In this article, Naomi Fink, Chief Global Strategist at Amova Asset Management, explores how external shocks are feeding into Japan’s domestic economy, amplifying inflation pressures and complicating the Bank of Japan’s policy outlook.

In March, we argued that the risks associated with the Iran conflict shock may run deeper than markets assume. Since then, the market has been buffeted by headline‑driven shocks, swinging between apparent signals of de‑escalation and renewed conflict escalation concerns.

We also pointed out in March that these external shocks complicate Federal Reserve and Bank of Japan (BOJ) policy paths. Given recent developments, the BOJ’s policy path looks increasingly complex.

Although the OIS market has all but priced out a rate hike at the BOJ’s April Monetary Policy Meeting, we believe that Japan’s central bank has reason to upgrade inflation forecasts and clearly signal imminent further removal of policy accommodation. Failure to do so could invite market perceptions that the BOJ is falling “behind the curve” amid the ongoing oil shock, which appears to have evolved into a terms-of-trade shock for Japan.

Given the yen has already weakened substantially and 10-year Japanese government bond (JGB) yields have been on a steady uptrend, market participants may be looking to the BOJ for clearer policy guidance. Against this backdrop, the April meeting offers the central bank a chance to reduce policy uncertainty.

From external shock to domestic transmission

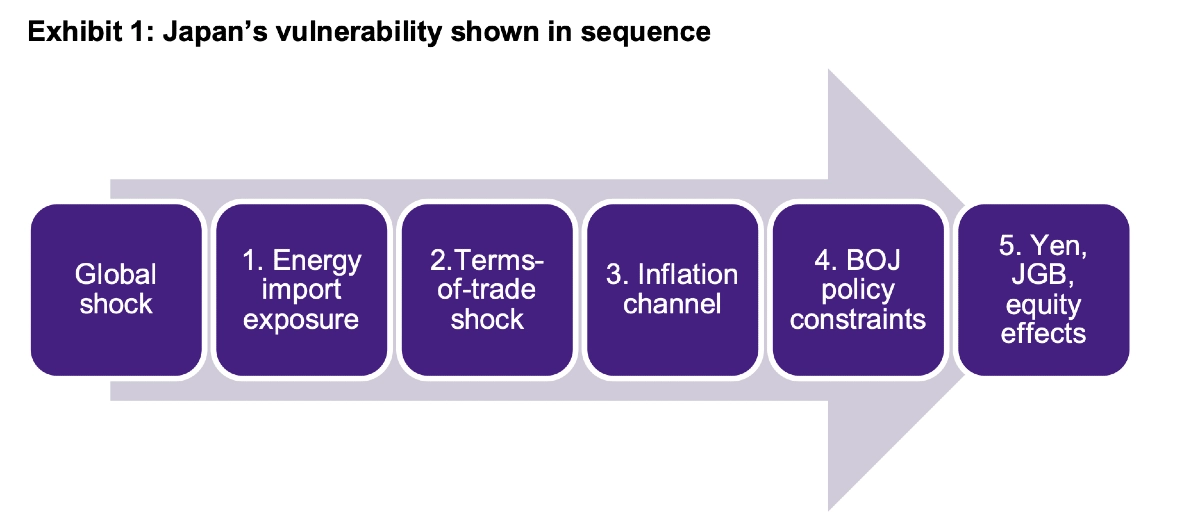

In March, we outlined Japan’s vulnerability to the ongoing global shock as a sequenced transmission process, in which each state is contingent on the last, rather than driven by oil prices alone. We framed the risk as a terms-of trade and inputcost burden shock, with oil prices only one among several interdependent factors, alongside cross-market spillovers.

Based on the following framework, we have compiled a diagnostic that puts Japan beyond the initial terms of trade shock stage and into a phase of macro amplification, specifically through the inflation channel (stage 3, shown below).

Where are we today? The macro transmission channel

Energy and logistics stress persists

Energy/logistics stress persists: Oil prices have retraced some of the spikes seen in March, with Brent and WTI easing from recent highs.

However, transport channels remain strained, with traffic through the Strait of Hormuz continuing to face disruption and anticipated reopenings failing to hold. LNG prices, as measured by the Japan-Korea Marker, still remain 35% above early-year levels, according to Bloomberg. Global shipping costs have also risen: the Baltic Dry Index surged by 56% between late January and 17 April, also according to Bloomberg.

