Global markets have shown remarkable resilience in the face of geopolitical turmoil, rising energy prices and increasing inflation concerns, according to Fidelity International’s (“Fidelity”) Mid-Year Outlook 2026: The Shock absorbers.

Despite a more fragmented world order and ongoing uncertainty in the Middle East, Fidelity believes strong corporate earnings, resilient economic fundamentals and continued investment in artificial intelligence (AI) should provide support for risk assets through the second half of the year.

Fidelity reveals its top convictions for the second half of 2026:We are constructive on equity risk overall, but particularly in Japan and select emerging markets. We remain mindful of the strong rally markets have seen since April.AI capex has been the driving force for global markets and is supporting other themes like energy scarcity and grid upgrades. Commodities particularly those that are linked to energy, can provide useful diversification for geopolitical risk when traditional assets such as duration and gold behave less reliably.

“Markets have proven impressively resilient against a volatile first six months of this year. But their steadfastness shouldn’t be surprising. They’ve become well-versed in seeing through the noise and recognising upside,” said Salman Ahmed, Global Head of Macro and Strategic Asset Allocation, Fidelity International. “Now is not a time to shy away from risk, only to ensure it’s balanced in a well-diversified portfolio that will cushion the inevitable shocks when they come.

“While recent diplomatic progress between the US and Iran may help ease some immediate concerns, uncertainty remains elevated and the path ahead is unlikely to be straightforward.

Global macro-outlook and navigating the second half of 2026

“The key macro variable for the near future is the energy supply shock caused by the closure of the Strait of Hormuz.

“Our base case has been a ‘messy resolution’ to the conflict. The proposed deal to reopen the Strait of Hormuz and extend the ceasefire, points towards de-escalation, however, there remains a meaningful range of possible outcomes. Markets are likely to continue pricing some geopolitical risk premium until a durable resolution becomes clearer.

Higher inflation and tighter monetary policy will drag on growth across most regions; energy markets will maintain a persistent geopolitical risk premium.

A constructive environment

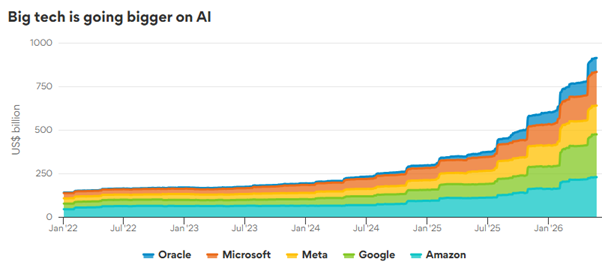

“Resilient fundamentals are supporting markets, despite geopolitically-induced volatility. Most significantly, US tech behemoths are continuing to pour billions into AI development that is driving continued earnings momentum.

Source: Fidelity International, Bloomberg, May 2026. Charts shows Bloomberg consensus estimates for 2-year blended forward capex.

“That immense capex spend is bolstering companies across the value chain, including the industrial enablers that support the building of datacentres and rising energy needs.

“A wider set of US businesses are also starting to feel the impact of that AI-driven capex spend underpinning earnings and improving productivity. This broadening effect across the market presents enticing entry points while attention is focused on a small number of high-valued tech names.

“The earnings story remains strong globally, driven in part by AI capex, but also due to the partial unwinding of trade tariffs and resilient economies.

The emerging markets split

“That uncertainty also means it’s important to be selective when allocating across regions.

“We are underweight European equities, which are more exposed to supply disruption and the prospect of stagflation. Meanwhile the AI trade and strong earnings are supporting US stocks, though parts of that market have already run a long way.

“Japanese equities continue to look attractive, with earnings strong and the policy backdrop favourable.

“Emerging markets (“EM”) remain a high conviction allocation for us. EM equities benefit from broader tailwinds such as the AI cycle. A softer dollar and structurally improving policy credibility should also be positive drivers.

“However, the conflict in Iran is having a divergent impact across the EM universe. Those that export commodities in Latin America are benefitting; those that import energy, particularly Asian economies that are reliant on supply that passes through the Strait of Hormuz, are suffering.

“So, a discerning approach by EM investors is required. Brazil for instance is one beneficiary from increasing energy prices with equities that are attractively valued and could do even better from an easing policy cycle. South Africa boasts attractive domestic fundamentals and commodity support. Parts of Asia Pacific too are compelling despite energy disruption – Korea, supported by the semiconductor cycle and corporate reform momentum, is one such example.

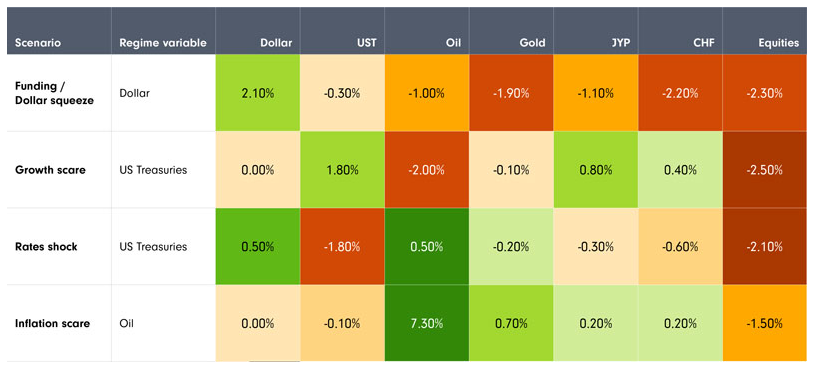

Rethink safe havens

“As the macro environment changes, so does the way we think about diversification. Heightened geopolitical and fragmentation risks are putting a strain on traditional safe havens, which means investors can’t rely on a single asset to support riskier elements of their portfolio. We have moved from a world that was defined by occasional growth scares into one of more structural instability. Varied sources of defence are necessary.

“The dollar, for instance, does not look as attractive for the long term as it once did. Gold has performed surprisingly poorly through the conflict but we remain positive on the commodity, owing to its supportive underlying drivers. It can perform strongly when inflation hurts bonds and serves as a diversifier when correlations between bonds and equities increase. Likewise, it can respond well to dollar weakness and falling real yields.

Safe-haven assets perform differently across market sell off regimes

Past performance is not an indication of future results

Source: Fidelity International, Bloomberg, April 2026. Based on weekly returns from January 1977 – April 2026. Dollar: DXY Index. UST: returns implied from the 10y US Treasury index. Oil: Generic 1st Crude WTI, backfilled with Bloomberg Commodity index prior to 1990. Gold: XAU Curncy. JPY: JPYUSD Curncy. CHF: CHFUSD Curncy. Equities: MSCI World Index, backfilled with S&P 500 Index prior to 1999

“Exposure to commodities should support portfolios with inflation set to remain higher for longer, particularly those with energy exposure that can protect against geopolitical risk.

“They can also provide a hedge while duration suffers. Inflation reduces the scope for yields to fall materially and therefore diminishes the upside for duration, hence its poor recent performance. Were growth fears to re-emerge later in the year then duration would reprise its role as an equity hedge.”