PIMCO’s Lotfi Karoui, Multi-Asset Credit Strategist, discusses the optimism in U.S. credit markets as analysts raise earnings and margin expectations for investment-grade and high-yield corporate issuers, with AI hyperscalers’ capital spending playing a central role in future earnings and capex forecasts.

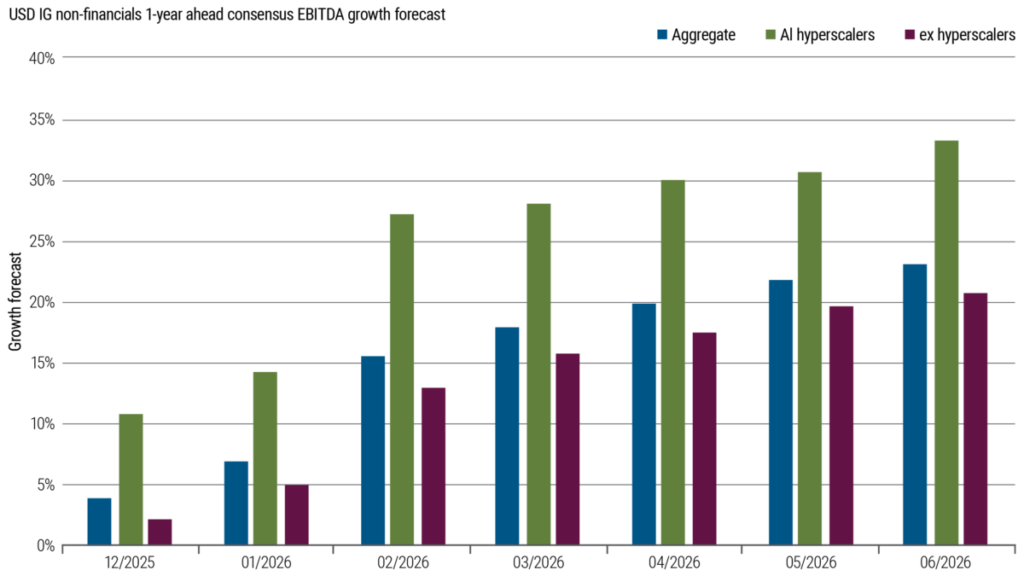

Since the start of the year, the market has become more optimistic on the earnings outlook for U.S. dollar (USD) investment grade (IG) corporate issuers, shrugging off the Iran conflict and consistently revising earnings forecasts higher (see Figure 1). The first wave of upgrades came after the AI hyperscalers reported, by and large, strong earnings. But most of the improvement has stemmed from the rest of the non-financials index, with analysts quadrupling their one-year aggregate EBITDA (earnings before interest, taxes, depreciation, and amortization) growth expectations, from 5% at the end of January to more than 20% as of 30 June.

Figure 1: Analysts have increased one-year-ahead EBITDA growth forecasts for USD IG corporate issuers

