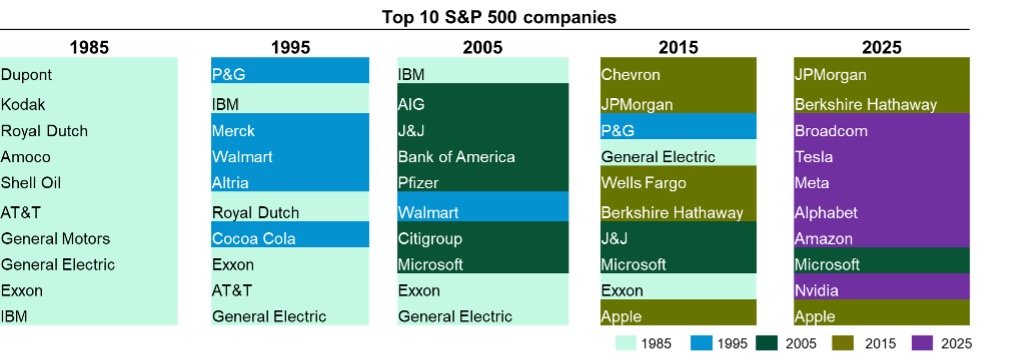

Ask equity investors about their mega-cap concentration today and most will acknowledge it. What they tend to be less certain about is how their overall portfolio would fare if market leadership shifted. Nisha Thakrar, Product Specialist at Nedgroup Investments, shares her insights.

Owning the same winners has been easy up to now. Just look at the €73bn of inflows into passive global equity core strategies over the past twelve months (funds and ETFs), or the €323bn held in actively managed, growth-heavy global equity portfolios, according to Morningstar.

They all point in the same direction, and the amplification has worked in investors’ favour because diversification has not yet been tested. Arguably the biggest risk investors face today is that diversification fails when it is needed most.

As markets continue their narrow streak, investors should look beyond surface level sector and manager diversification, and revisit it in terms of earnings drivers and behaviours.

This way, when leadership shifts (as it inevitably will) portfolios have exposures that can genuinely diverge. Here is where contrarian investing comes in.

The branding problem

If contrarian investing is to play that role, it must overcome its perception problem.

Being different for the sake of being different, ‘value’ dressed up in disguise, seen as being an approach driven by emotion, bold conviction and heroic timing, or simply a strategy suited only to crises, such perceptions explain why it remains under-utilised in portfolios that otherwise seek diversification.

Buying away from the crowd at low prices and selling high is foundational, but insufficient on its own.

To play a role across cycles, contrarian investing must be repeatable and grounded in process.

It rests on two non-negotiable principles, which are behavioural discipline (or comfort with discomfort) and deep fundamental research. This is because to act differently, you need to know something different.

Acting differently, knowing something different

As the US-Iran conflict unfolded in March 2026, equity markets turned negative across every sector except energy.

For many investors, this was a moment to step back. We took it as a moment to act on the back of multi-year, deep fundamental research, where the market had formed a decisively different view from our own valuations. The names we bought sit away from AI and, therefore, away from investors’ minds, but they serve essential, enduring needs.

These include healthcare equipment and infrastructure providers such as Baxter and ICON; the specialty chemicals value chain, including IMCD, Azelis and Nippon Paint; and food-related businesses such as Sodexo and The Magnum Ice Cream Company. All possess strong competitive positioning, resilient earnings, a pathway to growth and undemanding valuations in the low teens.

Notably, the conviction to act does not start with, or depend solely on, cheapness. It is rooted in long-term temperament – developed through cycles of being early, wrong and patient. This temperament drives a culture that prioritises deep research while scrutinising downside risk with equal rigour, free from the pressure of market noise, and ultimately enables buying in periods of uncertainty.

Selling should mirror buying.

In 2024, when the market refocused on Netflix’s pricing power, accelerated subscription growth following a period of losses, and viewed its substantial content spend as a moat rather than cost, expectations reset quickly.

As an investment, the stock no longer offered a sufficient margin of safety and, crucially, the valuation had run its course, so we exited. What had not changed was the quality of the business or our view of management. The decision was anchored in valuation, just like the original purchase.

A role beyond market stress

Contrarian investing’s relevance extends beyond periods of stress. The increasingly short-term nature of markets – particularly reactions to quarterly earnings – continues to create an abundant opportunity set for long-term investors seeking mispriced and misunderstood businesses.

For example, as valuations have soared for the mega-cap companies we have owned, selling has followed the same discipline as in Netflix, releasing capital to be put to work elsewhere. Given our flexibility across geographies and market capitalisations, we have redeployed that capital into mid-cap businesses where coverage is thinner and mispricing more persistent.

This can create a structural advantage for the contrarian investor. An investor willing to be comfortable with discomfort, equipped with the resources to conduct deep fundamental research.

How to spot a contrarian investor

Below are four indicators to help identify whether a strategy is genuinely contrarian.

| Contrarian measure | What to look for |

| Active share | Typically above 80%, below 60% may indicate index-aware positioning.Beware: high active share does not guarantee outperformance. |

| Tracking error | Higher tracking error reflects a willingness to diverge and be early as contrarian investors often buy when others are selling. |

| Valuation multiples | Portfolios should trade at a discount to the index over time, reflecting disciplined entry and exit. |

| Positioning in unloved areas | Meaningful exposure to out-of-favour sectors, geographies or stocks where sentiment is weak whether due to a consensus negative outlook from sell-side research or a de-rating as investors pursue higher growth areas. |

Taken together, these signals help answer the question that matters most when evaluating any manager claiming to be contrarian: is the discomfort genuine, or merely labelled as such?

In a market where many portfolios still lean on the same winners, getting that distinction right matters more than it has for some time.

1 As at 30 April 2026. Source: Morningstar

Nisha Thakrar

Nisha joined Nedgroup Investments in 2023 and is the Product Specialist for the Nedgroup Investments Contrarian Value Equity fund. She has more than two decades of experience engaging with retail and institutional clients across asset class. Nisha was previously at Capital Group, where she was an investment specialist for the multi-asset solutions business, senior manager of the product development team in Europe and held various other roles. She also spent three years at Fidelity International, where she was latterly a pricing analyst.