Funds under management ended the year at £1,509 billion in 2024, an increase of 6% since the end of 2023, while net retail outflows fell to £1.6 billion, according to data published by the Investment Association (IA) today.

The year’s figures demonstrate a cautious return to investor optimism for 2025, helped by falling inflation, rate cuts by central banks and stronger equity market performance, particularly in the US. Investors also continued to back bonds in 2024.

Key findings for 2024

- Index tracking funds, a clear success story of 2024, took in a record £28.0 billion, exceeding the previous record inflow of £18.4 billion in 2020. Index tracking funds now account for a quarter of funds under management.

- Equity funds continued to see overall outflows through 2024, though at £5.7 billion outflows were significantly reduced from the £22.4 billion outflow in 2023. The overall outflow was driven by active equity funds as equity index trackers took in £20.6 billion. UK equity funds outflows weighed on equity net sales with £13.1 billion in outflows (£13.6 billion, 2023), while funds investing in North American equities, the top selling equity region, saw inflows of £3.3 billion in 2024.

- Fixed income funds had a positive year, which saw inflows accelerate in 2024, to £3.2 billion, up from £720 million in 2023. Investors increasingly opted for corporate bond funds in 2024, with net inflows of £4.6 billion following flat sales in 2023.

- Mixed asset funds saw outflows of £2.7 billion through 2024, only slightly easing from the £4.0 billion in 2023. The Mixed Investment 20-60% Shares sector continued to drive outflows, with investors taking out £3.8 billion.

- Responsible investment funds struggled, seeing significant outflows continue through 2024, with net withdrawals of £4.7 billion, up from £3.0 billion in 2023.

Trackers gain momentum

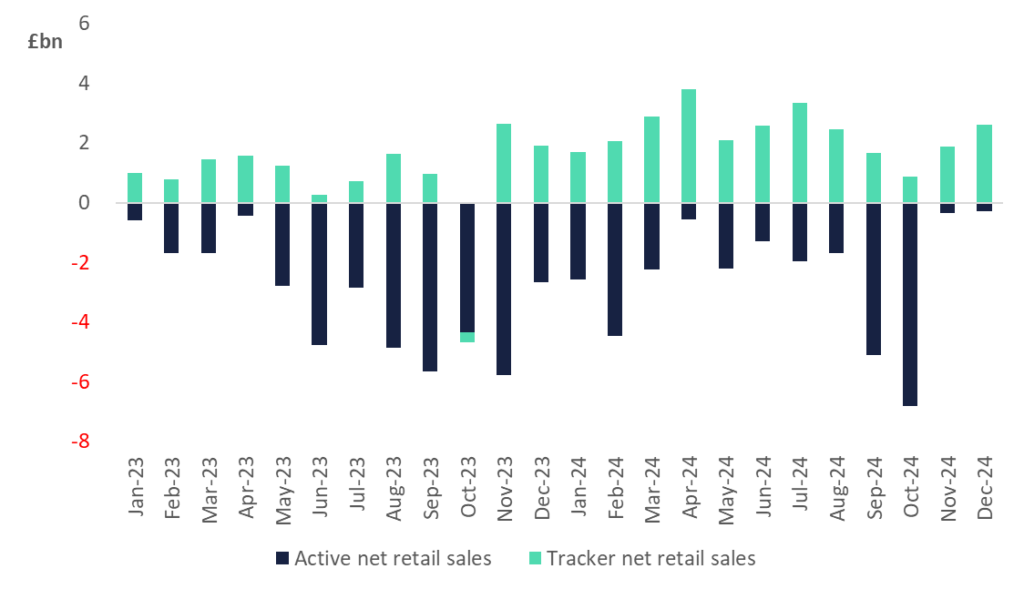

2024 saw a more positive year, with inflows in seven out of the twelve months and index trackers firmly in favour with investors. The net retail sales monthly average for 2024 until August was £491 million, buoyed by one of the highest April inflows around ISA season in recent years at £3.24 billion. The September and October outflows (£9.4 billion) in the run up to the Budget have nudged the 2024 net sales total into negative territory, despite a rebound to inflows in November and December.

Money flowed into index trackers across the year, with record inflows of £28 billion in 2024, £9.6 billion higher than the previous record year of 2020 (£18.4 billion). Index tracking funds now account for a quarter of UK investor funds under management, up from 18% in 2020.

Inflows to index trackers were boosted by sales of £20.6 billion to funds tracking equity indexes, up from £8.7 billion in 2023. Investors returned to equities as inflation eased, and central banks embarked on a rate cutting cycle.

Sales to Global and North American index trackers were strong as investors sought exposure to the large technology stocks that have propelled the performance of US and Global indices forward. Global trackers took the largest share at £10.2 billion, up from £4.3 billion in 2023, followed by North American trackers, which saw inflows of £3.8 billion – an increase from £3.0bn in 2023.

Since 2018, UK investors have placed significant capital into low-cost trackers, looking for cost effective exposure to global equity markets, and increasingly to bond indices. In 2024, the dominance of US equity market returns both on global indices, where the MSCI World has a 74% allocation to the US, and the US indices such as the S&P 500 attracted investors back into equity trackers. Advisers and wealth managers are also looking at ways to bring costs down for investors and are allocating a higher percentage of portfolios to index trackers.

Active & tracker retail sales

Miranda Seath, Director, Market Insight & Fund Sectors at the Investment Association, said:

“At the end of 2024, flows to US equities were bolstered by the strong response of the US market to Trump’s US election victory. Investors viewed a Trump presidency as broadly positive news for the performance of US companies and the large US listed technology stocks. This has driven sales to the IA’s North America and North America Smaller Companies sectors. Outflows from UK equity sectors also eased in November and December – the question is whether we’ll reach the tipping point back into inflows in 2025.

“Looking ahead, the outlook for UK equities is relatively good, UK stocks are seen as good value, the UK political agenda is clear and the pro-growth agenda set by the Government is a positive statement of intent.

“While there may be significant opportunities for investors in 2025, the febrile global geo-political environment could introduce more volatility. For example, after the initial announcement of US tariffs for Mexican, Canadian and Chinese goods, it’s still uncertain when and how high Trump will set final tariffs. Tariffs would be detrimental for both global trade and may introduce investor caution over sectors, such as emerging market equities. It is also unclear what impact tariffs will have on the US economy. The S&P 500 fell by 1.5% on the first trading day following the recent tariff announcement. The dollar has strengthened, and tariffs are likely to push up the price of goods and components from outside the US, which will have some impact on consumer prices and manufacturing, and therefore on inflation. With a more uncertain outlook, the Federal Reserve could pause the rate cutting cycle.

“Whilst returns may be choppier across equity markets around the world, it could bring some interesting opportunities for investment managers to drive performance. With such distinct short and long-term structural changes witnessed across global markets in recent months, what will remain true in 2025 is that markets won’t stand still. The key message therefore to investors is to stay invested through periods of volatility and to think long-term. The UK investment management sector is critical to support this, by empowering investors to access capital markets and improve their financial futures.”