Fixed income ETF inflows set to continue amid Trump and central bank policy uncertainty. Yields continued to rise early in the month, before bond markets rallied strongly following better-than-expected inflation data.

At $4.8bn, flows into fixed income ETFs were respectable despite it being the slowest January for three years. Uncertainty about Trump’s policy agenda and central bank policy are likely to continue to drive inflows into ‘safe-haven’ assets in the near-term.

Paul Syms, Head of EMEA ETF Fixed Income and Commodity Product Management at Invesco, comments:

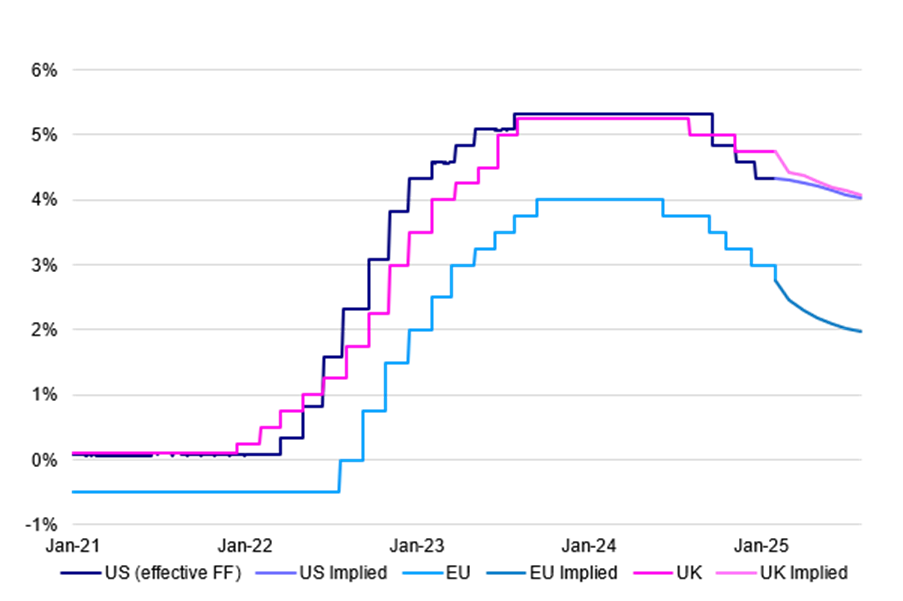

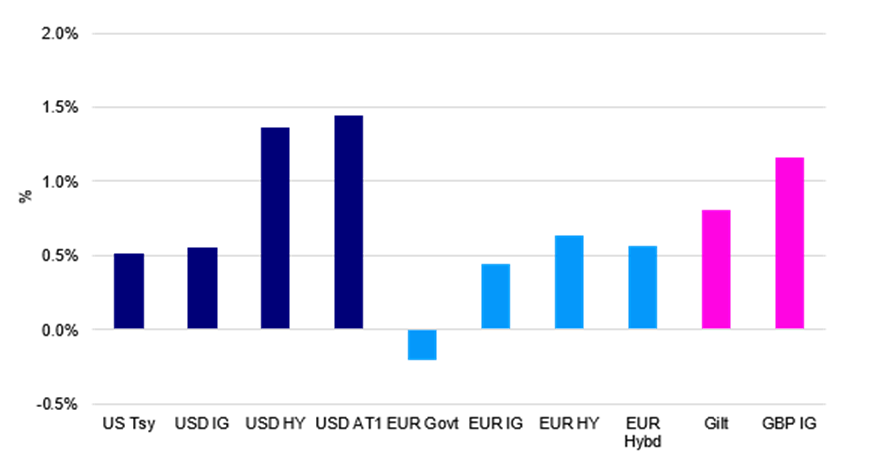

“Although January was a rollercoaster ride for bond markets, yields generally ended the month slightly lower, which led to positive returns for most fixed income asset classes. Yields continued to rise in the first half of January, following the trend seen since the middle of November, as stronger data and less dovish central bank commentary caused investors to push back expectations on further rate cuts. In particular, the closely watched US employment report showed the change in non-farm payrolls beating expectations while the unemployment rate ticked lower.

“There were some region-specific events that also drove markets. The focus in the US, as well as globally, was on Trump’s inauguration, his policy agenda and its potential impact on growth, inflation and Fed policy. Meanwhile, in the UK there were concerns about the outlook for growth and implications for the deficit following last October’s Budget. However, the lower-than-expected core inflation prints from both the US and UK mid-month triggered a change of sentiment towards bond markets which proceeded to rally in the second half of the month. Following 100bps of easing in the last four months of 2024 and indicating that few rate cuts were likely at their December meeting, the Fed held rates steady at the end of the month, with the statement leaning more hawkish. The ECB, however, continued to ease policy with a further 25bp rate cut.”

Asset class returns – January 2025

Fixed Income ETF Flows

“While flows into fixed income ETFs in January were respectable, at $4.8bn it was the slowest January for three years. Interestingly, while the yield on the benchmark 10-year US Treasury reached its highest level in over a year, flows indicated significant uncertainty about the outlook. This led investors to have mixed views on whether to add duration or wait for a better entry level.

“Government bonds ($3.4bn) was the strongest category for net inflows, of which $0.5bn went into sub-1yr maturities. Cash Management ($1.6bn) and Fixed Maturity ($0.4bn) were the next strongest categories with Aggregate ($0.4bn) the only other category experiencing material inflows. Outflows were led by Investment Grade (-$0.8bn), potentially on concerns that spreads are trading at historically tight levels. Emerging Market Debt (-$0.3bn) and High Yield (-$0.2bn) also experienced net selling while in the “Other” category (-$0.3bn), outflows from a curve steepening exposure in US Treasuries were partially offset by inflows into CLOs, Smart Beta and Green Bonds.”

Top Fixed Income ETF Categories in January 2025

Outlook

“Having briefly risen above 4.8% in the middle of the month, the 10-year Treasury rallied strongly in the second half of January to end the month at 4.54%, a marginally lower yield than at the end of December. It seems that, following yields across bond markets hitting the highest levels for several months, it only took the slightly better inflation data in the UK and US to cause sentiment towards bond markets to turn more positive. Indeed, as markets are now only pricing in a shallow easing cycle from central banks in 2025, it has left bond markets looking more attractive overall. However, while developed market government bonds appear to offer value at current yields, deficits remain high, and curves could continue to steepen even if central banks slow the easing cycle.

“Meanwhile, credit spreads are trading at historically tight levels, although there are many reasons for spreads to remain tight; corporate balance sheets are broadly healthy, the probability of recession is low and overall yields are high. But it is difficult to expect spreads to tighten much further, so the appeal of credit markets in the months ahead is likely to be primarily driven by the additional carry they offer over government bonds. Given current valuations, it appears prudent for investors to add duration through government bond markets when yields rise, while taking advantage of the carry available in credit markets, but with a lower duration exposure. However, uncertainty about the outlook, particularly as Trump announces new policies, means that being nimble is likely to be key in the months ahead.”

Positioning

“January largely saw a continuation of the theme seen throughout last year with fixed income investors remaining cautious and favouring allocations to either government bonds or cash management products. In the short term, with heightened uncertainty, flows into ‘safe-haven’ asset classes appears likely to continue. However, central banks are likely to ease further in the months ahead and, as yields and therefore expected returns on cash decline and yield curves steepen, investors are likely to start locking in yields currently available in bond markets by rolling along the yield curve in coming months.”

US, EU and UK rates and rate expectations