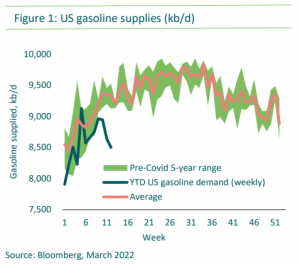

Looking at weekly gasoline demand data from the US, it’s possible that we are starting to see the beginnings of demand destruction there as well.

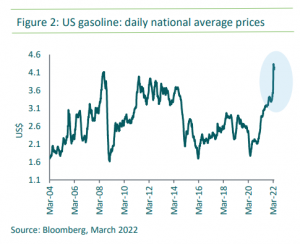

In Figure 1 below, the green shaded area represents the pre-covid five-year range and the pink line the average. Year-to-date US gasoline demand is represented by the dark blue line, where we’ve begun to see a downward trend as gasoline prices have risen in recent weeks – above the peak prices reached in mid-2008 (Figure 2).

If the conflict persists, energy prices are likely to remain elevated, further eating into consumers’ incomes. The announcement of a further release of US oil reserves on 31 March may have a short-term impact on oil prices but it is unlikely to have a longer-term impact given the temporary nature of the supply. The two attempts at releasing strategic reserves over the past year have not had sustained success in lowering prices which, instead, are reacting to high global demand, supply disruptions, low inventories, and limited supply additions. While the Biden administration is encouraging the US shale industry to drill more, it takes a long time to physically bring production onstream. It should eventually lead to a production boost, but it’s unlikely that higher US supply will come on stream before 4Q 2022.

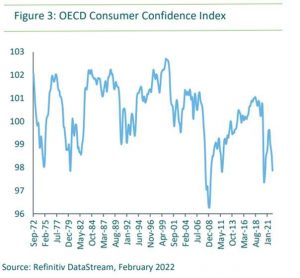

At an aggregate level, the OECD Consumer Confidence Index had already been tracking lower since the middle of last year as COVID-related fiscal support began to unwind and macroeconomic uncertainty ticked up. We would expect the decline to continue.

On the other hand, a near-term resolution to the war in Ukraine could reverse some of the inflationary pressure and also bring some relief to global markets. Yet, we need to define what ‘resolution’ means, as an improvement from the point of view of the intensity of the conflict – which is clearly very much hoped for from a humanitarian perspective – would not necessarily lead to an immediate lifting of sanctions.