Artificial intelligence is driving a structural increase in global electricity demand, pushing power generation and grid infrastructure to their limits. As renewables emerge as the fastest and most economical solution, green bonds are becoming an increasingly important source of capital—connecting long-term digital growth with scalable, low carbon energy investment.

AI’s paradigm shift

Artificial intelligence (AI) is now shaping the global economy at a speed that is hard to overstate. Its influence now extends far beyond software. AI depends on a vast physical infrastructure spanning computing, data and power, each expanding at a pace that is already testing today’s capacity.

The computing side is the most visible. More than a billion people are now using AI-enabled platforms in some form, from search interfaces to productivity tools. This surge has driven intense demand for advanced chips. The race for processing capability is shaping investment plans across major technology companies and influencing supply chains and global trade policy.

Behind the scenes, the data footprint is growing even faster. Each new model increases the load on data centres. McKinsey estimates that supporting global AI workloads may require about US dollar (USD) 5.2 trillion in capex by 2030, much of it from hyperscalers already expanding rapidly. The biggest bottleneck, however, is power generation. AI demands vast and steady electricity supply. Forecasts suggest global electricity consumption could rise by more than 40% over the next decade, with data centres accounting for a growing share. Meeting this need requires major investment in new transmission lines and grid upgrades. These pressures are already visible, and the gap between current and future capacity is widening.

Surging energy demand from data centres

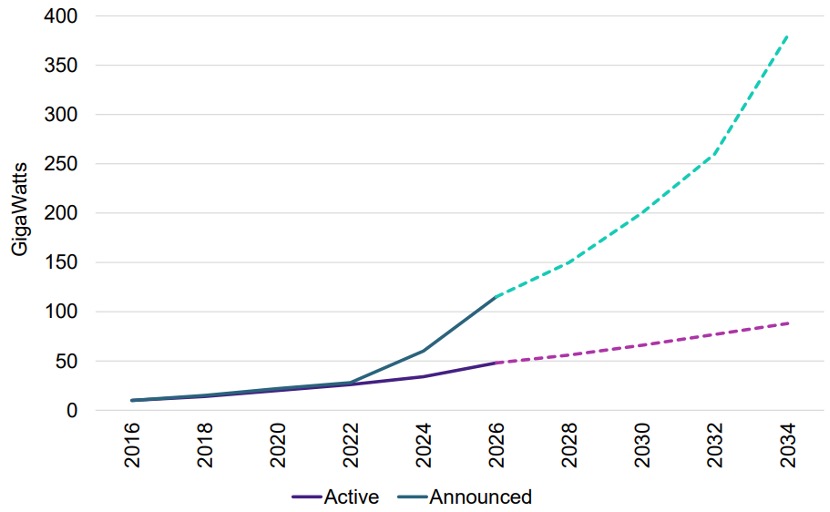

The steep rise in US data centre construction shows how quickly AI is reshaping the energy landscape. Goldman Sachs expects installed capacity to reach around 46GW by October 2025, an annual increase of 36% (see Chart 1). Much of this growth is concentrated in regions boasting proximity to end users and reliable access to large volumes of power. Around 70% of the 12.4GW of new capacity expected in 2025 is clustered in locations that can offer both.

Developers are planning for a data-driven future. A further 63GW of new projects has already been announced, reflecting the long-term investment cycle underpinning AI infrastructure. Hyperscalers continue to build at pace, and are competing for land, grid connections and electrical supply.

Chart 1: US Data centre capacity

All of this depends on meeting the demand for power. After two decades of flat demand, electricity consumption projections point to a 40% rise over the next decade driven by AI, digitalisation and new manufacturing. Current infrastructure cannot absorb this easily. Our analysis suggests that meeting future demand will require a sixfold increase in the rate at which new generation and transmission capacity is built.

Alongside this physical build-out, financing activity is accelerating. Debt issuance linked directly to AI infrastructure continues to grow as utilities, developers and technology companies raise capital for new power supply, storage and data centre construction. This further reinforces the connection between AI expansion and long-term energy investment.

The US grid exemplifies the scale of the challenge. Connecting the projects already in the transmission queue is estimated to require about USD 4 trillion. This represents one of the largest infrastructure build-outs in modern history. It also presents a substantial opening for private capital, particularly for investors who can support renewable energy, storage solutions and grid modernisation at scale.

