The Fed’s freedom to print money at will, in all probability, shall be soon tested. And with it, the cornerstone of the last twelve year’s financial paradigm.

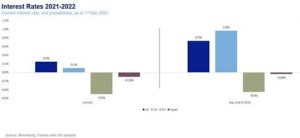

For one, with inflation that high and wage pressures exacerbating and eating into corporate margins, the Fed’s compulsion to raise interest rates, i.e. make money more expensive, is growing. QE, which in essence makes money cheaper can’t really exist in a rate hike cycle. Next year will feature a more hawkish Fed, so these sorts of decisions will be made easier.

To be sure, raising interest rates and stopping QE has more of a psychological effect than a real one. Inflation, not rates influence consumer behaviour. Rates are a signal that ‘we are doing something about it’. The signal is politically expedient and might serve the purposes of policy makers across all branches of government, especially during a mid-term election year for the US. But raising the cost of money in the US by a fraction does very little to speed up the production and transferring of goods from Asia. Demand driving orders is not the result of credit-induced exuberance but rather panic, as wholesalers and retailers are running short on everything as a new Covid-19 variant becomes dominant. So, in all probability, no matter what the Fed does, this bout of supply-side inflation will remain firmly outside its control.

What does this mean for investors?

In the coming investment committee, we will fully assess the rise of risks against valuations and market momentum. The Fed’s ability and willingness to suppress any sort of equity and bond market risk in the last twelve years is, at the very least, compromised by surging inflation. However, we don’t believe there’s sufficient reason to panic.

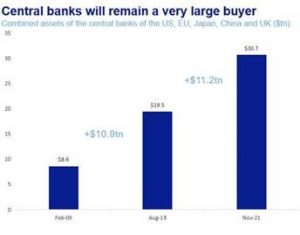

For one, there’s still plenty of money in the system. Since September 2019, the Fed’s balance sheet went from $3.7tr (already considered a huge balance sheet), to $8.6tn. A 130% rise in two years, which added another $4.9tn to the global financial system. More than $10tn has been added by the four major central banks (US, EU, China and Japan). For investors, that huge liquidity pool constitutes the most potent financial safety net in history. It will take years for that money to be fully integrated into the financial system. Fiscal stimulus in the US and China ensure more money for the real economy. So does the almost $2tn in Private Equity dry powder.

And, overall, money will remain cheap. Raising interest rates 1% or so sends the message but does not make money materially more expensive. If central banks really believed that this sort of inflation could be fought with higher rates, then we would already be experiencing a 7% interest rate. With global Debt-to-GDP skyrocketing to 356% over the past two years, government debt-to-GDP over 110% for many developed markets, and fiscal easing on the way, materially raising the cost of capital is simply not an option.