As gold falls in price, Sara Niven, manager of the aberdeen Global Balanced Growth Fund, has shared her thoughts.

“In the aberdeen Global Balanced Growth Fund, we consider gold as a core allocation* as it provides diversification to the two largest risk exposures in our portfolio: equity and duration. In recent years, gold has benefited from a structural shift in central bank demand, the debasement trade, questions around Fed independence and renewed private sector demand for uncorrelated assets. This support has allowed gold to trend nicely above the 100-day moving average since late 2023; that is, until recently.

“The escalation of conflict involving the US, Israel, and Iran coincided with a loss of momentum in gold. With the bounce in oil prices, rates have repriced higher and the dollar has strengthened; both are negative for gold. Additionally, there has been isolated speculation (notably around Turkey) that some central banks could mobilise gold reserves for liquidity. These factors emerged when gold was trading 25% above its 200-day moving average, so a reversal from stretched levels of some magnitude was not a surprise.

“With gold now down nearly 20% from the start of the conflict, the entry point is becoming more attractive as we believe the longer-term drivers are still intact. Since Q4 2025, we have reduced the fund’s gold allocation on strength, moving from 9% at the end of September 2025 to 5% as of February 2026. Although valuation looks better, the initial impact of the conflict has been tighter financial conditions, and as a result, we think it is premature to add to our exposure.”

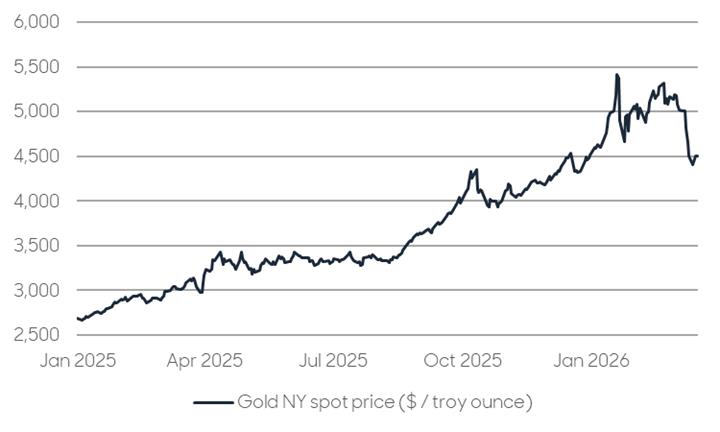

Gold prices have given up their gains YTD

Source: Aberdeen, Factset, March 2026

*5.3% allocation to gold as at 28 February 2026. For further details, see factsheet here.