Time to buy China?

We turned cautious on China in early 2021, both for the impending rotation to countries and regions such as the US and EU which are benefitting from the vaccine rollout, as well as for tighter policies at home. China equities suffered another difficult week—this time for a crackdown on the ride sharing company Didi that had just completed an IPO. While regulatory risk still runs high, we believe that the worst of China’s underperformance over the last quarter may be behind us.

In the midst of the pandemic in 2020, prior to the rollout of vaccines, China was the clear economic winner, having effectively used lockdowns to contain the virus, while a combination of targeted stimulus and global demand for China products brought a swift return to pre-COVID-19 levels of economic activity. However, as China often does, the government used the swift recovery to reassert its reform objectives. Specifically, it tightened credit to less productive parts of the economy, including property, and imposed new regulations on technology companies that had arguably abused the privilege of their enormous size. Given the combination of fresh stimulus and the vaccine rollout that principally benefited the developed world of the West year to date, it is not surprising that flows followed better opportunities outside of China. However, as growth in the US is likely past its peak, the headwinds for China equities may begin to abate as China begins to ease policies at home.

Chart 1: Chinese credit growth

Firstly, credit growth deceleration looks to be bottoming. Having declined sharply since November 2020, as shown in Chart 1, current levels of expansion align with the government’s credit growth target, i.e. nominal GDP growth. While the credit impulse is currently negative, this is partly due to base effects of significant stimulus a year ago. Issuance of local government bonds is also expected to gather pace in 2H 2021 to make up the remaining 76% of the net issuance target, implying a boost to infrastructure investment later in the year. Also, while the government has curbed lending to speculators as with property, the government has continued to encourage credit expansion, benefiting the real economy.

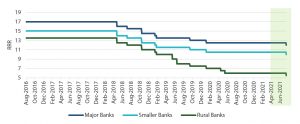

The government’s objective to supply the real economy with needed credit was confirmed last week with the cut of the reserve requirement ratio (RRR) in a broad-based manner. This is the first major easing since mid-2020, that coupled with earlier deposit rate reform is designed to ease banks’ funding pressures and should ultimately expand credit available to the real economy.

Chart 2: China RRR cut

In its efforts to expand credit, the government remains targeted, aiming to direct resources to new economic sectors such as 5G, IoT, AI and advanced manufacturing, which are critical to unlock potential growth and strengthen self-sufficiency. As always, it is a balancing act, redirecting capital away from inefficient use to where it is most needed to grow the real economy, while in the process not inflicting too much economic pain to any one sector.

In addition to stabilising credit that should ease concerns for slowing growth, we also believe regulatory crackdown is at or close to its peak, which should ease concerns for regulatory risk. Of course, many investors will not immediately see it this way given the harsh punishment of Didi early in July, just two days after its US IPO.

The regulatory campaign began in November 2020 when the Ant IPO was suspended to bring tighter controls to the fintech sector. In April this year, Alibaba was issued a hefty fine, albeit one that was ultimately seen by the market as light relative to its revenues. In essence, the regulatory campaign seemed methodical and fair, achieving reasonable government objectives while not bringing undue pain to the tech sector that is still vital in supporting the new economy and jobs growth.

However, the recent harsh punishment of Didi sent new shockwaves across the tech sector. This was exacerbated days later when authorities announced new rules governing tech listings overseas. Still, the recent shakeup does not appear out of scope from the government’s reasonable objectives, so it may be that Didi will mark the peak of regulatory concerns.

China equities could also benefit from the rotation back to growth and tech as the reflation trade loses steam on the back of growth passing its peak, while yield curves continue to flatten. China tech stocks trade at an attractive discount compared to US peers, and if regulatory risk is indeed peaking, it could pose an attractive opportunity, in our view. China’s recent efforts to support credit expansion in favour of the real economy is also a positive inflection point that should avert fears of a deeper slowdown with promises of stronger demand ahead.

Conviction views on growth assets

- Cautious on EM, for now: We turned more cautious on both EM equities and debt, due to the return of dollar strength coupled with weakness in commodity prices and inflation expectations. We also note the China credit impulse shifting negative and the likely downsizing of the US infrastructure stimulus. Of course, EM is still lagging DM peers in terms of the vaccine rollout, and now the rise of the Delta variant is likely to weigh on re-opening efforts as well. That said, we think EM assets are still attractive, mainly showing better value where we seek targeted opportunities.

- Barbelled exposure to equities: We continue to believe that a balance between secular growth and opportunistic value is the best means of positioning in the current environment. We like the re-opening play still and favour quality opportunities that are still showing value are the best means of participating in this upside. Still, opportunities in secular growth areas such as US and North Asia tech are still compelling from a strong earnings growth and cash flow perspective.