Import price acceleration

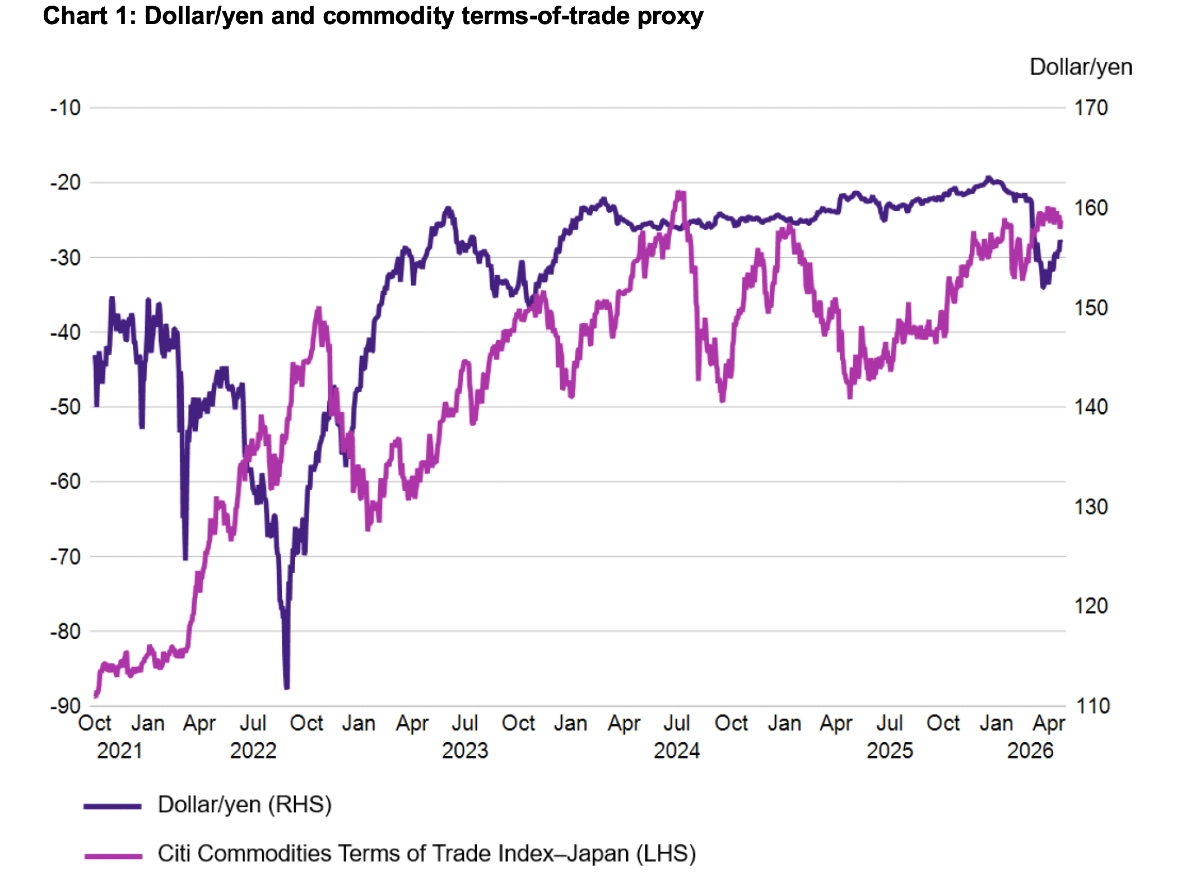

Japan’s import price index rose 7.9% year-on-year (YoY) in March, an acceleration from previous months. This has been accompanied by a deterioration in a proxy indicator of Japan’s commodities terms of trade (see Chart 1). The drop in the commodities terms of trade is indicative of an external income drain for Japan, all else equal, in the absence of an offsetting lift in export revenues.

At the same time, the energy import bill is worsening. Recent profit warnings by Japan energy importers cited higher LNG procurement costs and expenses associated with securing spot cargoes from non-Persian Gulf suppliers.

Household real income remains under pressure despite firm wage momentum:

Although the “Shunto” spring labour negotiations point to strong wage increases and household consumption showed resilience as of Q4 2025, the key question remains whether wage increases can outrun inflationary pressures.

The government announced its largest fuel subsidies since the scheme began in 2022, but such fiscal measures are, by design, temporary. They are intended to alleviate immediate price pressures rather than contain inflation expectations.

Corporate margin/fundamental impact has been confirmed:

Although the TOPIX has gained roughly 4.5% over the past three months, the breadth of the rally has been narrowing. Meanwhile, more than 60% of Japanese companies surveyed by Tokyo Shoko Research plan to raise prices to cope with higher oil costs, with a majority expecting costs to increase by more than 20% YoY if oil prices remain above USD 100.

Japan’s chemical producers are straining to keep ethylene plants operational given the disruption to naphtha supplies. The Reuters Tankan confidence index fell by 11 points to 7 in April, the steepest monthly decline in over three years and the largest fall since January 2023, when Japan was last in the midst of a terms-of-trade shock.

