Macroeconomic Conditions Are Improving

Growth momentum decelerated sharply in April, yet the most significant disruption to production and trade activities has likely passed. Hard-hit Shanghai is reopening. Supply chain disruptions have dissipated, and production is resuming.

These developments should support a sequential rebound in economic reopening in the coming months. This is particularly true if the government refines its COVID restrictions, reducing transport and industrial production disruptions.

Uncertainties related to economic forecasts are high. COVID cases in China are declining because of the aggressive lockdown. Absent broader natural immunity, China risks locking down again if new cases ramp up with increased mobility.

Internet Sector Challenges Are Receding

Unlike previous years, when Chinese internet companies spearheaded earnings growth, we expect this year to be more broad-based. We continue to see opportunities in companies receiving strong policy support. We continue to favour areas along the green value chain and strategic investment areas, such as high-end manufacturing and technology self-sufficiency.

At the end of 2021, the Chinese internet space faced challenges resulting from rising uncertainty around regulatory, delisting and geopolitical risks. We are beginning to hold a more balanced view on certain stocks in this sector as significant uncertainties should start to subside. Over the year, we expect sentiment and fundamentals to improve within the Chinese internet sector.

Our Reasons for Optimism

We expect EM equities to perform better in the second half. Healthy earnings and a lower equity risk premium support this view, especially if Fed repricing is close to an end and inflation begins to moderate.

After the recent moves in equities and rates, we think EM equities have priced in much of the bad news. Valuations appear far more reasonable after the pullback.

Inflation may soon level off due to the transitory nature of the COVID impact and softening demand as growth slows. As the market prices in peak inflation and interest rates, the growth factor should return to favour.

We continue to favour a balance of cyclical and secular growth. We like traditional growth (e.g., technology, biotech, and innovation) and cyclical stocks (e.g., metals and mining). Telecoms and financials, particularly banks, are attractive. Banks look well-placed to benefit from higher margins on the back of rising rates.

Despite the top-down pressure on risk assets, EM companies exposed to structural growth drivers, such as the energy transition, digital transformation, and health care innovation, have continued to deliver strong revenue and earnings growth.

Second Half Looks More Promising

We expect to see opportunities in EM equities, especially if Russia and Ukraine reach a ceasefire. We note several constructive points if inflation peaks and cost pressures normalize, which would allow the market to focus on earnings rather than inflation and interest rate pressure.

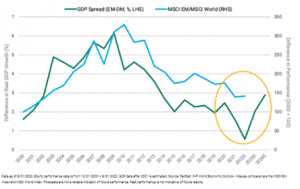

Relative growth rates, which have historically supported relative performance, favour emerging markets. This view is reinforced as the U.S. appears to be on an aggressive tightening path while China is expected to ease its path, and its internet regulatory cycle is nearing an end.

Figure 4 | Relative Growth Rates Support the Outlook for EM Equities

Emerging vs. Developed Economies: Real GDP Growth and Equity Performance Spread

Relative Valuations Favour Emerging Markets

Valuations are also attractive as equities have derated significantly this year. As of the end of May, the 12-month forward P/E of the MSCI EM was 11.57; 2021’s high was 15.6 (1/31/2021). That is a 26% decline. (Source: FactSet.)

Also, the relative valuations between EM and developed markets have cheapened significantly and are now more extreme than during the COVID outbreak in March 2020. (EM stocks are trading at a 33% discount to developed markets, relative to a 22% historical average discount.)

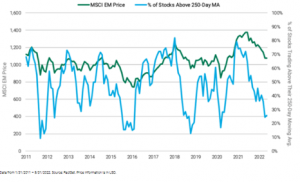

The market is beginning to price in much of the risks we have discussed. Figure 5 demonstrates how quickly emerging markets can rebound when valuations become significantly dislocated. We saw examples of this in 2012, 2017 and 2019.

Figure 5 | EM Price Momentum Has Room to Improve