Alicia Garcia Herrero, Chief Economist for Asia Pacific at Natixis CIB, has examined the economic implications of the escalating Iran conflict for Gulf economies and global energy markets.

Iran’s attacks have caused notable disruption to energy infrastructure around the Persian Gulf and led to an effective closure of the Strait of Hormuz. This imposes great downside risk on the Gulf Cooperation Council (GCC) countries who are heavily reliant on oil revenue. That said, countries with alternative routes that are less disrupted, such as Saudi Arabia and UAE may find some respite from the elevated oil prices.

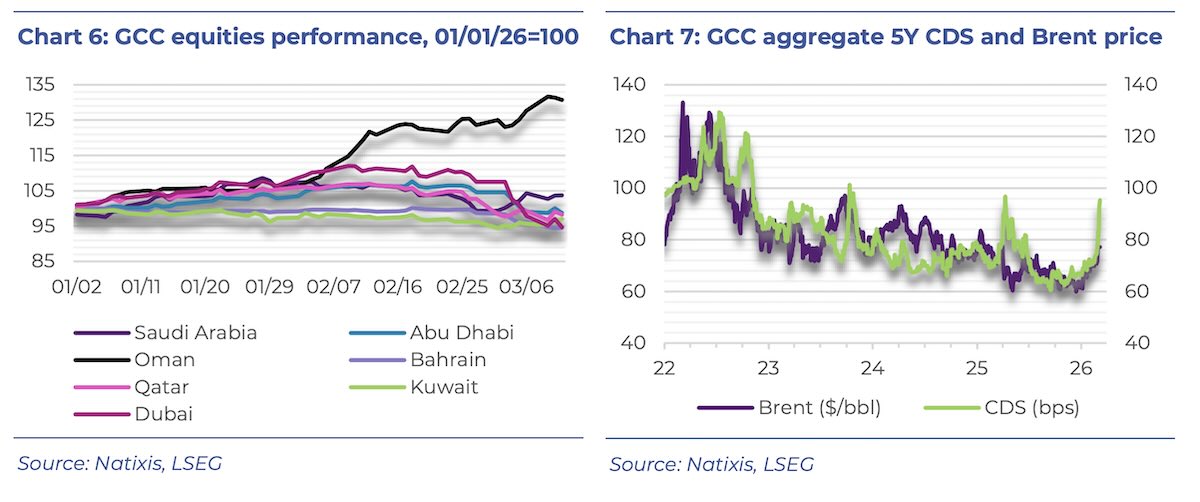

Financial markets reacted negatively to the attacks but have recovered partially, albeit still in an uneven way, with the UAE lagging Saudi. As regards government and corporate bonds, spreads widened but relatively moderately, and so did CDS. For example, 5-year CDS rose by only 20bps. This reflects GCC countries’ strong financial buffers with massive sovereign wealth funds and limited debt, generally.

A few immediate negative effects on the economy are worth highlighting. Firstly, the spike in oil prices might not be enough to compensate for the production shut-in due to lack of storage facilities. This will depend on the duration of the closure of the Strait of Hormuz and demand for oil, which hinges on the resilience of global economy, central bank reactions to the pass-through inflation as well as demand destruction in countries with limited oil reserves.

