Data and culture, underpinned by rigorous governance and controls, are now critical enablers of scale for driving value for consolidators, according to NextWealth’s Consolidation of Advice Report 2026 (CAR 2026).

The report identifies four distinct operating models shaping acquisition strategies – Provider-backed, PE scale-led, PE optimisation-led and HNW-focused – each with their own key characteristics and non-negotiable approaches when it comes to integration, adviser autonomy, data infrastructure and growth, highlighting the lack of a single route to scale.

Data and culture in the front seat

Cultural alignment, the hardest factor to systemise, is shown to be consistently cited as a cause of failed acquisitions. Firms will make assumptions based on informal sense-check measures during the deal process and treat that as either key indicators of alignment or a red flag – such as how a CEO responds when their processes are questioned, whether they lead with valuation expectations in early conversations, and how they speak about their clients and staff.

Meanwhile, poor data quality is stopping deals even getting off the ground. Firms complete individual client-level analysis before making offers, using this to build the integration plan in parallel with the commercial assessment. Where acquisition targets are unable to produce data to evidence their claims, firms may walk away.

CAR 2026, which provides an in-depth examination of M&A activity in the UK financial advice market from Q1 2021 to Q1 2026, explores the forces shaping acquisition decisions and defines acquirers not by deal count or assets, but by the strategic choices they make around integration, proposition control, data infrastructure, and growth.

Drawing on interviews with acquiring firms and private equity investors, the report also shows how private equity ownership is maturing, why integration quality has become the defining competitive differentiator, and what consolidation means for platforms, asset managers, and technology providers who serve this market.

The key take-away for CAR 2026 is that data, underpinned by the right culture and strong governance, is needed to validate and achieve scale, which ultimately drive value – no matter the consolidator’s operating model. These factors have always mattered, according to NextWealth, but acquirers now apply a systematised process to ensure good outcomes for advisers and clients as the FCA continues to scrutinise consolidation. Due diligence on the business to be acquired is a structured process with clearly defined criteria, not a qualitative assessment made late in the deal.

Understanding the operating models shaping consolidation

CAR 2026 examines how operating models can be grouped by the consolidators’ approach to integration, proposition control, data accessibility and growth strategy. From this it has identified four distinct models – Provider-backed, PE scale-led, PE optimisation-led and HNW-focused.

While the ability to evidence client outcomes, maintain high-quality data and effective integration are consistent across the board, each model has its own non-negotiables and diverge on their approach and importance given to key factors. Specifically, how deeply and quickly they integrate acquired businesses, how much control they assert over proposition, platform and investment, adviser autonomy, strategic partnerships, how reliable and developed their data and governance infrastructure is, and what role acquisition plays within the acquirers’ broader growth ambitions.

“We examined the acquisition, technology, and investment proposition strategies currently employed by 30 leading acquirers. What we found was that the era of buying advice firms simply for scale is well and truly over. Today’s acquirers must prove they can integrate, govern, and grow their businesses organically to survive the next phase of consolidation,” explains NextWealth Consulting Director, Emma Napier.

Napier adds that the first wave of PE investment during the early 2020s, which pushed firms to scale as fast as possible, has been replaced by more considered approaches: “In 2026, firms measure success against the value created, which has been executed against the business plan. Some of the firms previously prioritised pace of acquisition over integration discipline are feeling the pressure now. It is no wonder, therefore, that the quality of a target firm’s data and cultural fit have become key acquisition considerations. They cut across almost every acquisition decision. Meanwhile, the importance of data hygiene and management cannot be overstated. We found that many acquirers screen target firms on the quality of data well before even making an offer. Notably, some firms go so far as to start to integrate data before deals are signed,” says Napier.

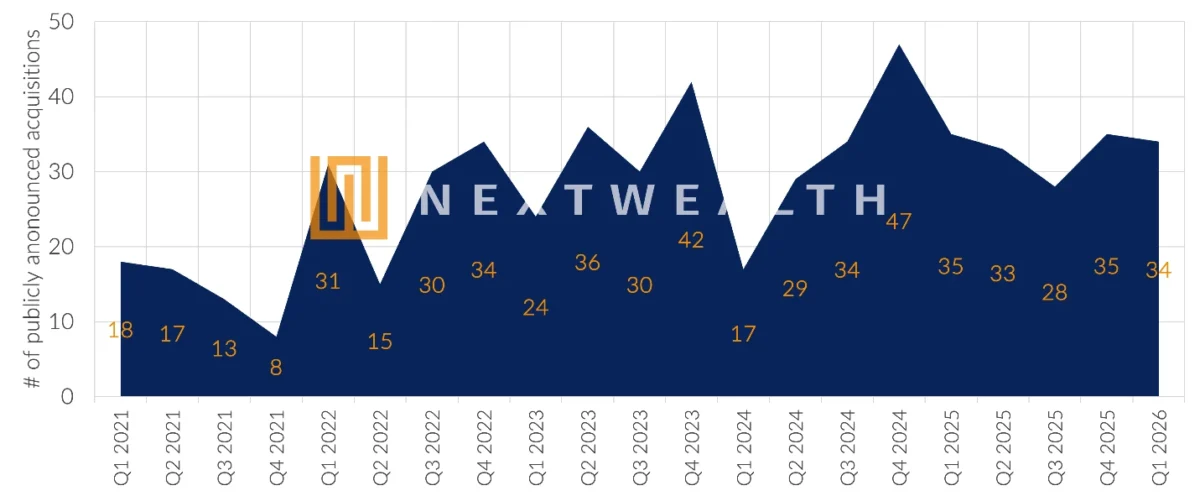

M&A activity in the UK advice space in 2025 was in line over the last three years and early 2026 activity suggests momentum continues. “The momentum is still there, it’s just that acquirers are more deliberate than they once were, they’re clearer about the model they are building and the role acquisitions play within it,” says Napier. “The market is no longer defined simply by how many deals happen, but by who is doing them. A small number of firms account for a large share of acquisitions, but new entrants from adjacent market sectors are broadening the buyer pool, and that means more exit routes for sellers.”

Number of deals per quarter

The market remains active, but it is increasingly concentrated, says Napier, and a small group of firms is setting the pace, but they are not all doing it the same way.

For further information, visit the NextWealth report webpage.