The Japanese stock market has been the best performing of the major stock markets in the first half of this year (to June 30) and is now in its fourth year in a row of delivering investors double digit growth, says Asset Management One International (AMOI), part of one of Japan’s largest fund managers with $495 billion in assets under management.

In the first half of this year (to close of June 30), Japan’s Topix is up 14.9% in comparison the US’ S&P 500 up 9.3%, the FTSE 100 is up 5.5% and Europe’s Euro Stoxx 50 is up 8.2%.

AMOI says that the stock market growth has been underpinned by unprecedented improvement in profits and corporate turnover.

- Average profit margins for Japanese companies are up 40% from 5.8% five years ago to 8.1% now. Profit margins are now the highest since at least 1985 (the earliest year for which data is available)*

- Operating profits are up by 66% in the last five years from 19 trillion yen to 31.5 trillion yen (year end Dec 31 2025)*

- Sales are up by 20% in the last five years increasing from 324.6 trillion yen in 2020 to 389.5 trillion yen in 2025*

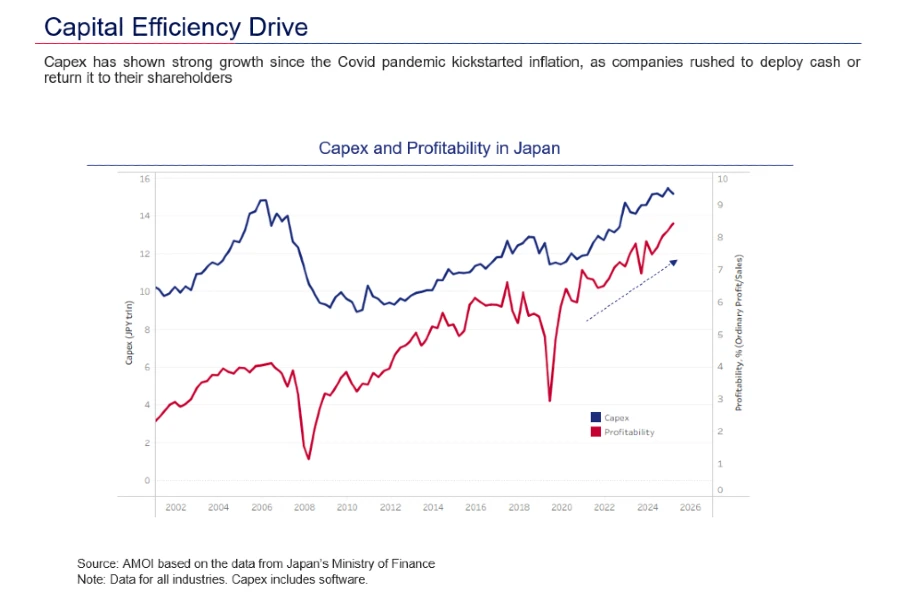

- CAPEX, which has helped to spur Japan’s improved profitability, is up by 37% in the last five year from 11.4 trillion yen to 15.6 trillion yen in the last year*

Japan has been through a virtuous circle that started when Japan’s decades-long deflationary period finally ended. Price rises led to increased corporate sales which created room for higher wages. That improved household income has supported consumption.

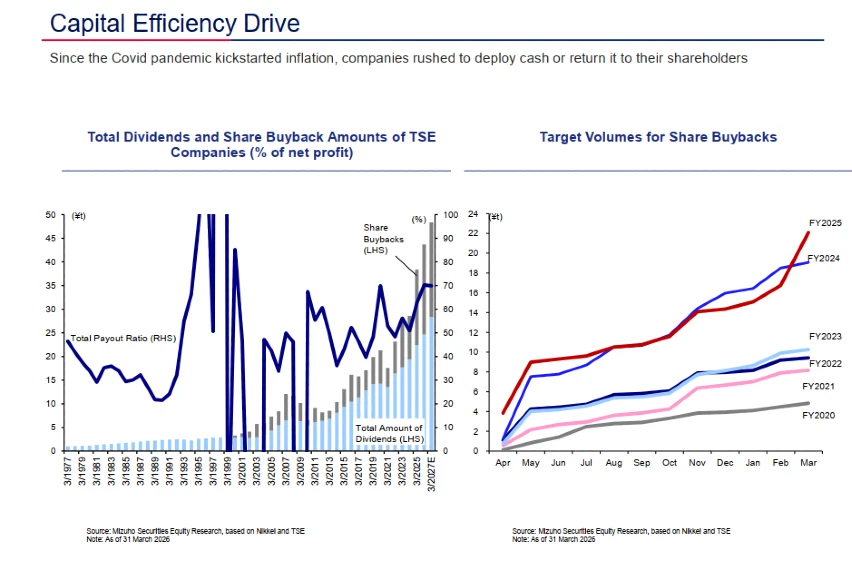

Corporate governance reforms have also helped to translate the improved business conditions into better corporate profits. The improved CAPEX of Japanese companies has partly been stimulated by the firms having to either return cash to shareholders or invest it – rather than just having that cash sit on their balance sheets. Corporate governance reforms have also encouraged Japanese companies to be much more selective about their investment plans and ensure their returns deliver economic value.

Japan’s corporate governance reforms have also ensured that the improved profits have been returned to shareholders through a massively expanded programme of share buybacks and dividend increases. For example:

- Share buybacks have increased by 250% from 5.1trillion yen in 2020 to 17.8 trillion yen in 2025** (year to Dec 31)

The net result of the improvements of higher profitability and corporate governance reforms is that the many healthy Japanese companies whose shares were trading at a substantial discount to their book value have seen that discount narrow as domestic and foreign investors have become more active buyers.

Asset Management One’s Japan Value Fund, for example, has outperformed the broader Japanese market by a significant margin delivering returns of 21.7% in the year to date*** versus 18.6% for the Topix TR (Total Return) in the same period. Past performance is not a reliable indicator of future results.

Oleg Kapinos, Head of Global Distribution Strategy at Asset Management One International explains: “Strong fundamentals have propelled the market upwards, taking some of the low-valuation stocks with it. But for active investors like us, it is the persistent pockets of inefficiency that continue to present attractive investment opportunities. As long as we keep finding businesses where we believe the stock price is lower than the company’s intrinsic value, we will have abundant options for investment.”

*Asset Management One

** QUICK, Bank of America

***As of June 30, AMO Japan Value Equity Portfolio Class I JPY Acc. Performance is in local currency