Ten years on from the referendum, Brexit appears to have contributed to a slower-growth, lower-investment and lower-productivity economy, even if it did not trigger the economic collapse many feared. Hetal Mehta, Chief Economist at St. James’s Place, comments on the 10-year anniversary of Brexit.

Ten years on from the Brexit referendum, the UK economy has not suffered the cliff-edge shock many feared. But nor has Brexit been cost-free. Its impact has been slower-burning, less visible in any single year, but meaningful when viewed through the lens of investment, productivity, trade and labour supply.

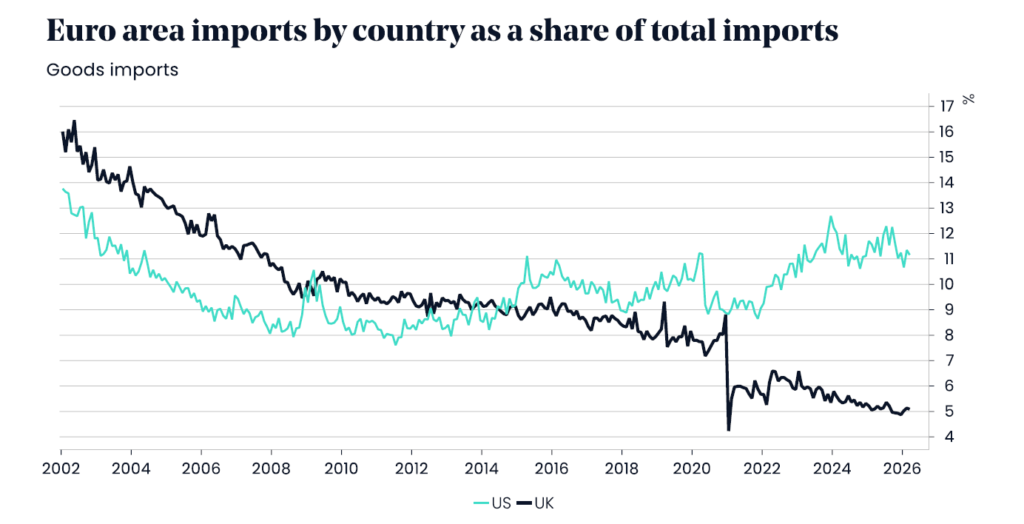

The UK’s trading relationship has changed

The difficulty is that Brexit has been followed by a series of major shocks – Covid, the energy crisis, war in Ukraine and a global inflation surge – which makes it hard to isolate its exact effect. But there are areas where the signal is clearer.

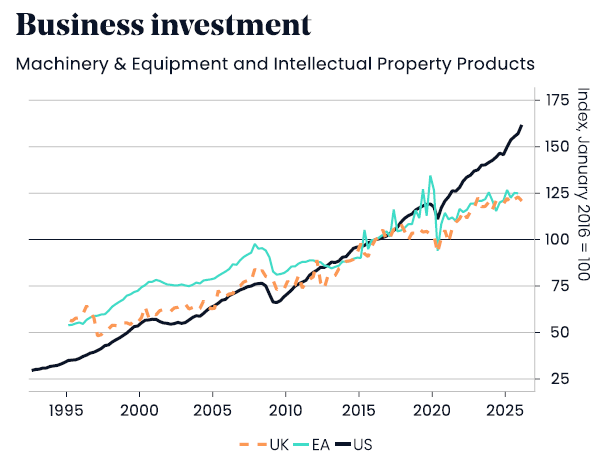

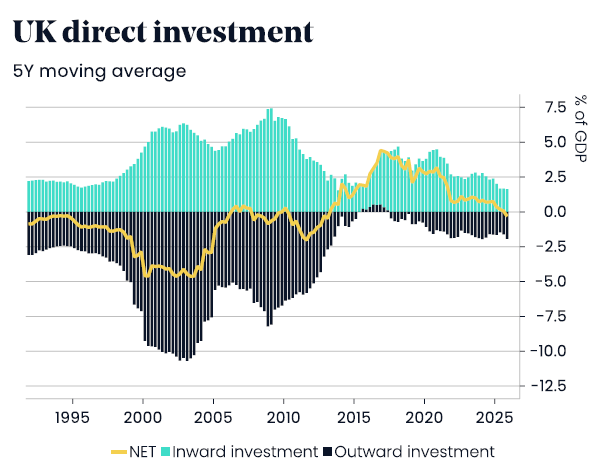

The UK’s share of European imports has fallen since 2016, business investment has lagged the US, and inward direct investment has weakened. None of these trends can be attributed to Brexit alone, but Brexit has almost certainly amplified them.

The most important consequence is not that Brexit caused an economic collapse. It did not. The bigger issue is that it appears to have contributed to a lower-investment, lower-productivity environment at a time when the UK could least afford it. A weaker sterling also raised import costs, adding to inflationary pressure, while changes in migration patterns have altered the labour market and contributed to capacity constraints in some sectors.

Investment is where the long-term cost emerges

For investors, however, the picture is more nuanced. The UK economy still faces structural challenges and there is now the added uncertainty of a Labour leadership contest, but UK equities look attractive from a valuation perspective, particularly relative to the US. The market also offers diversification benefits, given its more defensive sector composition and global revenue exposure.

Our central global/US scenario remains a soft landing, but investing late in the cycle is always difficult. The UK’s Brexit legacy is not one of dramatic collapse, but of gradually weaker momentum. That makes selectivity and diversification essential – and it also means investors should not overlook UK assets simply because the macro story has been difficult.