Potentially major disruption to global sugar cane production does not appear to be fully reflected in bond prices. Mariam Bangura, Credit Analyst at Impax Asset Management, explores how a potentially strong El Niño event could create opportunities and risks within the high yield credit market.

Few things are ever certain, but an especially strong El Niño effect this year looks close to being so. [1] This warming of the equatorial Pacific Ocean – which occurs naturally every two to seven years – brings wetter weather to areas including the southern US and drier conditions to the likes of Australia, India and southeast Asia. Its distortion of ‘normal’ weather patterns can wreak havoc with global agricultural markets.

While agriculture is only a small part of the high yield universe, El Niño can be a first-order event for issuers directly exposed to several soft commodities – including cocoa, coffee and palm oil – whose production can be heavily impacted. Among European issuers that are commodity producers, rather than merely buyers, sugar is arguably the most significant crop.

Our analysis indicates that there could be a disconnect between what El Niño could mean for sugar producers and what the credit market appears to be pricing, supporting opportunities for active investors.

Will sugar prices spike?

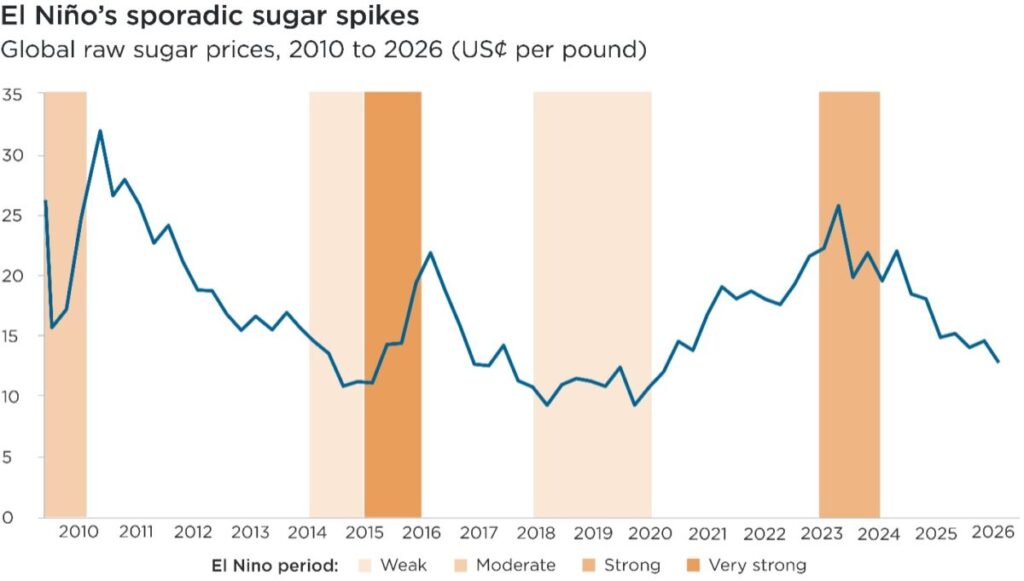

Sugar markets have been in turmoil recently, driven by strong production outpacing global consumption. Raw sugar prices fell sharply through 2025 and into 2026, reaching around 13.3 US cents a pound – their lowest in years – and remain near those lows. [2]

The prospects for global sugar prices later this year, and beyond, hinge largely on how El Niño plays out in Brazil, which exports approximately half of the world’s sugar cane. [3]

The wetter conditions that El Niño typically brings to southeastern Brazil – where the country’s sugar-growing is concentrated – are a double-edged sword: while positive for cane development, they are disruptive to mill operations, so delaying harvests and impacting crushing. The net effect on Brazilian supply is therefore ambiguous.

Should Brazil’s mills keep turning, flowing exports should offset the likely reduction in supply from drier conditions in Thailand and India, which respectively account for 11% and 7% of global cane exports. [4] Under these circumstances, a lid should be kept on global sugar prices – as transpired during the last El Niño event of 2023-24, when there was a record Brazilian crop. [5] Brazil has not always been able to fully offset the shortfall in Asian production during El Niño years, however. Prices spiked in both 2011 and 2016 (see chart below).