China’s leadership in power production

Any discussion of electricity demand must consider China. As living standards rise and industrial capacity expands, its long-term energy needs will continue to grow. The transition away from coal toward renewables therefore represents one of the largest decarbonisation opportunities in the global system.

China’s approach to power generation also illustrates how quickly national strategies can shift when energy security and economic priorities align. Nuclear power is a clear example. After beginning to scale capacity around the turn of the century, China accelerated development sharply after 2010. By 2024, its nuclear output had reached roughly 450TWh, more than three times Germany’s peak generation before its phase-out. Germany’s withdrawal from nuclear followed post-Fukushima politics. China faced different pressures, seeing nuclear as a way to strengthen energy independence and support its industrial strategy. The result is a power system undergoing rapid diversification.

Alongside nuclear, China continues to add record volumes of solar and wind capacity each year, even as it builds new coal plants to meet short-term demand and stabilise the grid. This combination highlights the global challenge: countries are trying to expand low-carbon power at speed while maintaining economic growth. For investors, it reinforces the scale of the infrastructure build-out required worldwide and the importance of financing tools that can accelerate renewable deployment without adding fiscal strain.

Renewables: the fast, cheap path forward

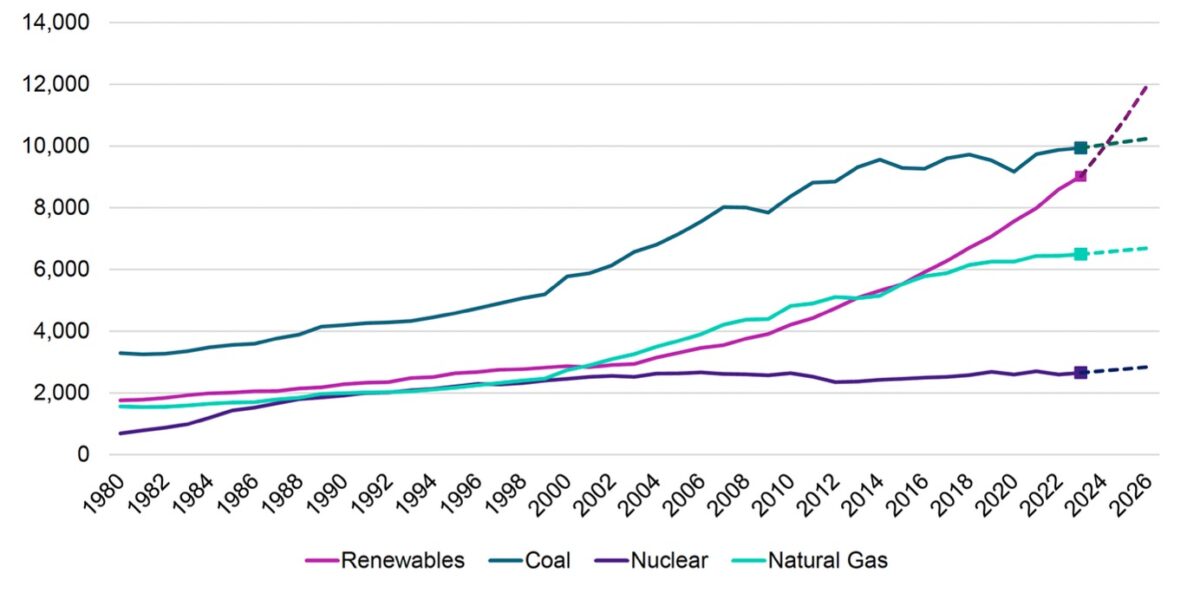

As electricity demand accelerates, the economics of generation are shifting decisively toward renewables. Wind, solar, hydro, bioenergy and geothermal now form the largest single source of global electricity production (see Chart 2). This shift has been driven by falling costs, better technology and a growing global project pipeline.

