In the U.S., higher and more persistent inflation may mean a shift in expectations. Could the current $15 billion per month pace of tapering be accelerated to say $20 billion per month? And how soon and by how much will interest rates be increased?

We continue to expect the Fed will keep the tapering pace at $15 billion as markets like consistency. With tapering likely to end in mid-2022, we expect the Fed to take stock of conditions at that time and look for unemployment below four percent before raising rates. We anticipate one increase in late 2022, though we acknowledge a second hike in 2022 is possible if inflation remains high.

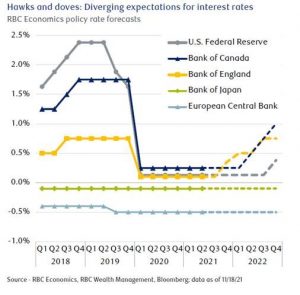

The doves

At the other end of the spectrum, the Bank of Japan (BoJ) and the European Central Bank (ECB) are unlikely to increase interest rates before 2023.

Japan’s economic recovery has been slower compared to peers in 2021 due to a series of long-lasting and stringent COVID-19 restrictions. Inflation has been soft at a mere 0.2 percent year over year, partially due to government policies such as encouraging major telecom carriers to cut mobile phone fees. Given the muted inflation, we expect the BoJ to maintain its policy rate at negative 0.1 percent until late 2023.

By contrast, the October CPI in the eurozone reached 4.1 percent, up from 3.4 percent the previous month.

The price increases were broad-based. With the recovery proceeding at a healthy pace, we believe the ECB is likely to start to rein in monetary stimulus. It already indicated it aims to terminate its Pandemic Emergency Purchase Programme in March 2022, though it will likely transition to a separate, existing asset purchase programme, lasting well into 2023, to continue to support regional economic activity. Markets do not expect the ECB to increase interest rates until sometime in late 2023.

Stay alert

Higher and persistent inflation can change market expectations for tightening of monetary policy, creating volatility. So far, fixed income markets have borne the brunt of this as equity markets seem to have been largely immune, though this may change over 2022. With this in mind, keeping an eye on housing costs and wages can help investors assess future central bank moves.