The focus of stimulus has also been different. During the GFC, most of the fiscal support went to financial institutions. Arguably, the need to nurse financial institutions back to health made the recovery from the GFC weaker and enabled deflationary pressures. One school of thought is that monetary policy affects inflation via credit channels. The need to recapitalize financial institutions meant monetary policy in the wake of the GFC was unlikely to be inflationary.

During the COVID-19 crisis, most of the stimulus has gone to households. The COVID-19 crisis was very different in that financial institutions were comparatively healthy going in. Instead of needing to rebuild banks, monetary authorities could use banks to help channel credit to sectors that needed it most. The outsized nature of the monetary and fiscal impulse deployed during the COVID-19 crisis and the fact that this response was used in a health crisis and not a financial crisis—has summoned investors’ inflation fears. These fears have been fed by how the U.S. dollar has depreciated, by how real yields have fallen deeply negative, and by how the U.S. current account and budget deficits were negative and have gotten worse.

What does the market think?

Markets process vast amounts of information, and it is generally a good idea to start with the collective wisdom of the markets in forming one’s own views. Then we can determine if there is something from the market narrative that is missing or distorted to determine if we have an empirically based reason to have a difference of opinion.

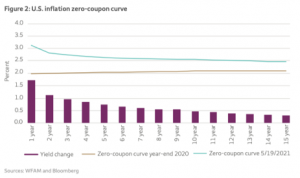

Market expectations around inflation are embedded in the inflation forward curve. Figure 2 compares the inflation zero coupon curve in the U.S. at the end of 2020 with mid-May 2021.

As can be seen, the front end of the forward curve has reacted much more sharply than the back end of the curve. This was driven by recovering growth expectations, a weaker U.S. dollar, short-term supply constraints, and stronger commodity prices. Similar to major central banks’ views, markets are pricing a transitory increase in inflation while the longer-term structural view on inflation is well contained. Front-end inflation expectations are back to the 2010–2012 highs while the long end is still 50 basis points below post-GFC levels. Hence, we see a scenario of reflation that signals inflation should be accompanied by plenty of growth.