By Frédérique Carrier, Head of Investment Strategy in the British Isles and Asia at RBC Wealth Management

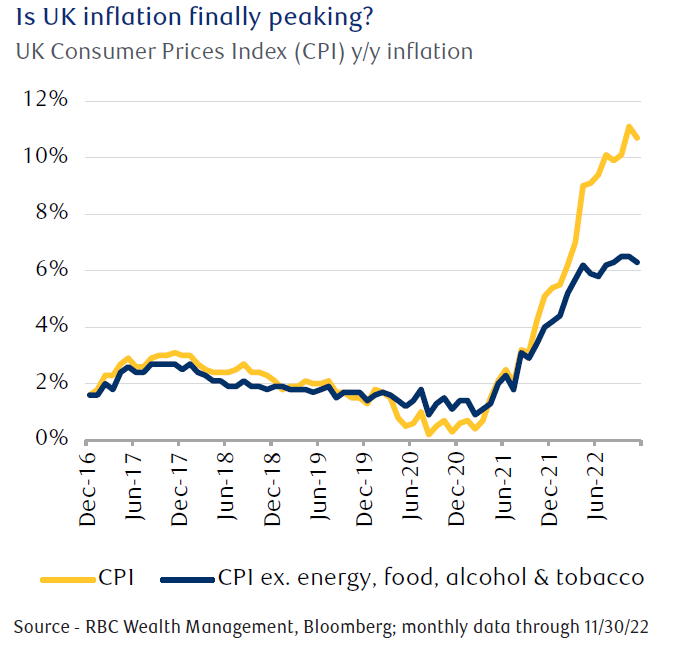

November inflation in the UK ticked down and was below expectations. Unlike in the U.S., where inflation is now much below its June peak, UK inflation remains stubbornly elevated, reaching 10.7% y/y compared to the 41-year high of 11.1% y/y a month earlier.

Encouragingly, with half of the main consumer price inflation categories making downward contributions, including alcohol and tobacco, clothing and footwear, and recreation, consumer price inflation may have peaked. Households and businesses struggling with the cost-of-living crisis will hope that is the case.

Facing double-digit inflation in Europe, the Bank of England opted to increase the Bank Rate 50 basis points (bps) to 3.5%, the highest level since 2007, at its last meeting of 2022. A tight labour market, partly due to a labour shortage after the pandemic and Brexit, likely influenced its decision, in our view. For now, RBC expects rates to peak at 3.75% in Q1 2023 and to be maintained at that level throughout the year.

In Europe, the European Central Bank (ECB) increased the deposit rate by 50 bps to 2% and signalled the need for further rate hikes to tame inflation. With staff projections for inflation in 2023 exceeding 6%, ECB President Christine Lagarde delivered a very hawkish message, suggesting interest rates would have to continue to “rise significantly at a steady pace” to ensure they prove sufficiently restrictive for inflation to return to the 2% target. We think that statement suggests two further 50 bps hikes are possible.

Messaging around its balance sheet reduction was more subdued. The ECB announced that as of next March, it will no longer reinvest maturing bonds that were issued as part of its asset purchase programme.

The ECB is making interest rates its main inflation-fighting weapon. The risk remains that in an effort to shore up its credibility, the bank will raise rates too aggressively, which would deepen the expected recession.