In this issue of the “IBKR Economic Landscape” from José Torres, Senior Economist at Interactive Brokers, José discusses how climbing yields are threatening to end the nine-day equity winning streak, as heightened geopolitical tensions, tariff uncertainties, and robust economic metrics lift inflation expectations.

Crude is jumping amid ongoing Middle East violence, with the tenuous ceasefire at risk of falling apart, which would further sustain oil prices. Additionally, he dives into US ADP-Jobs and ISM-Services reports and offers an international roundup.

Climbing yields threaten to end 9-Day winning streak for stocks

Climbing yields are threatening to end the nine-day equity winning streak on Wednesday, as heightening geopolitical tensions, tariff uncertainties, and robust economic metrics lift inflation expectations. Crude is jumping amid ongoing Middle East violence, with the tenuous ceasefire at risk of falling apart, which would further sustain oil prices.

On the cross-border commerce front, President Trump has proposed reinstating his protectionist trade policy by proposing new duties starting at 10% across 60 nations. Wednesday morning’s data didn’t offer any relief for Treasurys either, with hiring hitting a 16-month high, exceeding forecasts and offering additional evidence that AI adoption may not be as detrimental to job opportunities as feared, since both are accelerating simultaneously.

Additionally, ISM services beat estimates as consumers increased their spending even as costs accelerated and interest expenses remained elevated. Investors are reacting to the plethora of developments by trimming equities across the four major benchmarks and most of the Magnificent 7 names, although 8 of the 11 principal stock sectors are gaining after the Nasdaq 100 briefly hit a fresh record in the first five minutes following the opening bell.

In fixed income, rates are rising relatively evenly across the curve, which is strengthening the greenback while derailing non-energy cyclical commodities and precious metals as Fed hike probabilities rise. Elsewhere, cryptocurrencies and volatility protection instruments are nearly flat while prediction markets catch bids.

