This decade the gilt market has suffered three major convulsions (to date). The first of these in 2022, the Truss/Kwarteng “giltmageddon”, was a truly toxic combination of a political crisis, an inflationary shock, a currency crisis and a pension crisis all motivated by debt sustainability concerns.

The next convulsion in summer 2025 played out against a less chaotic political and inflationary backdrop, however debt sustainability concerns were so acute that long bond yields rose to higher levels than their 2022 peak. The third convulsion, experienced this quarter, was caused by the Iran war energy shock and associated inflationary concerns that pushed the 10 year gilt yield to 5%, its highest level since 2008.

“It is notable that the frequency of gilt crises appears to be increasing. Excessive debt and anaemic economic growth has left the UK economy extremely vulnerable to adverse economic developments. As there is no political will to enact expenditure cuts on a scale required to consolidate debt, successive governments stagger helplessly from one crisis to the next.

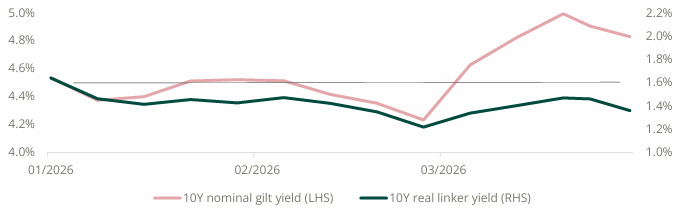

“However another notable feature is that index linked yields have fallen over the quarter even as nominal yields have risen. As inflation fears have been the principal cause of this recent sell off investors have been prepared to pay more for inflation protected bonds, particularly at the short end of the curve where our funds are positioned.

“Many investors turned away from index linked bonds after their poor performance in 2022. However since 2022 linkers have repriced to much more defensive levels and are now acting in a much more reliable fashion. All of our bond funds have made modest gains over this quarter despite the rising nominal yield environment.”

10Y Nominal vs Index Linked Gilt Yields during 2026

By Emma Moriarty, Portfolio Manager at CG Asset Management