Classification is key

There is, however, a key difference between ETFs and most other ETPs. As per UCITS regulations, the former are considered “collective investment vehicles”, while the rest are referred to as “debt instruments”.

UCITS guidelines require the index being tracked by an ETF to either comply with the diversification ratio applicable to its asset class or comply with the “20/35” ratio, where each constituent must have a weight below 20% of the total portfolio, but under exceptional circumstances, one single constituent weight can go up to 35%.

This means that, except for ETFs, almost every other exchange-traded vehicle gets labelled a “debt instrument”, including themed investment vehicles unable to comply with the “20/35” ratio and short & leveraged (S&L) single-stock vehicles.

Exchange-Traded Commodities (ETCs) – instruments that have either individual commodity assets or baskets thereof underlying them – are classified as “debt instruments”. There is a key similarity between ETFs and ETCs here: both are required to be fully collateralised, i.e. the issuer buys and holds the underlying asset in order to offer the product to investors.

Exchange-Traded Notes (ETNs), which have a broad and flexible structure, are also classified as “debt instruments”. They can (and sometimes do) comprise of instruments that are deemed difficult for many investors to access such as, say, currencies and even innovative mixes of commodities with equities.

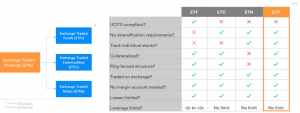

Broadly, here are the various features that delineate the different exchange-traded vehicles:

Market products don’t devolve neatly into these three categories: for instance, we call our offering “Exchange-Traded Products” because they combine major features of all three major instrument types: the products are physically-backed (like ETFs), fully collateralized (like ETCs) and are diverse with regard to leverage factors (like ETNs). Other issuers need not necessarily be designed the same way, despite having the same underlying and leverage factor, and term their products as ETPs as well.

Investors should consider the risks with the underlying of an ETP along with the specific features being offered by design that could affect the return profile. Using ETPs has the potential to deliver a wide variety of benefits in different market conditions to investors, which can outperform many broad-based ETFs over different periods if given due care and attention.