Navigating through these numerous cross currents has been hazardous for investors. Some of the biggest beneficiaries of the working-from-home (WFH) boom are now well below their peaks. The Citi Global Stay at Home Basket is 21% below its peak in February. Zoom Video Communications is down -56%, Peloton Interactive -73%, Roku -47% and Just Eat Takeaway -52%.

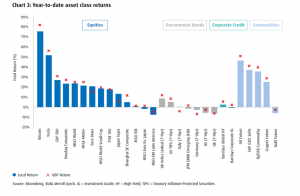

In terms of conventional asset classes, developed market (DM) equities rose strongly and outperformed emerging market (EM) equities and bonds. There was remarkably little difference in returns on tech, as measured by the NASDAQ or FAANGs, versus more conventional DM equities, though this masks major divergences during the year. MSCI World Small Cap outperformed in the first quarter but has fallen to be 4% below Large and Mid-Cap. Longer term small cap outperformance has been skewed by outsized initial bull market bounces. With sterling little changed against the euro and the dollar, exchange rates affected returns to UK investors only marginally, though the weakness in the yen damaged unhedged returns on Japanese equities.

In the bond market, inflation protected securities were the place to be. Conventional government bonds gave negative returns in most markets. Long duration bonds (not shown in the chart) had a very volatile year and have rallied recently but still generated negative returns overall. Corporate debt fared only slightly better. Commodities generated strong returns, though gold was a notable poor performer despite rising inflation and negative real interest rates. Some commentators suggest that Bitcoin has displaced gold as a safe haven. I doubt that ‘safe haven’ will prove an enduring feature of Bitcoin and its relatives.

This pattern of returns can be readily traced to macro fundamentals. Economic growth surprised strongly to the upside in DM, even though forecasts began the year fuelled by optimism given the promise of vaccine success. By contrast, growth in EM in general, and China in particular, was disappointing. The crisis in the property sector looks set to cast a medium-term shadow over China’s economic performance, even though targeted policy supports are now being implemented.

Strong growth in DM fed through to corporate earnings, which beat analysts’ estimates in spectacular fashion. Earnings growth in 2021 looks set to come in at 51% in the US, 52% in continental Europe and 83% in the UK.

Inflation also beat forecasts and this damaged bond returns, even though central banks in most DM kept official rates on hold and maintained their aggressive bond buying programmes. Expectations of interest rate hikes for 2022 did rise and the US Federal Reserve finally retired the word ‘transitory’ as a description of inflation in December – much too late in my opinion – and gave a clear signal that they planned to taper their bong buying more steeply. Despite relatively weak growth, official interest rates were raised in numerous EM. Turkey deserves a special mention: the authorities believe that the way to tackle inflation is to cut interest rates. As a result, the currency has tumbled and the economy has fallen into recession.

Covid has been the biggest peacetime challenge the world has faced in a century or more. The response by economic policymakers has been unprecedented in terms of speed and scale. That provided massive immediate support, but it is medical science that has turned the tide in the war against Covid. Ordinary people in DM have suffered greatly, those in EM even more.