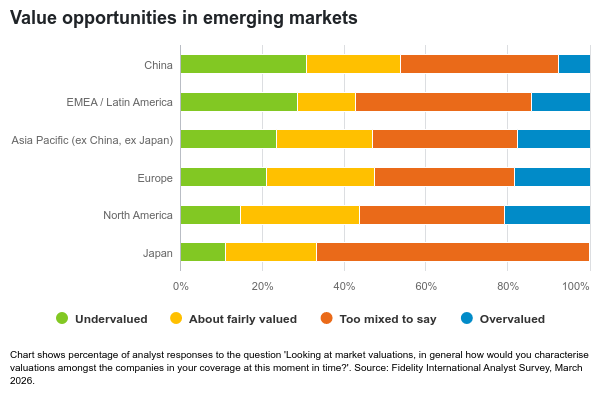

Diverging performance expectations

In this context, sentiment toward equity performance remains differentiated rather than uniformly negative.

Of China analysts, 31% see their sector as ‘undervalued’, the highest across the world and compared with 24% in Asia ex Japan/ex China, and 29% in EMEA/Latin America.

China’s innovation drive

China remains central to the emerging market story, although higher energy import costs and renewed supply chain disruptions are adding near term pressure. Other structural growth drivers continue to support the long-term outlook.

Policymakers continue to prioritise high-tech industries to strengthen self-reliance, supporting growth in electric vehicles, artificial intelligence, biotechnology and robotics.

Local semiconductor equipment manufacturers are benefiting from domestic capacity expansion and supply chain localisation. In biotech, analysts note faster development timelines and lower costs relative to Western peers.

Consumer demand, however, remains uneven. Housing weakness and deflationary pressures persist, though analysts see opportunities at both the premium and value ends of the market.

No common outcome

The duration of Middle East tensions remains a key variable. Prolonged disruption could intensify inflationary pressures and weigh more heavily on energy importers.

At the same time, structural growth drivers and reform momentum are creating increasingly differentiated outcomes.

Niamh Brodie-Machura added: “What stands out from the survey is the degree of divergence within emerging markets. Differences in reform momentum, energy exposure and innovation capacity are leading to increasingly varied corporate outcomes. In this environment, treating emerging markets as a single asset class is less effective – disciplined, bottom-up country and stock selection is becoming more important.”

Important information

This document is classified as a Marketing Communication as defined by the Guidelines on marketing communications under the Regulation on cross-border distribution of funds (ESMA34-45-1272).

This material is for Investment Professionals only, and should not be relied upon by private investors.

The value of investments and the income from them can go down as well as up so you/the client may get back less than you/they invest.

Investors should note that the views expressed may no longer be current and may have already been acted upon.

Overseas investments will be affected by movements in currency exchange rates.

Investments in emerging markets can be more volatile than other more developed markets.