Short-dated UK government and corporate bonds have demonstrated significantly lower volatility and more resilient performance than broader fixed income markets during recent periods of bond market turbulence, according to analysis from Aberdeen Investments.

The findings come as investors reassess the role of fixed income in portfolios against a backdrop of heightened macroeconomic uncertainty, shifting interest rate expectations, and more pronounced volatility across global bond markets.

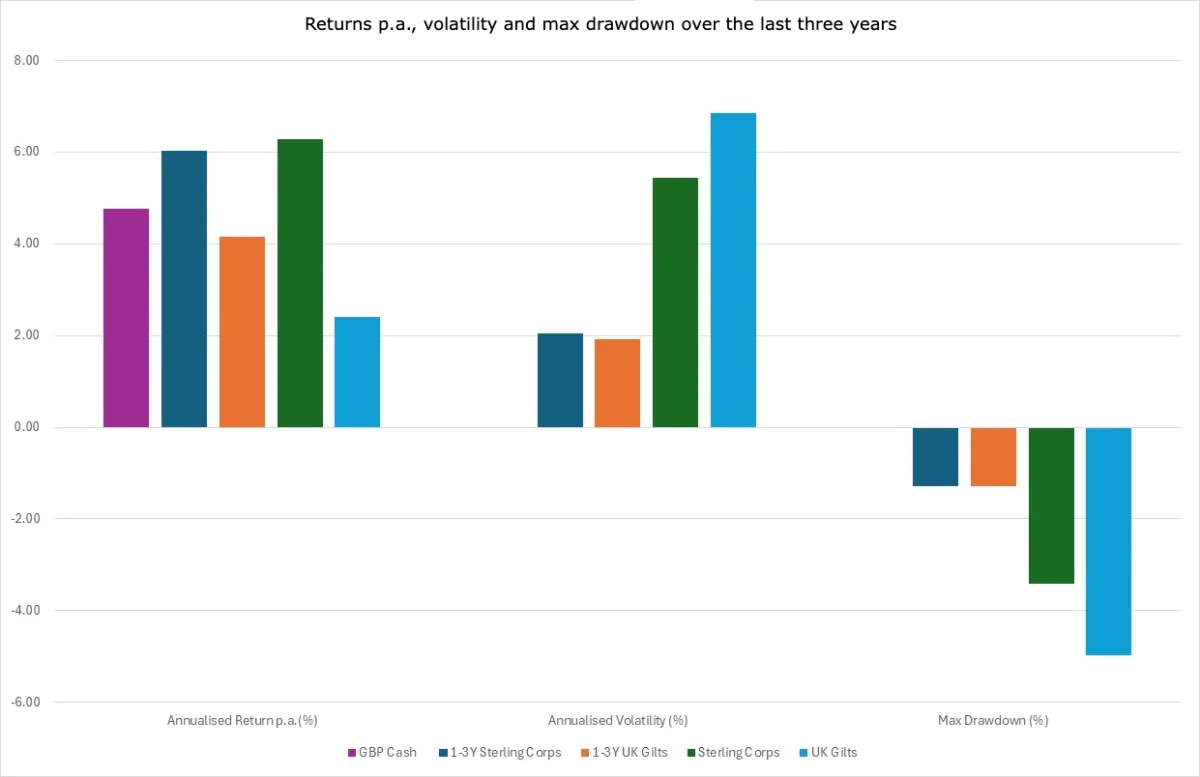

Aberdeen’s analysis shows that sterling-denominated UK corporate bonds and gilts with a maturity between 1-3 years have annualised volatility of around 2% and 1.9% respectively over the past three years*. This is significantly lower than the 5.4% and 6.9% experienced by longer dated UK corporate bonds and gilts respectively.

Over the same time period, max drawdowns – which is the largest percentage drop in the value of an investment from its highest peak to its lowest trough – were approximately -1.3% for both short-dated UK corporate bonds and gilts, versus -3.4% and -5% for longer dated corporate bonds and gilts.

“Short-dated credit is increasingly being used not just as a step out of cash, but as a core building block. It offers a balance between maintaining capital stability and generating income, which is particularly valuable in a more uncertain and volatile environment.

“As markets continue to adjust to evolving macroeconomic conditions, managing risk and maintaining flexibility within fixed income portfolios could be important for investors. In this context, short-dated bonds might be well positioned to play an ongoing role in delivering more stable outcomes for investors.”

Mark Munro, Investment Director, Fixed Income at Aberdeen Investments and manager of the Aberdeen Short Dated Enhanced Income Fund

Figure 1: Short-dated sterling-denominated bonds in comparison to longer-dated bonds

Source: ICE BofA 1-3 Year Sterling Corporate Index, ICE BofA 1-3 Year UK Gilt Index, ICE BofA UK Gilt Index, ICE BofA Sterling Corporate Index, ICE BofA SONIA Overnight Rate Index, data as at 31 May 2026.

“The current environment has challenged some of the traditional assumptions around fixed income. Assets that were once seen as low risk, including parts of the government bond market, have experienced more pronounced volatility.

“In that context, short-dated credit has stood out for its ability to combine income with relative stability, making it an increasingly important consideration when it comes to assessing the balance between risk and return.

“As interest rate expectations have shifted, we’ve seen greater volatility in longer-dated bonds, while short-dated credit has provided a more stable return profile. That combination of lower sensitivity to rates and still-attractive yields is increasingly appealing to investors.”

Mark Munro

Elevated yields supporting short-dated bond demand

Aberdeen notes that yields on short-dated bonds are still relatively high compared to recent years, which makes them more attractive to investors. Starting from a higher yield means investors have more of a “buffer” if markets become volatile, helping to soften the impact of ups and downs in bond prices.

Short-dated bonds deliver comparable levels of income to longer-dated bonds, but with lower interest rate risk, with offering a yield of around 5.3% for bonds with a maturity between 1-3 years, compared with 5.7% for longer dated bonds, despite having a significantly shorter duration of approximately 1.8 years versus 5.8 years for longer-dated bonds**.

Short-dated bonds tend to be more stable as they mature quickly, usually within three years. As a bond gets closer to its maturity date, its price naturally moves closer to its original value – something known as “pull to par”. This can help steady returns over time and make losses less likely, especially over shorter investment periods.

Aberdeen notes that short-dated bonds also continue to offer a meaningful yield advantage over cash, with a pickup of around 1.6%***, providing additional compensation for the modest increase in risk, meaning the asset class can potentially enhance returns on the more defensive portion of an investor’s portfolio, while still maintaining a strong focus on capital stability.

Aberdeen’s analysis also reflects a broader shift in how investors are thinking about liquidity. While cash and money market instruments have traditionally played a central role, declining yields and increased volatility in other defensive assets have prompted investors to look more closely at alternative sources of income and stability.

The Short Dated Enhanced Income fund turns three years old on 6 July 2026.