Chart 2 – Global Electricity generation by source (TWh)

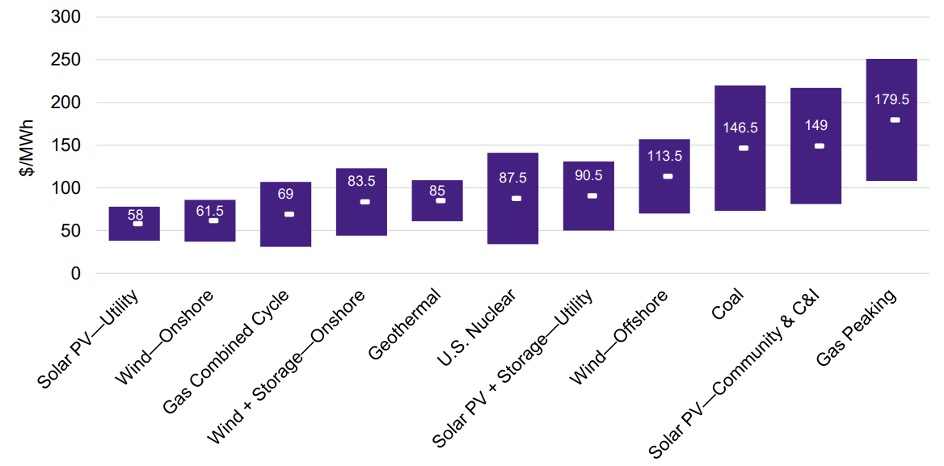

The cost advantage is evident. Levelised cost of energy analysis (chart 3) shows that, under the right conditions, many renewable technologies remain competitive with conventional generation. In regions with strong solar resources or consistent wind patterns, costs have declined to the point where renewables are often the cheapest new source of power. Their modularity also allows capacity to scale quickly, crucial in markets facing structural increases in demand from AI, electrification and new forms of industrial production.

Chart 3: Levelised cost of energy comparison

The challenge is that the AI boom may outpace even this rapid expansion. Computing power is becoming the defining input for the global economy, and the capital intensity required to support it is rising. Analysts estimate that AI companies could require around USD 2 trillion in combined annual revenue simply to fund the infrastructure needed to meet projected demand for compute. That level of investment is only viable if the power underpinning AI becomes cheaper, cleaner and more abundant.

This only compounds the case for renewables that can offer the speed, scalability and cost profile needed for long-term energy security. But turning potential into capacity requires vast amounts of capital and a financial system capable of directing it into projects at scale. That is where green bonds begin to play a central role.

Green bonds: financing the transition

Meeting AI-era energy demand will require capital far beyond traditional funding sources. Green bonds have therefore become one of the most important tools for financing the shift toward cleaner, more resilient power systems. Issuance reached its high point in 2021, led by Europe, but volumes are once again approaching those levels. The rise of anti-ESG sentiment has arguably forced sustainability to evolve beyond virtue signalling, driving a more comprehensive market-based approach. The market has matured, with clearer standards, stronger disclosure and deeper participation from institutional investors seeking predictable, asset-backed exposure to the energy transition.

Europe’s progress in digital infrastructure is following a similarly maturing path. According to the European Data Centre Association, more than EUR 100 billion is expected to be invested in data centres across the region by 2030. Crucially, these facilities are now operating on a power mix that is about 94% renewable, making Europe the greenest data centre market globally. This alignment between clean power and digital expansion shows how green financing can accelerate growth while supporting climate goals.

