Productivity

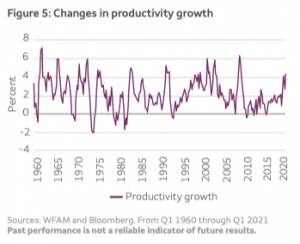

Faster productivity growth, which is the ability to produce more with a given quantity of inputs, is positively correlated to lower inflationary pressures. Productivity growth was very low after the GFC. During the COVID-19 crisis, we likely had a few years’ worth of technology adoption crammed into a few months due to forced technology adoption and quick changes in consumer and business behaviours as people adapted to a stay-at-home and work-from-home world. Relatively high productivity growth, as shown in Figure 5, contributes to our view that inflation should be elevated for only the next 12 to 18 months before bottlenecks clear.

In this case, the input to watch is labour. To the extent we can see the number of people unemployed drop quickly, there are possibly years of productivity benefits to be harvested. That could mean faster growth against a backdrop of strong profit margins with inflation migrating back to central banks’ targets.

What should investors think about now?

As multi-asset investors, our research has shown that a strategic allocation to what we call “inflation assets” can improve the expected risk-return behaviour of a diversified portfolio. Most investors can benefit by maintaining a strategic allocation over a business cycle, congruent with their unique long-run return objectives and risk tolerance. While our research suggests that heightened inflationary pressures should decline within the next 12 to 18 months, we think investors can make tactical moves to harness near-term shifts in sentiment. The latest transition from a rapid COVID-19 recovery that benefited growth assets has shifted toward a rally in inflation-sensitive assets. That dynamic occurs when the market is changing its focus from early recovery to a mid-cycle stage of the economic cycle. In this environment, we prefer assets whose cash flows adjust upwards with inflation or whose valuations improve relative to other assets when there is inflation. Using this lens, the following assets may benefit through what we believe is a reflation (growth plus a temporary increase in inflation) cycle:

• TIPS: though short-term maturity with lower real interest rate sensitivity

• Commodities: energy and precious metals tend to do well

• Spread products like high yield, corporate bonds, or loans: which have lower interest rate sensitivity than long-duration government bonds and an additional spread component as a return buffer against higher rates

• Equities: particularly the lower-duration part of the equity market (cyclical and value oriented) and emerging market equities

• Alternative strategies: trend following, carry and value tend to do well during a reflation cycle

There are clearly risks to the inflation outlook. In this note, we discussed a few key variables we are watching that are shaping our views. We also offered some insight into our approach to tactical positioning in this environment. Above all, a key insight we hope that readers take away from this discussion is that the outlook for inflation, or any systemic risk for that matter, is dynamic and evolving. An informed view must remain adaptive. To this end, we hope we’ve provided some useful tools herein for refining your own outlook.