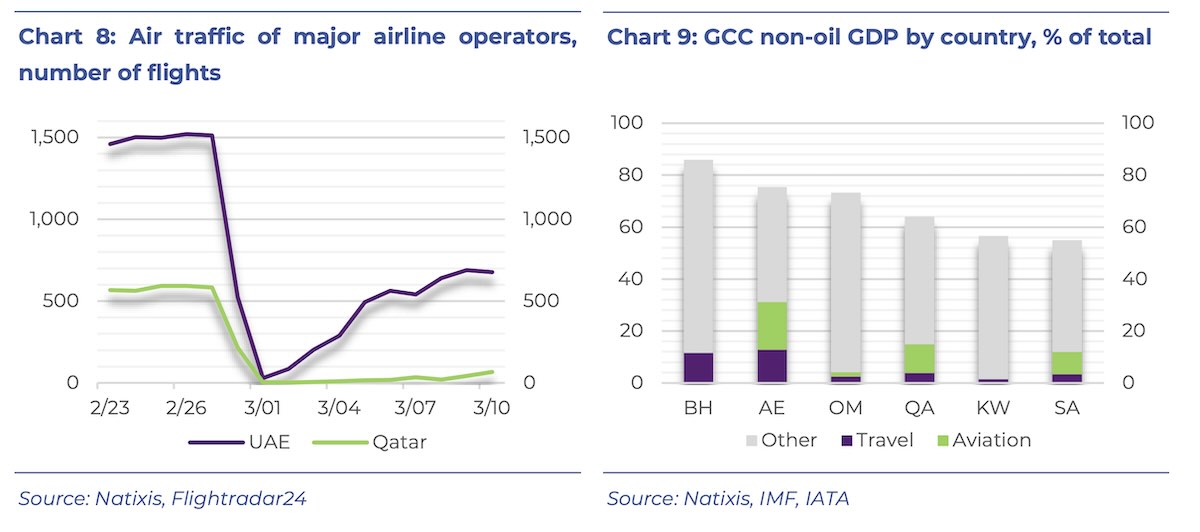

Beyond oil, those economies which are more diversified, especially the UAE, are also taking a hit due to the shock to tourism and the aviation sector. Air traffic collapsed following the first round of attacks and hasn’t fully recovered as of late, with UAE airlines operating at 45% of pre-conflict levels, while Qatar remains low at 11%.

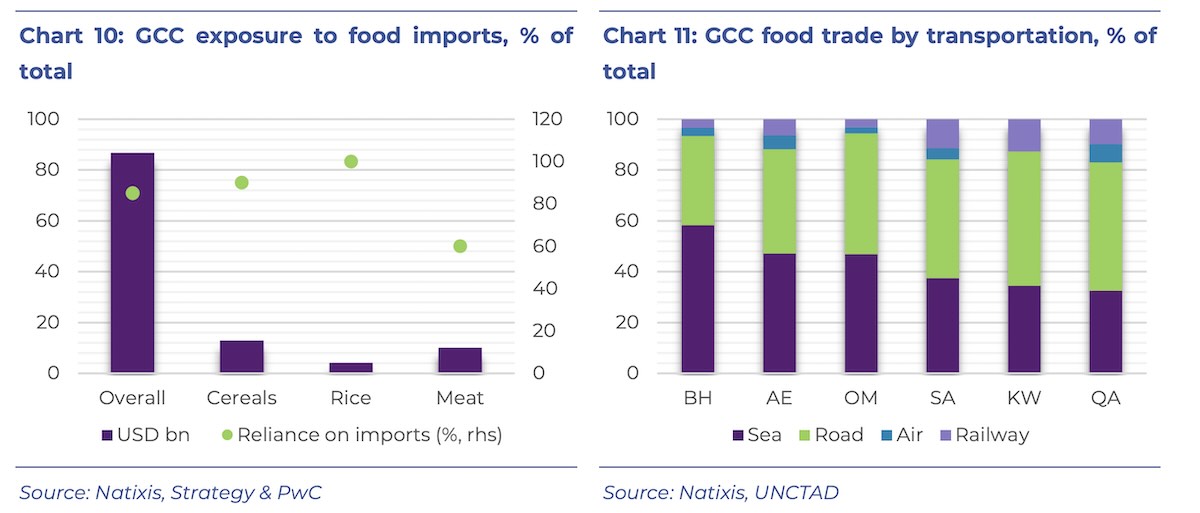

Finally, given the high reliance on food imports (85% in 2019), there have been worries about food shortages. However, data shows 43% of food imports are transported by sea, where 30% of them transit via the Strait of Hormuz, meaning the GCC’s exposure is around 13%, which is rather moderate. Moreover, the rerouting and substitution of food imports may benefit regional logistics hubs such as Saudi and UAE.

Looking ahead, the conflict may have important consequences for the region in terms of their attractiveness but also on their quest for diversification, which will only press on even beyond tourism and aviation.FDI inflows have been accelerating and supporting the non-oil economy since 2015,but this could change if the conflict is protracted.

On the other hand, the link between the Middle East and Asia could continue to strengthen, especially if the US were to abandon the region abruptly, with a possible new wave of strategic agreements. All in all, what is clear is that it is too early to tell, and more clarity is needed as to the duration of the shock as well as how we exit from this impasse.