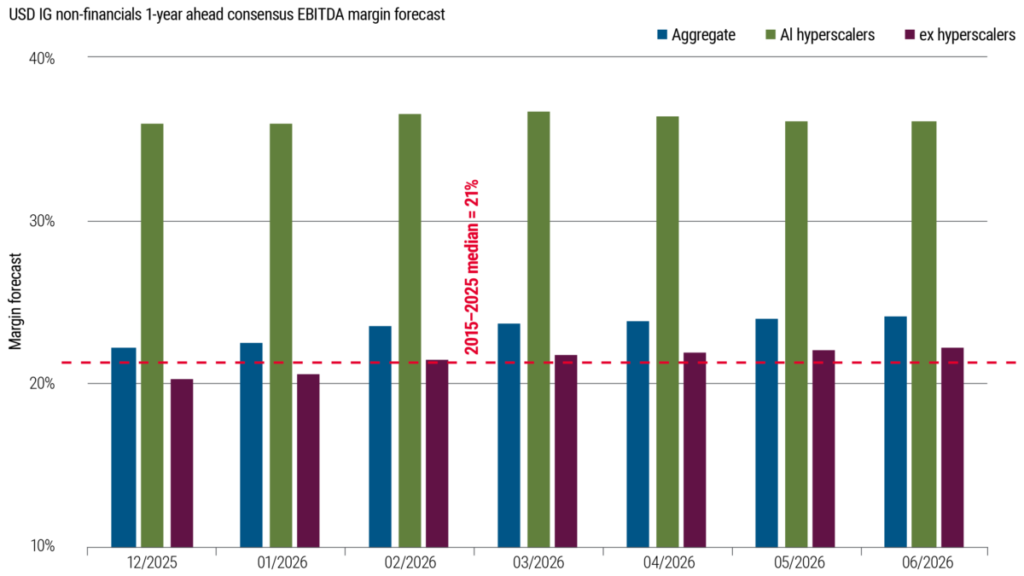

And despite modest fears of an inflationary shock that would eat away at margins, the market has so far believed these fears to be unwarranted; aggregate margin expectations for USD IG corporates have improved from 20% to 24% since the start of year, above the 2015-2025 median of 21% (see Figure 2).

Figure 2: EBITDA margin expectations have risen above the median of the past 10 years

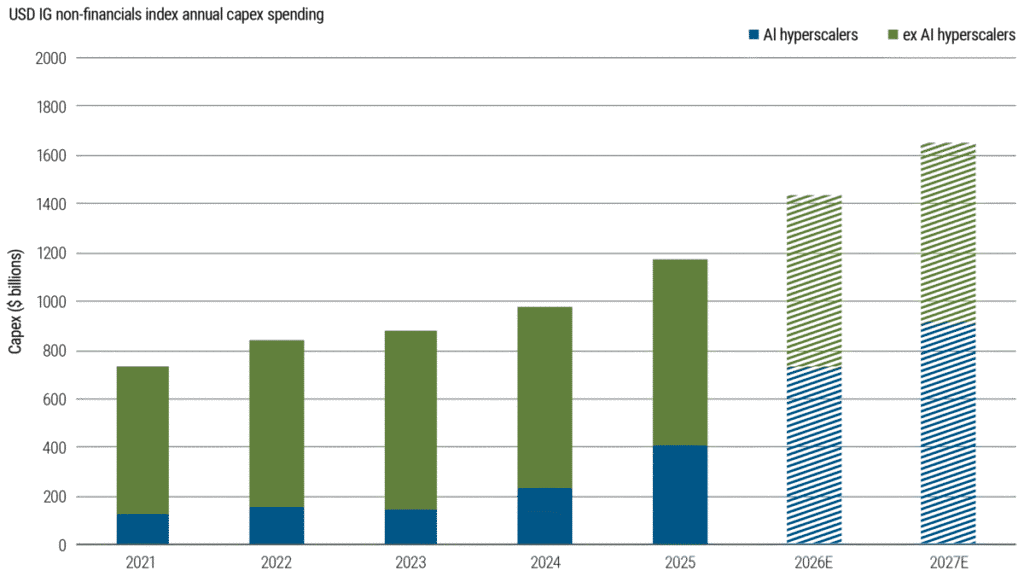

Aside from earnings, company forward guidance vis-à-vis capital expenditure plans will remain a key focus, particularly for the hyperscalers. As of 2025, these five firms accounted for around one-third of aggregate USD IG corporate capex.

Although current-year capital plans are already largely set, the focus will be on additional insight into 2027 and beyond, with current forecasts for hyperscalers to account for 54% of total capex by 2027, or $915 billion (see Figure 3). In fact, relative to 2025 levels, the entirety of the expected expansion in USD IG corporate capex has been driven solely by the five hyperscalers.

Figure 3: AI hyperscalers are expected to account for more than 50% of USD IG corporate capex by 2027

A second-order effect related to capex is that it directly feeds into future earnings expectations; the underlying revenues are recognized as they arise by the “pick and shovel” parts of the AI ecosystem, while the expenses are capitalized for the hyperscalers, thus won’t ultimately be included in EBITDA figures.