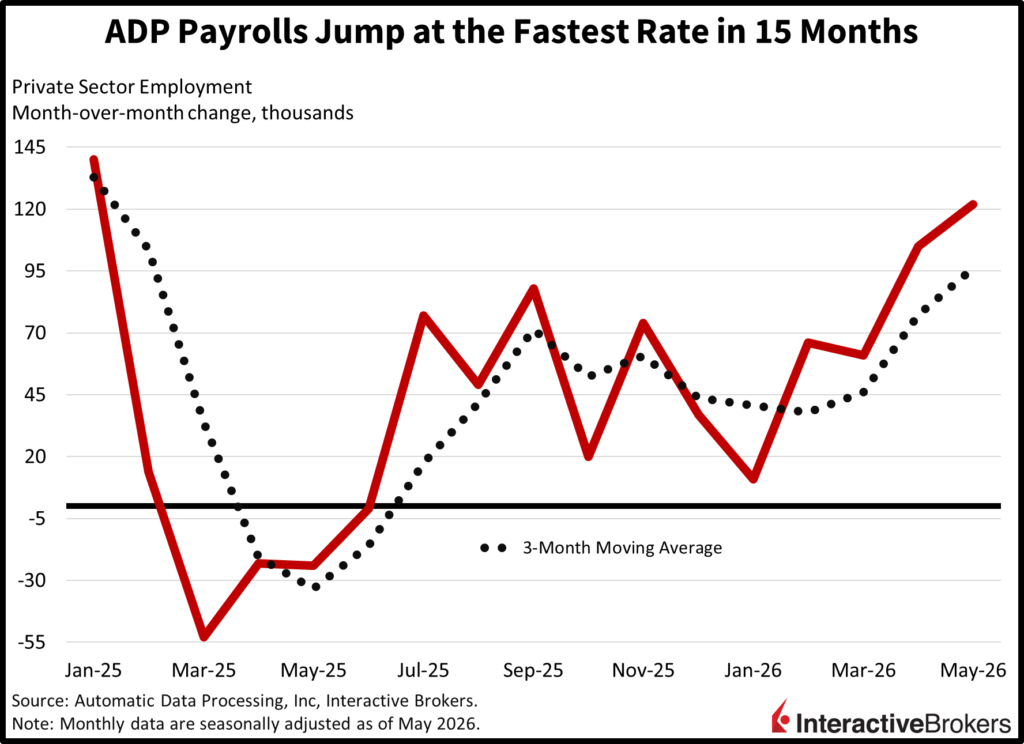

Employers continued to add workers last month

Hiring remained resilient in May, even as AI adoption, rising energy costs, elevated interest rates and geopolitical uncertainty could have dampened the accelerating labor market. Private sector payrolls grew by 122k last month, according to ADP. It was the strongest result since January 2025, exceeding the 117k expectation and the 105k reported for April. The expansion was broad-based across sectors and establishment sizes, with 8 of the 10 industries adding positions.

The education/health services, trade/transportation/utilities, professional/business services led with gains of 57k, 36k and 11k. Leisure/hospitality, financial activities, construction, other services and manufacturing contributed increases of 8k or less. On the flip side, information and natural resources/mining rosters shrank by 9k and 3k. Additionally, firms with 1-49, 50-499 and 500+ workers expanded headcount by 67k, 17k and 40k, respectively. Compensation trends were quite stable, with the year-over-year (y/y) change in median annual pay for job stayers and changers rising 4.4% and 6.5%, respectively, unchanged for the former and a tenth of a percentage point lighter for the latter relative to the prior period.

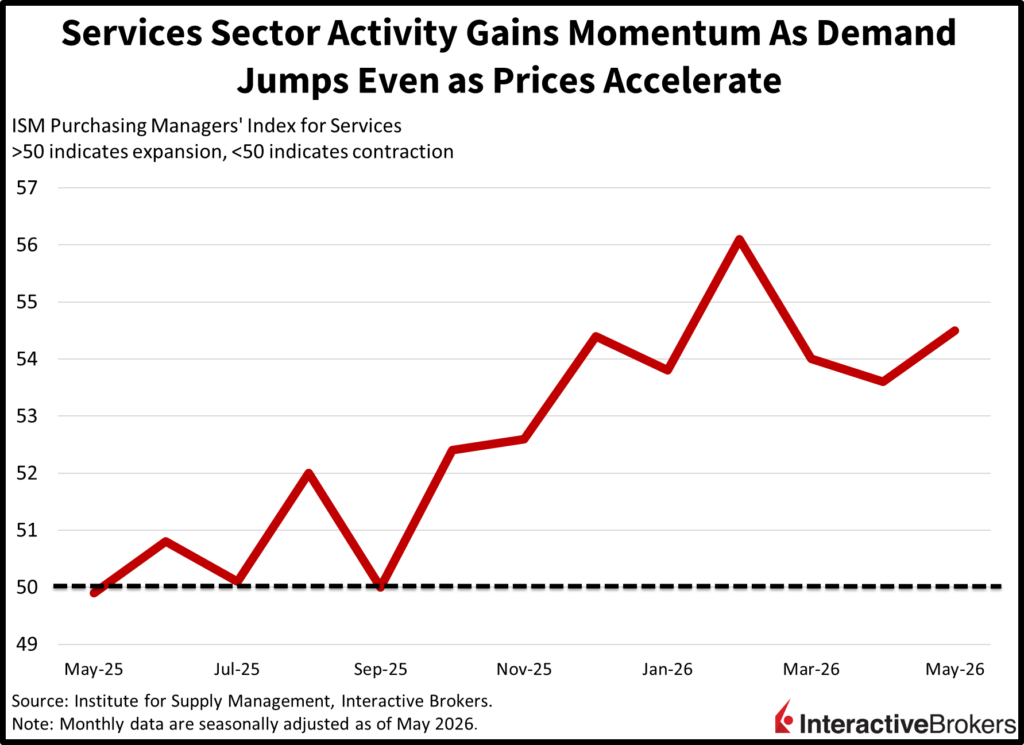

Services industry enjoys stronger growth

Services sector activity accelerated to the second-strongest pace of the year in May, marking a three-month high, driven by consumer spending overcoming fast inflation and high interest rates. The Institute for Supply Management’s (ISM) Purchasing Managers’ Index jumped to 54.5, arriving ahead of the 53.8 median estimate and April’s 53.6. Production and new orders led to robust performance, with scores of 57.7 and 57.3, up from the prior month’s 55.9 and 53.5, respectively.