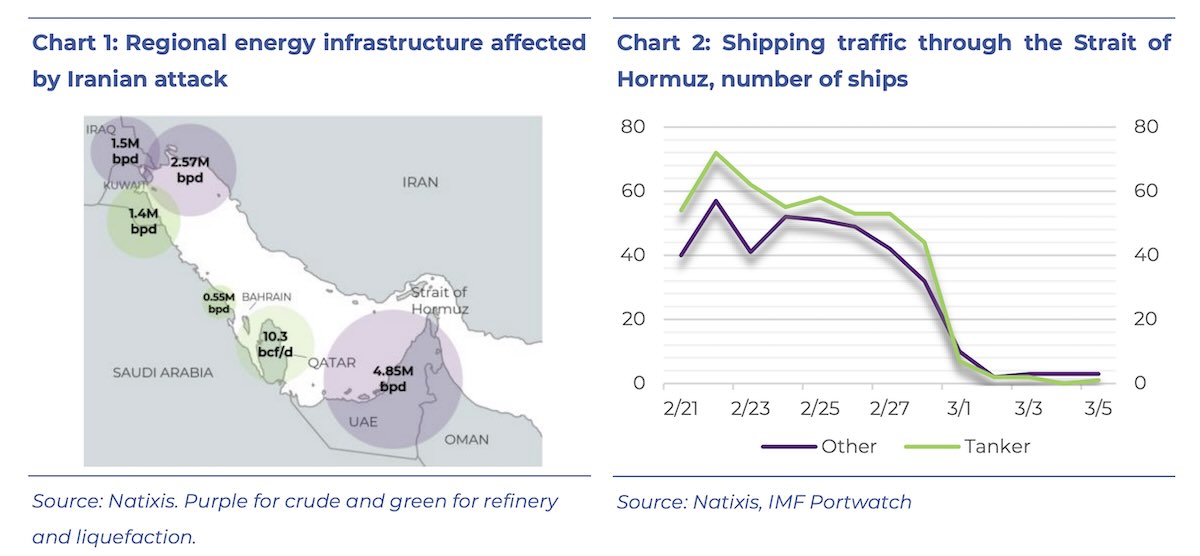

Since the US and Israel’s joint strikeon February 28, Iran has launched aggressive attacks against not only US military bases but also energy infrastructure in the region, causing notable disruption to the Gulf countries’ production and exports of energy.

Qatar shut its largest natural gas liquefaction facility in Ras Laffan on March 2, followed by Saudi Arabia, which halted its largest refinery in Ras Tanura after reporting a drone attack (Chart 1). As the Strait of Hormuz has been effectively closed since March 2, energy storage facilities are running out, which has forced a total reduction of 6.7 million barrelsper day(mb/d)by Saudi, UAE, Kuwait and Iraq as of March 10 (Chart 2).

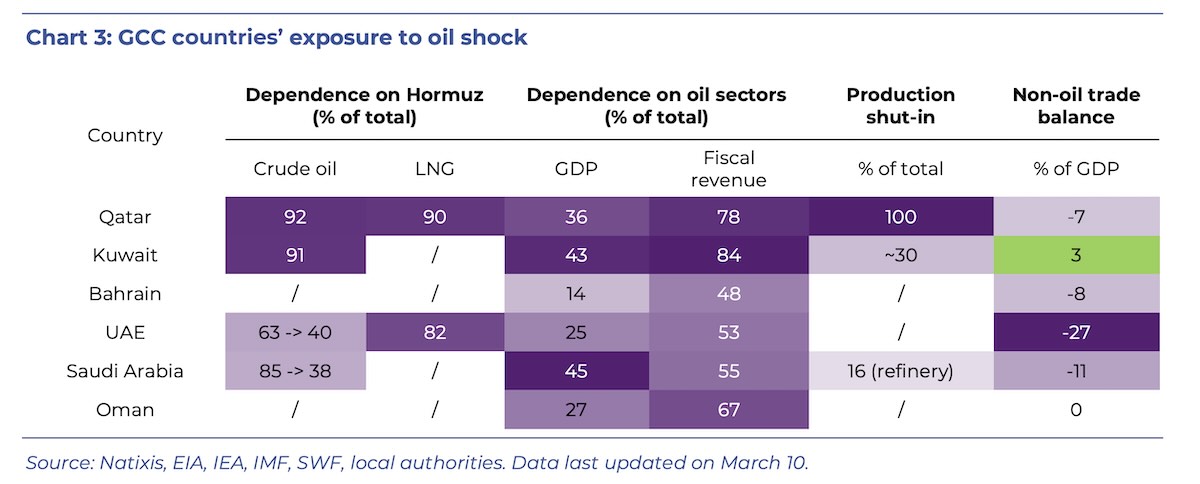

This has undoubtedly imposed great downside risk on Gulf Cooperation Council (GCC) countries, which are heavily reliant on oil revenue not only as a major part of their economy but also as a key source of government funding (Chart 3).

Qatar and Kuwait are taking the brunt due to a lack of alternative routes and high fiscal dependence on oil. Saudi Arabia is also heavily reliant on oil revenue from this transit chokepoint, but its exposure is mitigated by the cross-peninsula pipeline, which can move 5-7mb/d from the Persian Gulf to the Red Sea.

As of March 11, the IEA has agreed on a joint release of Strategic Petroleum Reserves (SPR), which is expected to supply an extra 4.4-6.5 mb/d depending on the timeframe (2 to 3 months). However, this is just a painkiller as the net outage is estimated at ~10 mb/d. The speed and distribution of the SPR release are also in question as the size is unprecedented (yet still not enough).

