As inflation, energy costs and shifting priorities reshape spending habits, a ‘K-shaped’ consumer economy is emerging. It’s one where higher and lower-income households are moving in very different directions.

In this update, Charles French, Chief Investment Officer (Listed Equities) at Impax Asset Management, explores what this divergence means for investors and the sectors he believes are set to benefit.

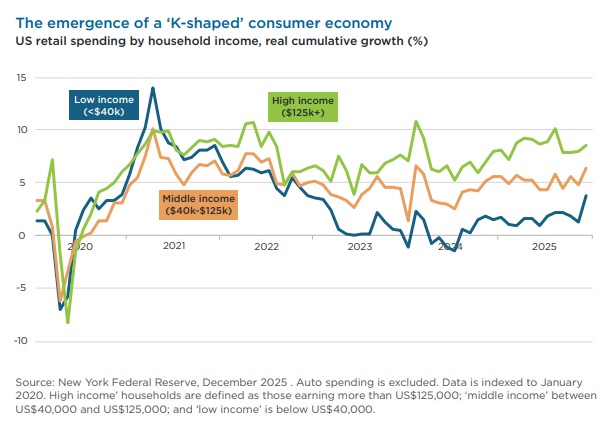

In early 2026, we have observed profound structural shifts in consumer behaviour, with spending generally shifting towards more services and experiences. There has also been the emergence of a ‘K-shaped’ economy, with the spending patterns of high and low-income cohorts diverging (see chart below).

The global consumer has proven more resilient than some headlines would indicate. We believe this trend is likely to continue, unless oil prices rise significantly further. Patterns of consumption continue to evolve, however: the post-pandemic recovery has matured into a period of selective consumption, where households prioritise value, experiences and differentiation over volume. We believe elevated energy prices and persistent inflation have reinforced these behaviours, rather than driving a broad-based retrenchment.

The latest energy shock is reshaping the consumption landscape in three ways

1.) Energy as a behavioural driver, not just a cost.

Higher, more volatile energy prices accelerate consumer interest in energy efficiency, electrification and cost-saving technologies. A clear example is electric vehicles (EVs), whose sales have surged as consumers reassess their economic competitiveness. Monthly EV sales in Europe topped 0.5mn for the first time this March as fuel prices soared.15 The rising competitiveness of EVs supports opportunities for suppliers of advanced driving systems (like Aptiv), leading battery-makers (like CATL) and EV producers themselves (like Rivian).

2.) Inflation fatigue, not capitulation.

Consumer spending continues, despite real incomes continuing to come under pressure in many regions, but with increased brand selectivity and a focus on value. Following years of raising prices, and with widening adoption of appetitesuppressing GLP-1 drugs leading to falling volumes, companies such as PepsiCo are reducing prices.16 This trend could be a positive turning point for nutritional ingredients companies (like Symrise) that help reformulate packaged foods. Meanwhile, we believe new dietary guidelines from the US government create a positive environment for high-quality protein providers (such as Norwegian salmon producers Lerøy and Bakkafrost, market-leading fresh produce suppliers (like Dole).

3.) Greater dispersion across income cohorts and regions.

Higher-income consumers, and those in more energy-insulated regions, continue to spend and invest – albeit at the expense of savings in the US.17 At the lower end of the ‘K’-shaped economy, where the cost-of-living squeeze is felt more acutely, consumers are prioritising spending and downsizing. Nonetheless, there are still companies benefitting from the transition to a more sustainable economy.

We note sustained demand for activities and consumer goods that support healthier lifestyles (such as premium running shoes, made by the likes of ON Holdings) as well as the prioritisation of ‘essential’ services, like insurance. Despite uneven consumption patterns in China, for example, robust demand for health and retirement protection products (from the likes of Ping An) demonstrates consumer will still invest in their financial security.

The current dynamic of rising energy, inflation and potentially higher-for-longer interest rates means these trends are unlikely, in our view, to revert in the near term. Persistently higher energy costs, uneven fiscal capacity across regions and accelerating technological disruption suggest that dispersion in consumption outcomes is likely to remain a defining feature of markets.