The energy crisis

Higher energy prices, natural gas prices in particular, are denting consumers’ purchasing power. EU natural gas prices have increased close to 300 percent over the past year. Most governments have put in place measures to reduce the impact of high energy costs, ranging from capping consumer gas prices in 2022, as France did, to reducing taxes, such as was done by Italy and Spain, which reduced the consumer sales tax on energy. While this may take the sting from the vertiginous increase in prices, gas prices remain elevated and the risk is that consumers may well respond by cutting spending elsewhere.

The energy crisis is also having a major impact on inflation, which came in higher than expected in January. The headline harmonised index of consumer prices reached 5.1 percent. Energy prices were the main driver, as core inflation was a more subdued 2.3 percent for the euro area as a whole.

That energy is such an important element of the current surge in inflation is also visible in the large spread of national inflation, with France—which has capped energy prices—at one end of the spectrum with inflation of 3.3 percent and Lithuania (12.2 percent) at the other.

We expect inflation to continue to moderate throughout 2022 as the contribution of energy gradually normalises, though it now expects inflation to fall below the ECB’s two percent target later than previously anticipated—by 2023.

Fear and trepidation?

The last time the ECB tightened monetary policy, in 2011, after the global financial crisis, it caused significant volatility in financial markets and choked off the recovery. The central bank soon had to abandon its policy. Since then, important progress has been made aiming to strengthen regional institutions.

In particular, we think the establishment in 2020 of the €750 billion EU recovery fund points to a willingness to share fiscal burdens. Financed by borrowing on behalf of the EU as a whole, the fund is largely allocated to southern member countries as they have suffered the most from the pandemic. The Banking Union, established a decade ago, ensures that if a financial institution needs to be recapitalised after bond and equity investors have been tapped, the European Stability Mechanism, an intergovernmental organisation which provides financial assistance, can be accessed, so that the host country is no longer the sole recourse. Moreover, the banking system is now much stronger, as the banks, prompted by regulators, have taken steps to rebuild their balance sheets. Finally, the ECB has given itself more tools to manage volatility in financial markets.

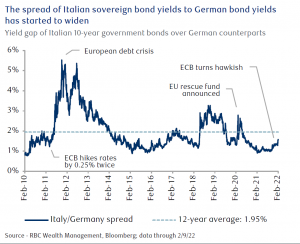

These structural changes suggest to us that the region should better withstand the upcoming monetary tightening cycle. Nevertheless, the ECB plans to keep a close eye on how its highly indebted member countries are impacted by its actions. Italian sovereign 10-year bond yield spreads relative to their German counterpart have already widened since the ECB meeting, though they remain much below their 12-year average.

Maintain Overweight

The 2022 global investment backdrop has already set out to be more volatile than last year’s. That also applies to European equities, particularly given the tensions between the West and Russia. Yet we continue to suggest holding an Overweight, or above-benchmark, position in this asset class. Given the prospect of above-average economic growth this year, we believe earnings growth expectations of around seven percent are undemanding, leaving room for upgrades. Valuations have improved and the MSCI Europe ex UK Index trades at a forward price-to-earnings ratio of 14.3x, below its five-year average. As for sectors, we think Financials appears well positioned to benefit from higher interest rates and the robust growth outlook, while the Industrials sector could also provide attractive opportunities given Europe is a leader in green technologies.