With a resolution in the Middle East now looking more likely, James Bilson, Global Unconstrained Fixed Income Strategist at Schroders takes a look at how bond markets may react once the focus moves away from geopolitics.

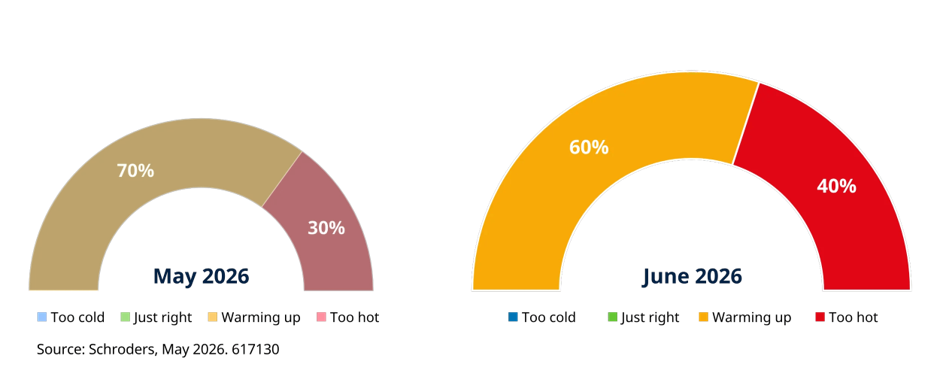

Two things are clear. Firstly, stronger US data is reducing the prospect of interest rates cuts by the Federal Reserve (Fed) and making hikes over the next year more likely. Secondly, while our view has become more hawkish, so has market pricing. We still see a slightly higher chance of the Fed staying on hold (“warming up”) than markets imply.

Probabilities assigned to our scenarios have turned more hawkish – but to a lesser extent than the market

Labour market loosens, labour market stabilises, labour market tightens?

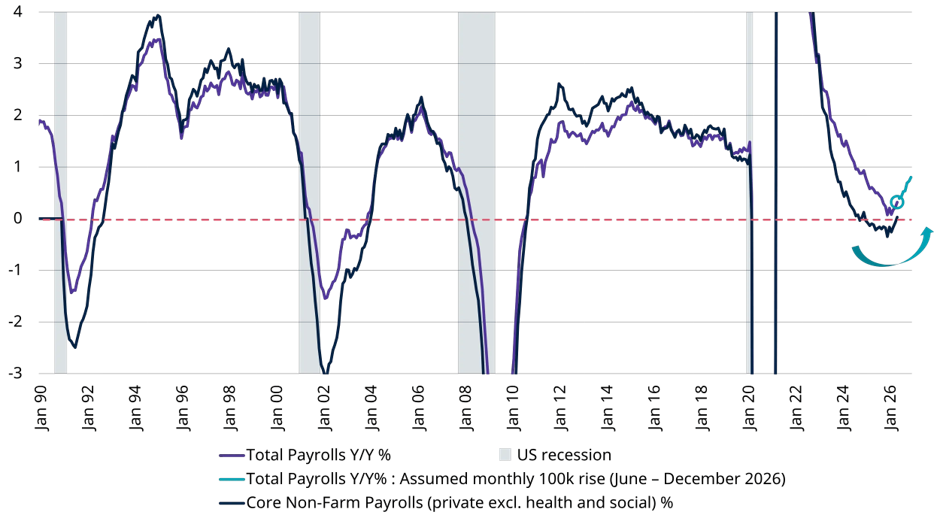

May’s US payroll report reinforced a trend we have highlighted for some time – that the labour market has stopped weakening and is now rebounding. This is critical for the Fed and for fixed income investors.

For now, the data points to a stronger labour market, but not yet a tighter one (tighter labour market conditions are typically bad news for inflation). But as the below chart shows, even if the US maintains a pace of 100k in monthly job growth from now until December – well below the recent three-month 188k average (which may have been exaggerated by World Cup related hiring) – payrolls will still be running at nearly 1% year-over-year growth. This is a pace that the supply capacity of the labour market cannot match. So even if payroll growth slows to around half its recent pace, a tightening of the labour market in the second half of 2026 becomes nearly inevitable.

