Andy Draycott, Portfolio Manager of the Chikara Indian Subcontinent Fund, shares his insights on the market situation in India. Market selloffs don’t just reset valuations. In the right conditions, they also accelerate competitive change.

In India today, higher oil prices, foreign outflows and geopolitical uncertainty continue to weigh on sentiment, even as the structural case for a growing pool of high-quality businesses remains intact.

Historically, periods of stress in India may have created short-term pain for some but they have also helped quality companies widen their advantage.

But the opportunity is not simply in buying lower valuations, it’s in identifying the businesses best placed to strengthen their position through the drawdown.

Securing a leading position

The opportunity from hereon in starts with India’s market structure.

Many of the country’s most attractive sectors remain underpenetrated, but they’re also consolidating. That combination is powerful. There’s still substantial room for category growth, while an increasing share of the profit pool is being captured by a smaller group of dominant private-sector players.

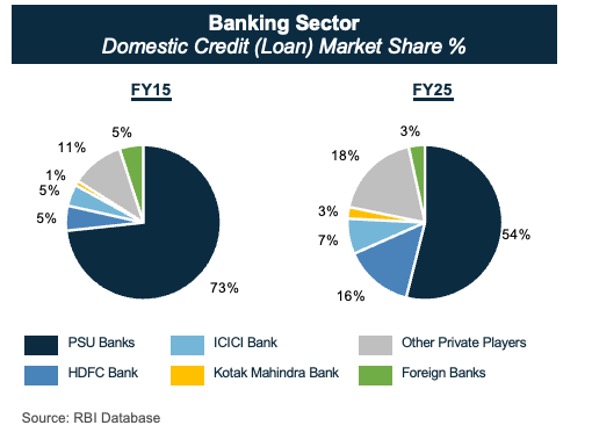

Three examples are used to illustrate this dynamic. .[1]In banking, public-sector banks have lost around 20% of domestic credit share over the last decade, while the top three private banks alone now account for 26%. (See chart below)

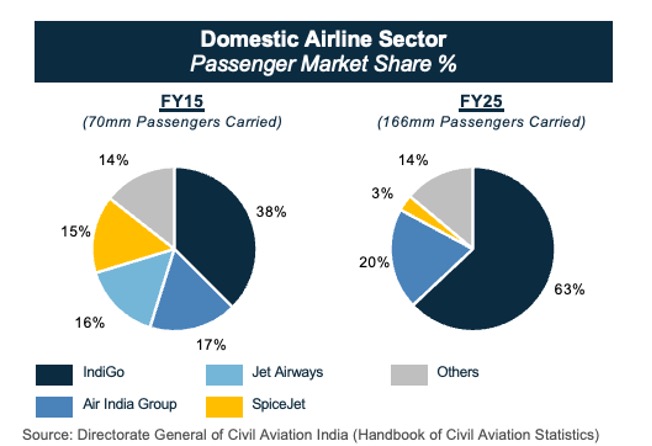

In aviation, IndiGo’s domestic passenger share has risen from 38% in FY15 to 63% in FY25. (See chart below)

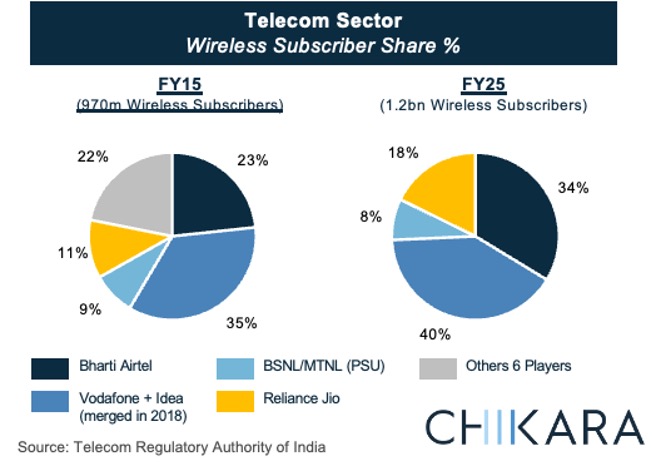

And in telecoms, a market that once had 12 operators has effectively become one with three private players and one state-backed entity. (See chart below)

These shifts show how pricing pressure, regulation, capital intensity and technological change have steadily pushed market share towards the best-capitalised and best-run operators.

At the same time, these three sectors are still far from mature.

India’s domestic airline market, for example, carried 70 million passengers in FY15. By FY25, that had risen to 166 million.

In other words, consolidation is happening inside markets that are still expanding rapidly.

These aren’t stagnant industries where consolidation simply protects incumbents; these are situations where leaders can gain share while the market itself continues to widen.

And that’s why today’s period of dislocation is so interesting.

When weaker competitors are forced to retrench, business transformations that might otherwise take years can happen much faster. The funding backdrop tightens, balance sheet strength matters more, and companies with net cash, established brands and operational scale can continue to invest while others are forced to defend their position.

In sectors like those mentioned above, India’s strongest franchises could exit this period with larger market shares, stronger pricing power and a bigger claim on future profit pools.

In today’s environment, broad market exposure can only get investors so far. The bigger prize lies in identifying which businesses are most likely to consolidate share as conditions become more difficult.

The benefits of an active approach

For investors, the key takeaway is not just that India has become cheaper. It’s that this sell-off may be offering access to a set of businesses whose long-term positions are improving at the same time valuations are resetting.

That’s where active management can really add value. In markets where weaker competitors are under pressure and stronger operators can keep gaining share, the most attractive opportunities are often found not in buying the whole market, but in identifying the companies whose future earnings power may be strengthening beneath the volatility.

Andy Draycott is portfolio manager of the Chikara Indian Subcontinent Fund

[1] [1] All charts and figures taken from webinar and slides in this piece