Inflows of £1.5 billion were recorded in April, a slight increase on March’s £1.3 billion and a sixth consecutive month of inflows, according to data published today by the Investment Association (IA).

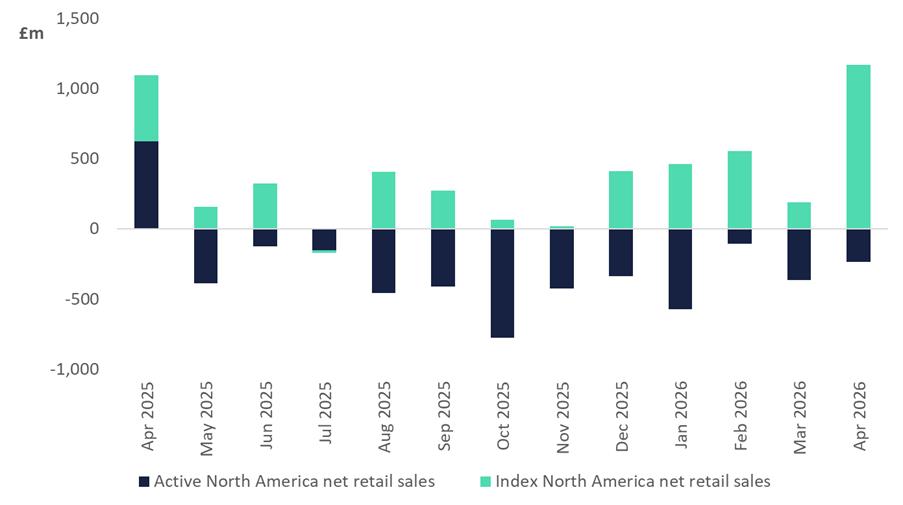

Equity outflows narrowed sharply to -£689 million from -£1.3 billion in March. Investors returning to equities did so predominantly through index trackers, with equity tracker funds drawing inflows of £1.7 billion against active equity outflows of -£2.4 billion. North American equities led inflows, attracting £860 million, the strongest monthly inflow since April 2025.

This return coincided with a robust US earnings season, with Alphabet, Meta, Amazon and Nvidia all exceeding expectations, supported by continued investment in artificial intelligence.

In contrast, money market funds recorded their first outflow since August 2025. £755 million was withdrawn following sustained demand for short term, low risk assets in the early months of the year, as investors used money market funds as a temporary home for their capital in a time of significant market uncertainty.

Money market funds saw record inflows (£2.01 billion) in March as the outbreak of conflict in the Middle East threatened global energy supplies and sparked inflation concerns. April’s money market fund outflows suggest some of this capital could be driving the shift back into equities, even as the broader outlook remains uncertain.

Key findings for April 2026

- Equity fund outflows narrowed to -£689 million, an improvement on March’s -£1.3 billion. North America was the standout, with inflows of £860 million, the strongest since April 2025. In contrast, UK equities saw outflows of -£673 million, with Global Emerging Markets returning to outflows of -£477 million, Asia (-£399 million) and Europe (-£244 million) also saw net outflows.

- Index Tracker funds attracted inflows of £1.8 billion, while active funds saw outflows of -£331 million. Modest headline outflows from active funds mask heavier redemptions of -£2.4 billion from active equity.

- Active equity outflows totalled -£2.4 billion against equity tracker inflows of £1.7 billion, up from £797 million in March.

- Money market funds turned to outflows of -£755 million, the first outflow since August 2025, with Short-Term Money Market the worst-selling sector in April.

- Fixed income returned to inflows of £466 million, reversing March’s outflow of -£966 million. Mixed Bond was the most popular fixed income category with inflows of £373 million, followed by Sterling Corporate Bonds (£85 million) and Sterling High Yield (£79 million). UK Gilts saw a modest inflow of £67 million, while Government Bonds recorded continued outflows of -£147 million.

- Mixed asset funds recorded strong inflows of £1.8 billion, up from £1.1 billion in March, with £341 million flowing into the 40-85% Shares sector, as demand for diversified strategies remained strong.

- Across other sectors, Volatility Managed had a strong month with inflows of £607 million – the second highest monthly figure ever recorded, behind only the £887 million seen in February 2020.

- Targeted Absolute Return saw outflows of -£114 million, reversing three consecutive months of inflows.

- Responsible investment funds saw outflows of -£381 million, a slight improvement on March, including -£423 million from SDR-labelled funds.

April inflows points to early signs of improved investor sentiment towards the US

Slowing equity outflows in April suggest a tempered return to equities as market performance has remained robust even in the face of the Iran conflict and the effective closure of the Strait of Hormuz. This appetite has been led by inflows into index tracking equities (£1.7 billion), concentrated to North American equity trackers (£1.2 billion).

A strong US earnings season and continued investment in artificial intelligence reinforced confidence. The first inflows into the Technology and Technology Innovation sector in seven months of £96 million also point to a renewed interest.

Outside North America, the demand for equities was weaker. Equity regions of Europe (-£244 million), the UK (-£673 million) and Asia (-£399 million) all posted outflows, reflective of both lower exposure to = artificial intelligence stocks and greater vulnerability to energy and fossil fuel price pressures.

Actively managed and index tracking net retail sales to the North America sector, April 2025 – April 2026

Miranda Seath, Director, Market Insight & Fund Sectors at the Investment Association, said:

“Six months of consecutive inflows is a meaningful signal that retail investors have not been shaken from their long-term plans, even as the investment landscape has remained far from straightforward.

“What’s particularly striking this month is the shift out of money market funds. For much of the past year, investors have been holding capital in short-term cash-like assets, understandably so, given the level of uncertainty in markets. The fact that we are now seeing that money begin to move is an encouraging sign that investors are starting to feel more confident in the investment outlook, particularly for the US following a strong month of North American equity inflows

“The question now is whether this momentum into North American equities broadens out, or whether geopolitical uncertainty keeps risk appetite contained.”