Europe marches to its own beet

To say there is one global price for sugar is not strictly accurate. Import tariffs mean that European sugar trades at its own price, somewhere between the global cane price and the price of subsidised, regionally-grown sugar beet. While a distinct crop, beet – roughly half of which is grown in the EU – is substitutable with cane once refined. [6]

Although El Niño is a tropical event, its potentially disruptive impacts on global cane production therefore have the potential to raise the ceiling for European sugar prices. The structural mechanics of the industry mean that changes to global or European sugar prices do not immediately pass through to producer revenues. Producers hedge against commodity price volatility by selling much of each season’s volume forward in advance – this year’s revenue is therefore largely fixed at the weak prices prevailing when those sales were struck. So, even if prices spike this El Niño season, any rally would be realised in cashflows a year or two from now.

El Niño’s potential impacts could be overlooked

Our analysis indicates that the possibility of a highly disruptive El Niño on sugar cane production this year might not be fully reflected in credit markets.

We believe a comparison of Europe’s two largest sugar producers – German group Südzucker and French competitor Tereos – highlights this potential disconnect.

While the former is overwhelmingly focused on European beet production, the latter also has a sizeable Brazilian cane business. Through hedging, both businesses have largely locked in revenues for this year at relatively weak price levels.

They offer differing exposures, however, to sugar prices when the hedges roll off. Unlike its Europe-focused peer, Tereos’ Brazilian exports offer exposure to a future global cane price that could – based on earlier El Niño years – be significantly elevated following adverse conditions this growing season.

Yet it was Südzucker’s credit spreads that tightened in May. Tereos’ bonds were meanwhile downgraded to ‘B+’ by credit ratings agency S&P. [7] Neither move had anything to do with the prospect of El Niño – Tereos’ downgrade followed an earnings report, while Südzucker shared a positive outlook.

This highlights the point, though: the market appears to be overlooking the possibility of an El Niño like 2010 or 2015 in its pricing of sugar producer bonds. We do not yet know how the all-important Brazilian harvest will play out, but the potential for global cane prices to surge – and be realised in cane producer revenues in 2027 and 2028 – is seemingly not reflected in spreads today.

Potential for credit dispersion

To be clear, this is not a forecast that sugar prices will spike – El Niño’s historic effects on global sugar production have been too unpredictable to support high-conviction predictions.

Instead, for credit investors, the point is that this El Niño is a dispersion event: its impacts could move the bonds of different producers based on their respective geographical footprints. Other factors are also at work, though, meaning this is not clear cut.

For instance, two supply factors are pushing European prices towards recovery: a reduction in local beet acreage and the reimposition of quotas on Ukrainian sugar imports. Some producers, including Südzucker, have diversified revenue streams from related products (like ethanol and ingredients) that are not perfectly correlated with sugar prices.

More broadly, and crucially, El Niño could widen the spreads between sugar producers who stand to gain from higher prices and sugar buyers whose margins are squeezed by them. Any sugar price rally – combined with higher fertiliser costs arising from the closure of the Strait of Hormuz – will be a net headwind for food and drink producers that are buyers of soft commodities, especially given their limited ability to pass on higher input costs.

Credit investors reflecting on their portfolio’s exposure to El Niño’s potential impacts may note that selected sugar producers are among the few issuers that can offer a direct counterweight to this possibility arising from a disruptive El Niño.

[1] World Meteorological Organization, June 2026: El Niño/La Niña Update

[2] Bloomberg data, June 2025. ICE Sugar No. 11 futures, generic front-month series (SB1) to June 2026

[3] OECD, 2025: OECD‑FAO Agricultural Outlook 2025‑2034

[4] OECD, 2025: OECD‑FAO Agricultural Outlook 2025‑2034

[5] Samora, R. & Teixeira, M., 31 August 2023. Brazil’s sugar production, exports projected to hit record highs. Reuters

[6] European Commission, 2026. Beet sugar represents roughly 20% of global sugar production

[7] S&P Global Ratings, June 2026: Tereos SCA Downgraded To “B+”