But what about QE?

We have to accept that QE’s use was also, mostly, psychological. Short term market operations might still be used to bail markets out of trouble. But with inflation running that high, adding trillions of long-term money into the system within the space of months at first whiff of market distress, is probably out of the question, even if it’s just for politics.

Should investors be worried?

Equity investors should get used to more volatility, and may well experience an equity re-rating and lower valuations in the next few months. This is more so for funds heavily exposed in tech, where valuations have risen disproportionately to the rest of the market. Focusing on fundamentals and being selective about managers will go a long way into preserving wealth.

Bond investors will have a more difficult time. High liquidity gives hope to traders that they might still find someone to take their holdings out of their hands at an even higher price. But the bulk of fixed income investors, who tend to hold the asset to maturity, are in trouble. Either they will lose a steady stream of money in real terms over the next few years, or they will experience a sharp correction in prices. Real returns (yield minus inflation) are deep into negative territory. Assuming 3% average inflation over the next five years, an investor in the five-year US Treasury note yielding 1.27% would experience an assured loss of 1.75% per annum, or 8.5% of their overall investment in real terms. Because no market can operate under an assured loss assumption, the probability for a sharp price correction (so that annual yields may rise) is climbing fast. Central banks will still remain a big buyer of debt, but adding no new money into the system would allow yields to drift upwards. We are already deeply underweight bonds and considering ways to mitigate the impact of a possible re-rating event on those that we do hold.

Why the case for remaining invested still stands

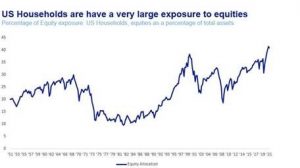

The end of QE and the end of the current paradigm, however, is not a disaster. The money already printed is not going anywhere and it can continue to fuel markets for a long time. And QE’s withdrawal will be handled with care. Inflation may be catastrophic in an election year, but so is a market rout, with US households having a record 41% of their total assets in equities.

It may even prove a blessing in disguise, as it could return long-gone sanity to investment markets. To be sure, a post-QE and post-rerating world, is a different, more volatile, world. Volatility may be uncomfortable, but it is the mother of opportunity. Investors will see traditional strategies, like the 60/40 equity/bond portfolio, working again. Overall, this should reduce risks, or at the very least, make them more manageable. Shorting markets may, on occasion, pay off as a strategy. Shorting capitalism over the longer term, never does. And while we expect a tantrum, or more than one, we believe financial markets will outgrow QE, much like humans do: by learning, sometimes the hard way, that even if things occasionally go south, is not the end of the world.