Backlogs also contributed positively, though they slowed from 53 to 51.3. Headwinds included exports and employment, with the former falling to the expansion-contraction threshold of 50 while the latter sank further into negative territory at 47.9, which is odd given the stellar jobs numbers we’ve been seeing. Price pressures were also challenging, rising from 70.7 to 71.3, providing additional evidence that the energy-cost shock has spread across the economy.

Summer headwinds are adding up

Summer headwinds are adding up, with an unresolved Middle East conflict, renewed tariff pressures and a hawkish repricing across the Fed Funds curve, challenging additional equity market appreciation. The 20% rally from the March 30 lows to yesterday’s all-time high was driven by a belief that oil prices would sink substantially against the backdrop of an expensive war that both sides were losing appetite for continuing.

And while yields have recognized the significant inflationary forces that may require central bank tightening, accelerating corporate profit expectations and lighter forward earnings multiples have shouldered the burden of increasingly restrictive stock valuations. But from here, equities likely need to clear some of these hurdles before advancing further, as the pace of gains over the past few weeks already signals decelerating momentum.

International Roundup

China’s service sector expansion accelerates

China’s services sector experienced accelerating growth last month, with the S&P RatingDog China General Services PMI strengthening from 52.6 to 54.4, placing it firmly above the contraction-expansion threshold of 50. The result also squeaked past the economist consensus estimate of 52.3 and is the highest level in three months. With increased orders, the volume of outstanding work ascended to a nearly two-year high. Businesses responded by expanding their payroll for the first time in four months.

Entrepreneurs said order growth was driven by stronger client demand, business innovation and expansion, new products, improved market conditions and new client acquisitions. Sentiment for the coming 12 months, furthermore, remained above the long-term average with businesses expressing optimism about market conditions, new projects and the economy. Input costs, however, were a challenge. They grew at the fastest pace since October 2024. Higher wages and labor costs, along with more costly fuel, were the primary culprits.

Euro area gate prices jump

April factory gate prices in the euro area were up 4.9% y/y and 0.6% month over month (m/m), according to the Producer Price Index. While the monthly pace sank from 3.4% in March and met the economist consensus expectation, the annual rate was more than double the preceding periods 2% ascent. It also exceeded the economist consensus estimate by 0.1 percentage point.

For the monthly print, intermediate goods were up 1.8%. Both capital goods and durable consumer goods became 0.3% more expensive. The non-durable consumer goods category was flat while energy costs sank 0.4%. Nevertheless, energy was still up 12.6% y/y. Intermediate goods and durable consumer goods, furthermore, were up 3.9% and 2.7% y/y, while capital goods increased by 2.1%.

Australia’s economy slowed in the first quarter

Australia’s gross domestic product grew 0.3% during the first three months and was up 2.5% y/y with higher living costs, soaring energy prices, weather adversity and decreased government spending dampening results. While the y/y print matched the expansion of the final quarter of 2025, the quarterly pace slowed from 0.9%. It was the weakest showing since the first quarter of last year. In recent months, spending on electricity, gas and other fuels jumped 11.7% as the US-Iran conflict drove energy commodity prices higher.

The energy burden and higher interest rates in March caused shoppers to grow cautious, resulting in reduced spending across various household categories. Spending on essential goods and services increased by 0.8%, but outlays for discretionary items were nearly flat, rising by only 0.1%. At the same time, government expenditures grew only 0.2%, the lowest growth since the third quarter of 2022.

The sluggish outlays follow a period of elevated defense spending. At the state and local levels, governments terminated electric bill rebates. GDP also took a 0.8 percentage point hit from the nation’s trade deficit. Exports were hurt by adverse weather, curtailing mining production. The machinery and equipment sector (M&E) bucked the overall trend with private business investment jumping 16.3%.