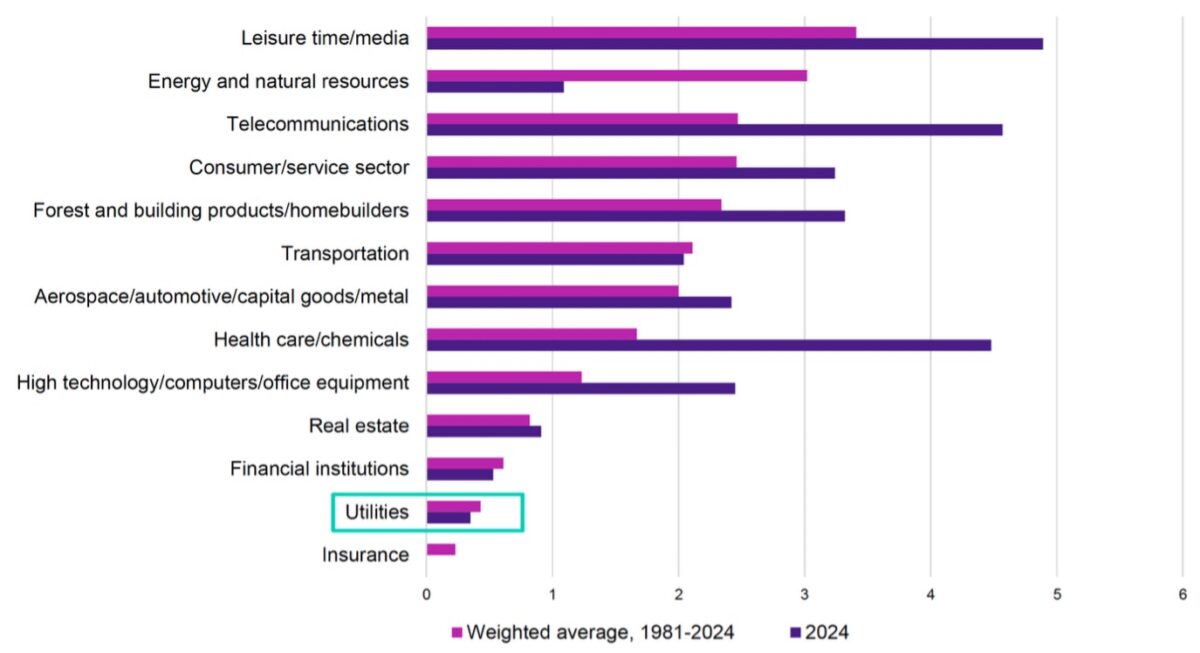

The broader point is that green bonds offer a practical way to channel capital into the infrastructure that underpins both AI and decarbonisation. They give investors clarity over use of proceeds, help issuers lower funding costs and support the build-out of renewable capacity that global electricity systems now urgently require. Utilities also remain one of the most stable sectors in global credit markets, with low default rates (see Chart 4) and long-term revenue visibility. This makes them well suited to finance large-scale renewable projects through green bonds, as investors gain exposure to essential infrastructure with predictable cash flows.

Chart 4: S&P global default rates

Europe’s ability to power its digital expansion with such a high share of renewables reflects the diversity of its energy mix. Different regions contribute in different ways. The Nordics provide abundant wind and hydro, offering some of the most stable and low-carbon electricity anywhere in the world. Southern Europe’s solar resources support fast, cost-effective development, whereas legacy hubs such as Frankfurt and Dublin rely more on battery storage and grid flexibility to manage variable loads.

Across the region, investment in smart grids and new access agreements is helping to speed up deployment. New approaches, including phased and non-firm connections, are helping to reduce connection timelines from seven to ten years to roughly one year in some markets, unlocking capacity while longer-term upgrades are completed. These improvements allow faster renewable connections and give operators better control over electricity flows. Together, they can help realise a cleaner and more resilient power system capable of meeting rising demand from AI and digital services.

Policy is another important factor. The EU’s focus on digital sovereignty has strengthened the case for developing more local compute capacity. Rather than relying on US-based cloud platforms, European institutions and corporates are being encouraged to build and store data within the region. The scale of interest is already visible. Around 170GW of data centre connection requests have been submitted across Europe, equivalent to almost one-third of the continent’s peak power demand. This underlines both the speed of digital expansion and the size of the opportunity for investors who can support the energy and grid infrastructure needed to keep pace.

Summary

As AI accelerates, the real bottleneck lies in power generation. Meeting future energy demands will require a concerted shift toward renewables, which remain the most economical and scalable option. Green bonds are poised to play a pivotal role in financing this transition, enabling infrastructure that supports both AI growth and climate goals. Green bonds offer a strategic counterbalance, directing private capital into clean energy and grid infrastructure at the scale required to support both AI-led economic growth and long-term environmental resilience.

To learn more about sustainable fixed income investing, read Amova Asset Management’s investment guide here.

By Steven Williams, Head of EMEA Global Fixed Income

Steven Williams

Steve Williams is the Head of EMEA Global Fixed Income and a Managing Director in Amova Asset Management’s London office. He is a member of the fixed income and foreign exchange investment committee as well as the portfolio manager with oversight for the firm’s investment grade, municipal, global green bond, global mortgages and global bond business.

He joined Amova AM in 2007 and took over co-management responsibility for the firm’s flagship global sovereign bond strategy as well as launching the first dedicated Danish mortgage bond strategy into Japan in 2016 and has managed Amova’s Global Green Bond strategy since 2015.

Steve, previously served as a Credit research analyst with New York Life Investment Management in corporate bonds and structured finance as a senior analyst. He has over 20 years of investment experience and holds an MBA from Duke University’s Fuqua School of Business. He received his undergraduate degree from the University of Michigan and is a certified FRM.