Yen amplification: alive and volatile

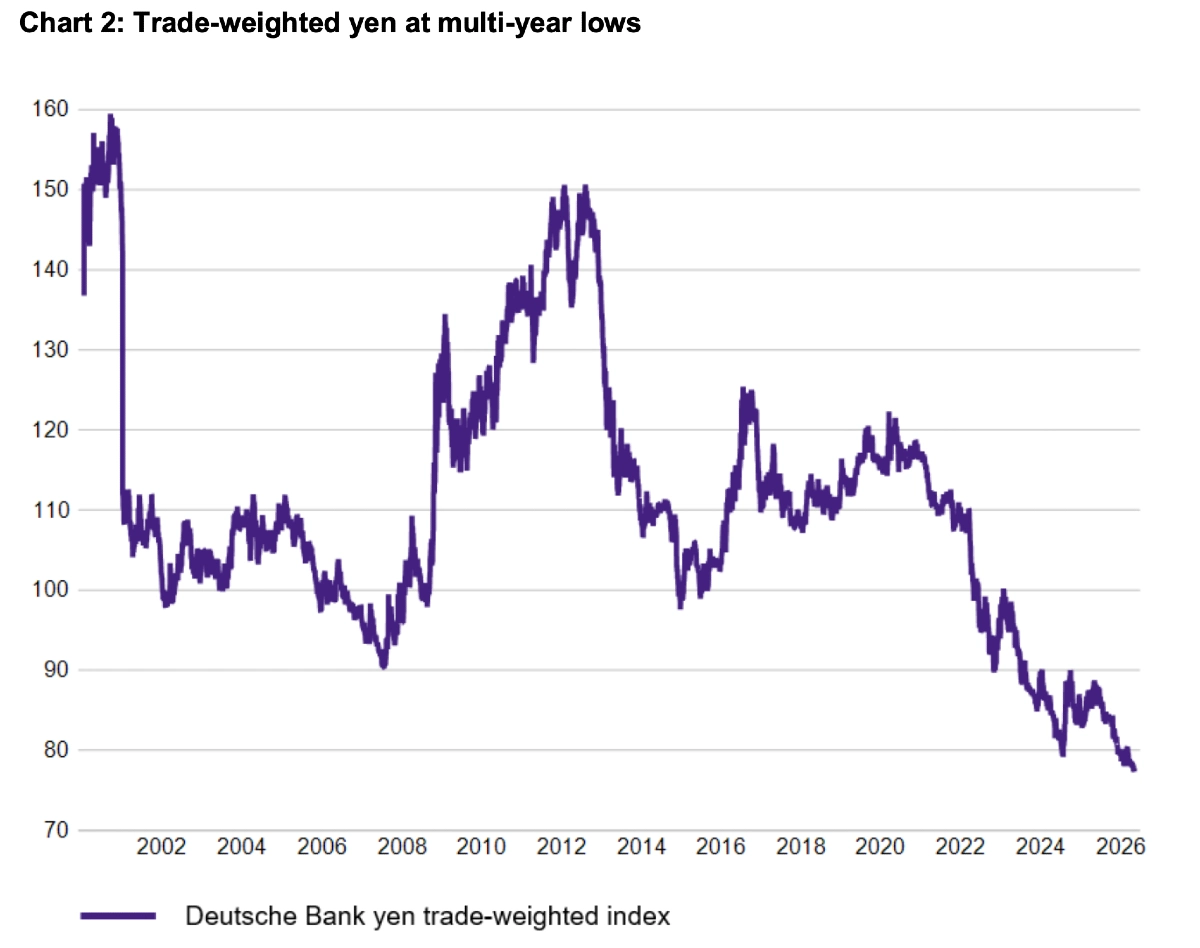

Persistent yen weakness has been acting as an inflation amplifier—magnifying Japan’s terms-of-trade shock—since before the Iran conflict, as mentioned in the BOJ’s latest policy statement. The yen remains near historical troughs versus the dollar, while in trade-weighted terms the currency has also hit multi-decade lows (see Chart 2).

The risk of currency market intervention is reported to be rising, with the Ministry of Finance warning that it is prepared to act. However, official intervention has historically served to limit short-term volatility rather than to reverse prevailing currency trends.

Secondary inflation pass-through: still contained, but for how long?

Inflation expectations are only starting to rise, as evidenced by corporates’ reported cost pressures and intentions to pass these through. This may afford the BOJ some flexibility on the timing of further policy action, but possibly less so when it comes to maintaining policy credibility. Even if the BOJ remains on hold at its April meeting as the markets expect, it would be rational for policymakers to significantly raise inflation forecasts (1.9% in the most recent Outlook) in their Outlook Report for the current fiscal year.