As such, the key determinant of oil prices remains the duration of blockage, on which the oil market is firming up a new price floor of $90/b in a scenario of 3-4 weeks’ disruption. However, should there be further escalation or protraction, the oil marketmay move towards higher levels, and we expect Brent to reach $125/b in April if the outage lasts for 3 months (Chart 4).

In that case, some GCC countries with sustained shipping routes, such as Saudi, UAE and Oman, could benefit from the elevated prices and partially offset the loss of volume (Chart 5). That said, it will need more time to ascertain the net effect as global oil demand could further sag if central banks pull the trigger to press down pass-through inflation and demand destruction materialises in countries with limited oil reserves.

Financial markets reacted differently to the attacks with Oman being an obvious hedge (Chart 6). Others have recovered partially but still in an uneven way, with UAE lagging Saudi. As regards government and corporate bonds, spreads widened but relatively moderately and so did CDS. For example, 5-year CDS rose by only 20bps (Chart 7). This reflects GCC countries’ strong financial buffers with massive sovereign wealth funds and limited debt generally.

Except for direct shock on oil sectors, non-oil sectors, especially travel and aviation, are also taking a hit. The regional air traffic had sharply fallen due to airspace closure following Iran’s attack on Feb 28 and not yet fully recovered as of late (Chart 8). UAE airlines are restored to 45% of their pre-conflict level while Qatar Airways remains largely disrupted, operating only 11% of capacity. Security concerns also discourage regional and global travellers, weighing further on travelling hubs like the UAE, Qatar and Saudi Arabia (Chart 9).

Moreover, given the arid climate, the Gulf countries have a high reliance on food imports which stoodat 85% in 2019with nearly 100% for rice and 90% for cereals (Chart 10). That said, among all food imports, 43% are transported by sea where 30% of them transit via the Strait of Hormuz, meaning the GCC’s exposure to the maritime chokepoint is around 13%, which is rather moderate compared to the oil shipping.

Given that, the GCC may avoid an immediate food crisis as food security has long been a key focus in the region. However, within the bloc, Saudi Arabia and UAE may benefit from their logistical significance as other countries will seek substitute import routes which may cross their borders, especially Bahrain, Kuwait and Qatar.

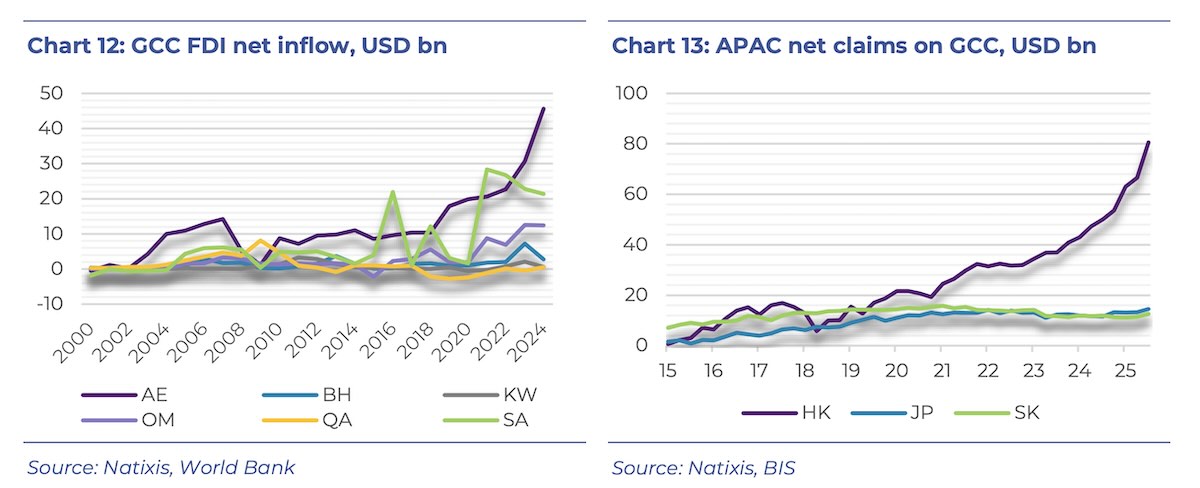

Looking ahead, the conflict may have important consequences for the region in terms of their attractiveness but also on their quest for diversification, which will only press on even beyond tourism and aviation. FDI inflows have been accelerating and supporting the non-oil economy since 2015, but this could change if the conflict is protracted(Chart 12).

On the other hand, the link between Middle East and Asia could continue to strengthen, especially if the US were to abandon the region abruptly, with a possible new wave of strategic agreements(Chart 13). All in all, what is clear is that it is too early to tell, and more clarity is needed as to the duration of the shock as well as how we exit from this impasse.