UK retail investors pulled £752 million from funds in July, reversing the inflows of £208 million recorded in June, according to data published by the Investment Association (IA) today.

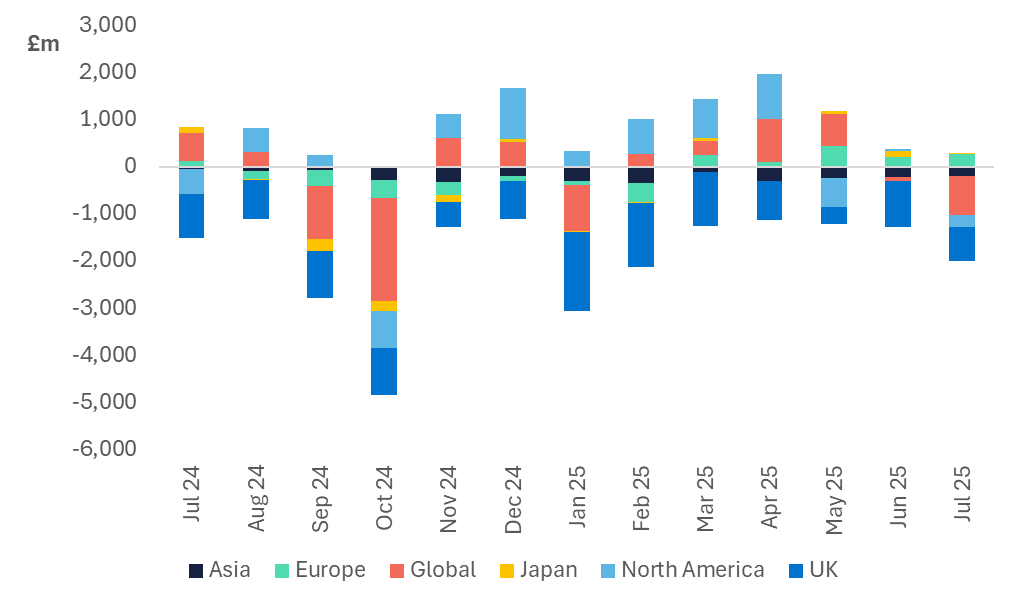

The shift was driven by £1.8 billion of equity outflows across Global, UK and North America funds. This came despite US equity markets rebounding from the April performance dip – the performance of US equity markets is a significant driver of global equity returns, but we saw rising outflows from global equity funds in July, albeit from actively managed funds (index trackers in the IA Global sector saw inflows of £539 million).

UK equities also remained in outflow territory, with £718 million of redemptions. This continued selling suggests investors are taking a more cautious stance toward UK equities, potentially in anticipation of the upcoming budget and its implications for taxation, spending, and broader economic growth. In contrast, Europe has continued to remain attractive with inflows of £276 million as investors seek diversification away from the US supported by opportunities in infrastructure, energy transition, and defence, which are increasingly viewed as structural growth areas.

Ongoing global trade tensions and the longer-term economic implications of higher tariffs may be prompting investors to take risk off the table. The start of July marked the end of the 90-day pause on US reciprocal tariffs and high inflows into short-term money market funds suggests that investors are waiting to see how market conditions will change.

UK retail investors placed £1 billion into money market funds in July, and the Short-Term Money Market sector topped the list of best-selling IA sectors. The sustained demand suggests investors are awaiting greater clarity for longer-term allocation and are using money market funds to park capital temporarily.

Additionally, mixed asset funds extended their consistent run of inflows from H1 2025 into the second half, with continued inflows into 40–85% share strategies. These funds appeal to investors by offering diversification alongside the security of active asset allocation decisions being taken by the investment manager, an attractive combination during periods of uncertainty.

Key findings for July 2025:

- Equities saw heavy outflows of £1.8 billion in July, doubling outflows from £912 million in June. European equities were a bright spot, attracting £276 million in July – a fifth consecutive month of inflows.

- Fixed income fund flows were broadly flat with net inflows of £66 million in July, down from £157 million in June, although the UK Gilts sector (£156 million) and Mixed Bond funds (£215 million) attracted inflows.

- Money Market funds saw their sixth consecutive month of inflows at just over £1 billion in July, an increase on £823 billion in June.

- Mixed asset funds recorded the ninth successive month of inflows of £198 million, although the 40–85% share sector was the only mixed asset sector to record an inflow of £285 million in July.

- Tracker funds reached inflows of £711 million, the lowest monthly net sales since October 2024, with allocations into tracker funds in the Europe ex-UK sector (£276 million) and the IA Global sector (£539 million), the highest. Funds tracking fixed income indices saw inflows of £205 million.

Net retail sales by equity region, July 2024 – July 2025

Miranda Seath, Director, Market Insight & Fund Sectors at the Investment Association, commented:

“The return to outflows at the start of July highlights the continued pressures faced by investors trying to balance the risks and opportunities of market volatility, geopolitical tension and uncertain trade relationships. These factors have driven investors to depart from equities in July, but we have yet to see if this will be a sustained trend or a temporary adjustment as investors continue to ponder their portfolio positioning, remaining firmly in ‘wait and see’ mode.

“While investors pulled away from North America equity funds, and to a certain extent Global equity funds – although Global index trackers sales held up – flows to European equity funds have been consistent in 2025 and in July, Europe was the only region to see notable equity inflows. The agreement of the EU-US trade deal at the end of the month means that two of the largest global trading blocs have set a clearer course: investors tend to appreciate greater certainty, which could help to open up selective opportunities for those interested in European assets.

“Widening government deficits in Europe, the US and the UK are firmly in the spotlight in September and bond investors are pushing up long-term borrowing costs by demanding a higher risk premium on government bonds. In the UK, as the Chancellor’s fiscal headroom evaporates, speculation about tax changes is mounting ahead of this year’s Autumn Budget. In the very near term in the UK, investors have seen a recent rate cut, pushing down rates on cash savings and rising inflation. This could push more money into investment funds. The steep rise in the value of physical gold suggests that institutional investors perceive that risk is rising- investors buy gold to hedge risk. If we follow this logic through to funds, it suggests that investors could de-risk as we head towards a late November Budget.”