US headline and core Non-Farm Payrolls % change

On the inflation side of the Fed’s mandate, there’s some good news with seasonality contributing to a more benign summer outlook and tariff-related pressure – worth 70–90bps on core PCE (personal consumption expenditures – the Fed’s favoured measure) expected to move towards zero in the second half of the year.

However, these tailwinds will be offset by similarly sized headwinds. We have yet to see the full impact of rising memory chip prices and broader tech inflation feeding through to consumers. Outside electronics, supply chain pressures and higher commodity prices are also lifting core goods inflation. Reopening the Strait of Hormuz will help, but is unlikely to solve the issue.

Overall, we expect core inflation to remain relatively unchanged, while headline inflation is likely to remain above 3%, unless oil returns to pre-war levels. Put simply, inflation is still too high.

Gilt-y pleasure?

Our positive view on Australian and Canadian bonds is unchanged. Both remain our preferred bond markets. However, we have upgraded our view on UK gilts. With energy concerns easing as an Iran deal looks more likely, we do not expect the Bank of England to raise rates, despite some hikes still being priced in. Labour market weakness, alongside a gradual (if uneven) improvement in domestic inflation pressures, such as wage growth and services inflation, supports this view.

The ECB sends a hawkish policy signal

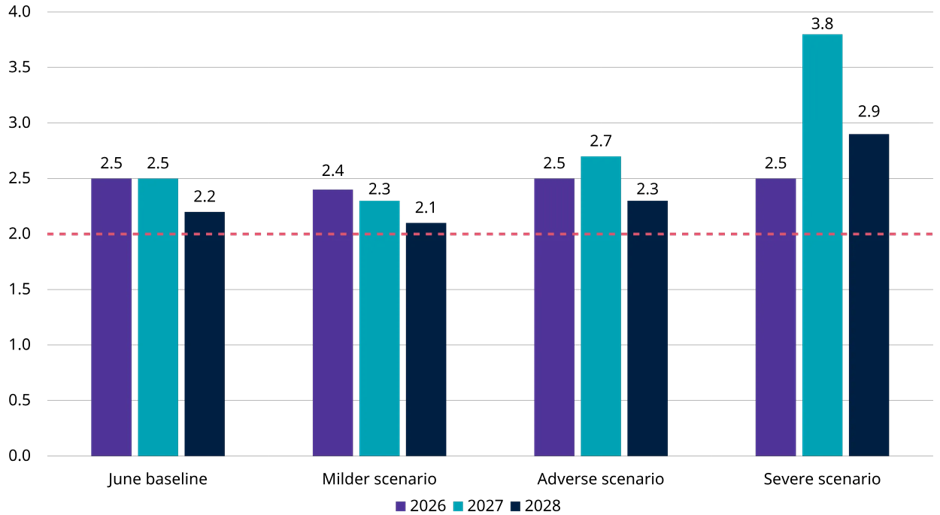

We have already seen the European Central Bank (ECB) tighten policy at its latest meeting on 11 June. Even though economic growth in the eurozone is subdued, we don’t think it has slowed enough to stop the ECB raising rates further. Indeed, its forecasts show core inflation above target across all horizons and in all scenarios, despite higher rates being assumed in the process.

ECB core inflation forecasts – baseline and scenarios

While we do not see these forecasts as likely to transpire, it is an important signal of the ECB’s view – and, for now, that view remains hawkish until proven otherwise. For this reason, we see German bunds as a good short when paired against our long position in gilts.

Asset allocation

The main change to our asset allocation is to neutralise our view on corporate credit. Valuations remain unappealing, but a benign macro backdrop suggests that zero is the appropriate score. We maintain a preference for hard currency emerging market debt and US agency mortgage-backed securities.