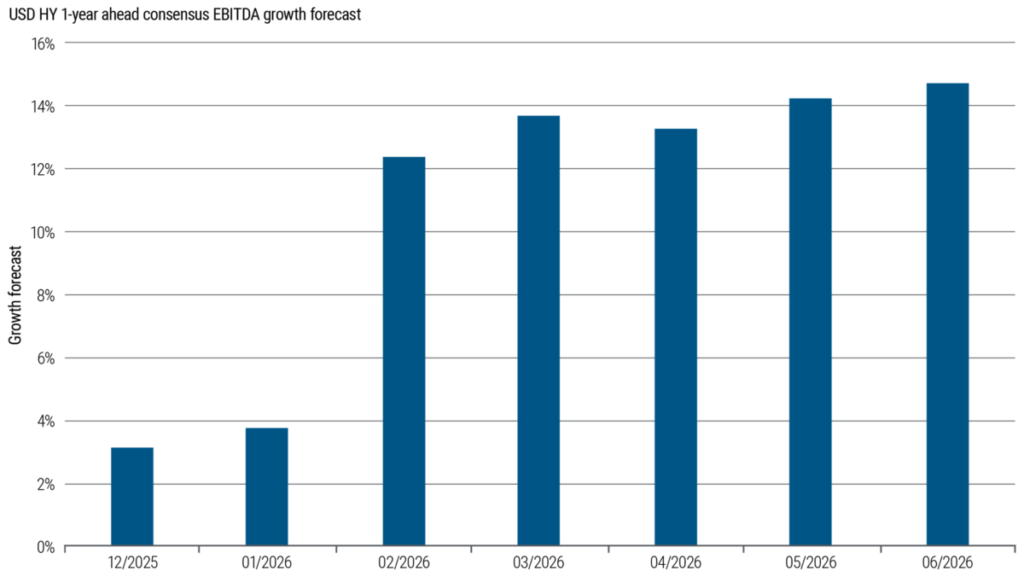

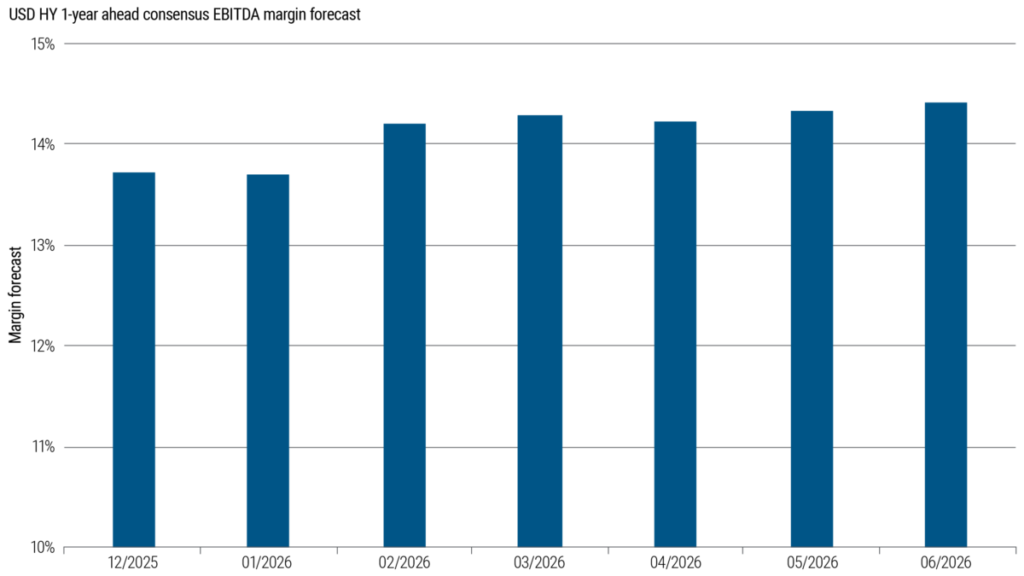

The same earnings optimism can be seen across USD high yield (HY) issuers as well. Figure 4 shows that since the end of January, analyst expectations for aggregate EBITDA growth have climbed from just under 4% to more than 14% as of the end of June, with expected EBITDA margins relatively stable (see Figure 5).

Figure 4: Analysts have raised EBITDA growth forecasts for USD HY issuers this year

Figure 5: USD HY EBITDA margin expectations have remained stable

To be clear, this universe of index firms is held constant, as of December 2025, and thus isn’t driven by any compositional effects year-to-date, such as fallen angels (IG issuers downgraded to HY), which would typically have higher EBITDA than the average HY firm given their size. Thus, it is more of a reminder of the resiliency of the U.S. economy so far, despite signs of a deeper K-shaped economic divide (for more, see the 13 April “The Credit Market Lens: Oil Supply Shocks Don’t Age Well”).

Of course, as we enter earnings season in earnest over the coming weeks, time will tell whether the optimism reflected in analyst expectations is warranted for these USD IG and HY issuers.

![[uns] renewable energy](https://wealthdfm.com/wp-content/uploads/2025/11/karsten-wurth-0w-uTa0Xz7w-unsplash-1.jpg)