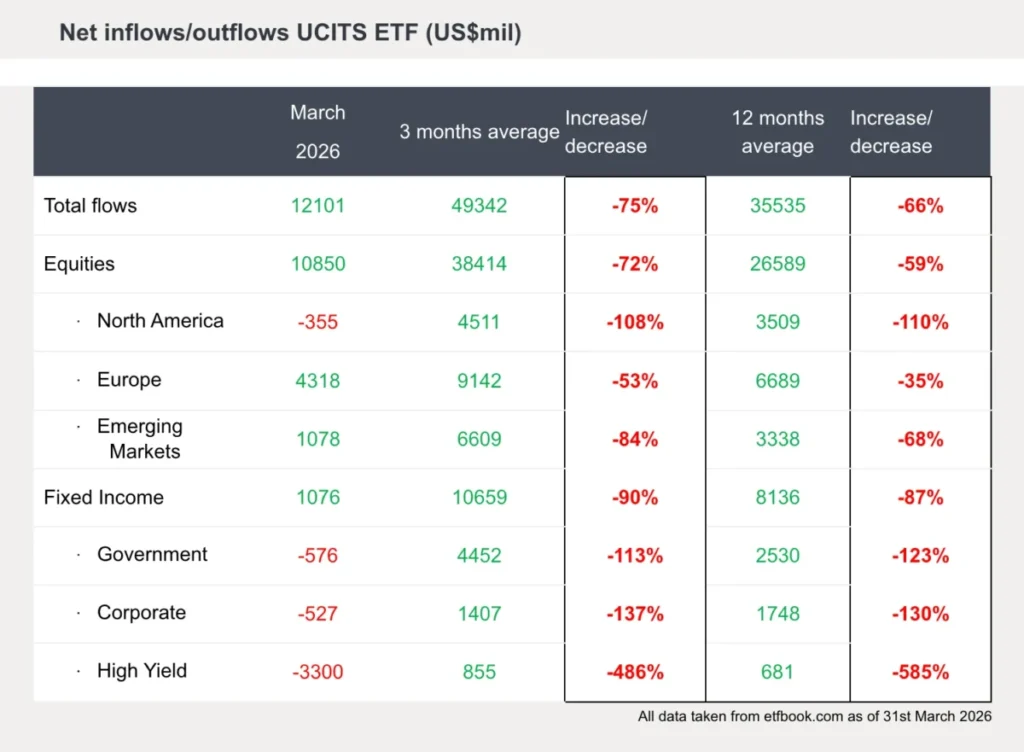

In March 2026, the European ETF market* was unable to escape the markets’ risk-off sentiment. With net inflows of USD 12.1 billion, investor demand fell to its lowest level since April 2024 – a clear break from the strong start to the year.

Nevertheless, the ETF market continues to record steady inflows overall, underlining its resilience and Q1 still represented a record quarter for ETF flows despite the market turbulence. Meanwhile Active ETFs are on for a record year if they continue the trajectory based on Q1 flows.

“The Iran conflict is increasing uncertainty – and that is clearly visible in the numbers. ETF investors are still investing, but more selectively: less risk, more liquidity and more defensive building blocks, and more actively. Active ETFs represented 24% of all flows for the quarter up from a medium-term average of 7-8%” says Max Dawe, Director, ETF Strategist, Fidelity International.

Against the backdrop of a generally weaker month, equity flows showed a clear regional bias. US equity ETFs recorded net outflows, while Europe and emerging markets still attracted inflows. What stands out is that momentum slowed markedly in emerging market ETFs. This fits with an environment in which geopolitical risks and energy price shocks are not pushing investors entirely out of risk assets, but are putting greater pressure on higher-risk regions and beta exposures.

“March was not a classic crash month, but rather a month of recalibration. Whether the recent easing of tensions around Iran will revive the trends seen in previous months remains to be seen,” Dawe adds.

Bonds: Defensive positioning instead of a classic flight to bonds

Overall, bond ETFs remained slightly positive in March, but the underlying picture is clearly defensive. A large share of new investments flowed into ultra-short-term bond ETFs, which attracted around USD 5.4 billion during the month.

“Investors used these products specifically as a temporary parking place for liquidity, not as a sign of increased conviction in the bond market,” Dawe explains.

At the same time, riskier segments saw substantial outflows. High-yield ETFs were under particular pressure, while traditional government and corporate bond ETFs also failed to attract stabilising inflows. This points less to a classic ‘flight to safety’ and more to broad-based risk reduction.

“Investors are cutting credit and duration risk and remain flexible as long as geopolitical uncertainty, inflation risks and the future path of interest rates remain difficult to assess,” Dawe concludes.