In the latest edition of the quarterly newsletter ‘The Future Strategist’, Mark Hawtin and the Liontrust Global Equities team share their market outlook for the coming quarter as well as their take on a range of topical issues.

The first quarter of 2026 has delivered two key change drivers that clearly impact the outlook and the way we are looking at investment positioning from here.

The first is the impact of the Iran war that has driven up energy prices and thus potential inflation numbers. This in turn has lowered the likelihood of rate cuts on the scale that was foreseen at the start of the year. This acts as a drag on growth and the discount rates applied to growth equities in particular.

The second factor is the dynamic shift in perception of AI winners and losers, and the software impact witnessed in the first quarter. Looking at the Goldman Sachs thematic baskets, Expensive Software fell 22% in the first quarter while Capex Beneficiaries rose 16%. The Mega Cap basket fell 10%, highlighting that rotation has been severe compared to previous periods. In short, it was hard to make progress in equities without owning hardware and AI-related capex names.

This trend is likely to continue into the second quarter, and the revenue from all this capex spending is starting to deliver meaningful revenues. We see this as an opportunity to expand the horizon of names that will directly benefit from the spending to include the key hyperscalers, Amazon and Google in particular.

In addition, we remain positive on bottleneck supply chain names like memory and hard disk drives while avoiding the most frothy parts of the theme such as optical networking. If there is anywhere that bears some resemblance to 2000, it is probably here. Cienna was around in the dotcom boom/bust. It traded at $37 in 1998, peaked at over $1,000 in 2000 and by October of that year was trading at around $20!

The shares did little for the next 25 years, but a new ramp has kicked in. From a share price of around $50 in 2025, the shares have jumped 10 times to trade close to $500. What are the chances of another year like 2000 in this sub-segment of the market?

Software remains a difficult area for investment with our proprietary technical system flagging most names as sell/avoid. The debate will rage for a long time over the disruptive nature of AI to the traditional software industry. It is likely that the final outcome will sit in between those who say this is Software 2.0 and nothing survives from the SaaS (Software as a Service) era and those that think the moats existing today are sufficient to protect large scale software names. Getting the investment strategy right in this sector, as well as related names that have been sold aggressively, will matter as the year goes on.

Outside the tech space, we continue to promote diversification. The structural trend for the US dollar is likely to be lower and this favours emerging markets. This also supports non-US dollar investors taking advantage of likely currency tailwinds outside the US.

We do not believe that the gold trade is over yet. There is still a great deal of uncertainty in the world, and this asset class provides good diversification. The gold miners in particular still trade at significant discounts to the gold price itself, and we continue to like these names as portfolio diversifiers.

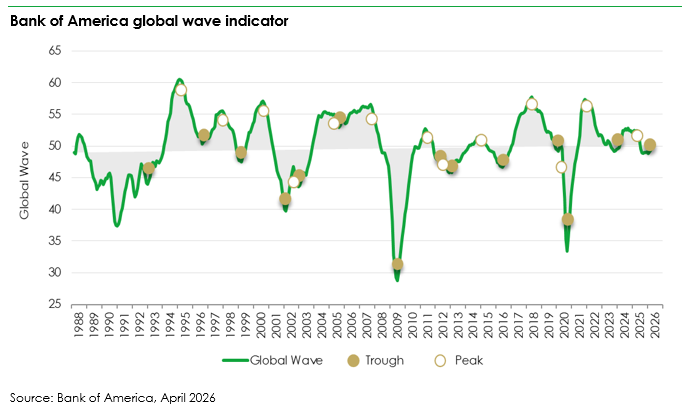

Economic data around the world have remained robust for now and this is supportive of equities. The Bank of America global wave indicator has turned positive, reflecting the strengthening of economic conditions, and traditionally this has been a good lead indicator for equity performance.

Following previous trough signals in the wave, the MSCI World index median performance over the following 12 months has been +16.5%, with emerging markets and Europe leading from a geographical perspective, which is again in line with our thinking on diversification. There are also clearly significant cash resources on the sidelines to buy the dip. We remain constructive overall, but with diversification as the price to pay for managing risk effectively.

Past performance is not a guide to future performance. The value of an investment and the income generated from it can fall as well as rise and is not guaranteed. You may get back less than you originally invested.