Defensive assets

Our view on defensive assets improved again this month but we retain a cautious approach over the medium term. Recent central bank meetings were closely watched for any signs that officials were ready to discuss plans to reduce quantitative easing (QE) purchases, and eventually raise cash rates. While many viewed the Fed as coming closest through changes to its “dot plot”, indicating that the median forecast for the first rate increase was brought forward to 2023, these forecasts have been of questionable value in the past. This was a point that Fed Chairman Jerome Powell made in his post-meeting press conference, and ultimately, the Fed kept its accommodative settings unchanged. The European Central Bank (ECB) also disappointed bond bears as it repeated its dovish message of accelerated QE purchases. With policy changes seemingly several months away, we are still more constructive on global bonds.

Global credit spreads were stable over the month, but lower benchmark US Treasury (UST) yields helped deliver positive returns. Most developed countries have made substantial progress in their vaccination programmes after slow starts, and the global economy is rapidly recovering lost output as the worst of the pandemic recedes. Ongoing fiscal and monetary support are also contributing to an environment of improving credit quality that is supportive of our positive view on IG credit.

Real yields remain sharply negative even as the world’s developed economies continue to reflate. This holding pattern is likely to continue in the near term as markets continue to assess incoming inflation data for evidence of transitory versus persistent price pressures. While negative real yields are generally positive for gold, the precious metal has nevertheless been under pressure from US dollar strength and technical selling. History also tells us that gold prices are likely to trend lower ahead of any formal announcement of QE tapering, as they did back in 2013. These factors combine for a weaker climate for gold and we have turned a little negative on the near-term fortunes of traditional inflation-hedging assets.

Tale of the taper

The world’s major central banks have undoubtedly been providing extraordinary support for the global economy throughout the pandemic by using massive QE programmes and near-zero or negative official cash rates. As the pandemic starts to recede for several developed countries, intense focus is now directed at any signs of upcoming changes to these policies. Forward guidance has been consistent across central banks in holding cash rates at current low levels well into the future, with any changes only coming after QE programmes are ended. The current landscape of QE programmes for the major DM central banks is shown in Chart 3.

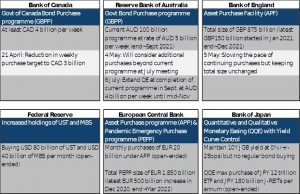

Chart 3: Major central bank quantitative easing programmes

Earlier this year in our March Multi-Asset monthly, we assessed the relative commitment of these six central banks to prolonging their QE programmes. At that time, we considered that both the ECB and the Bank of Japan would likely hold on to their QE policies the longest and that the Bank of Canada (BOC), Reserve Bank of Australia (RBA) and Bank of England (BOE) would be the first to taper asset purchases. We perceived the Fed to lie somewhere in between these two groups.

In recent months, our perceptions have begun to translate to actions as the most likely central banks have begun to announce QE tapering plans. The BOC was the first to move in April, announcing a reduction in its weekly purchase target from Canadian dollar (CAD) 4 billion to CAD 3 billion. This was followed by the RBA, most recently announcing that it would slow purchases from its current pace of Australian dollar (AUD) 5 billion per week to AUD 4 billion when the current programme was expected to expire in September, effectively prolonging QE until at least November. And arguably, the BOE could also be included in these first movers after announcing in May that it would slow the pace of its purchases even though the size of its program remained unchanged.

The Fed’s plans for QE, however, are of most interest to the greatest number of market participants. At its June meeting it confirmed that the Committee had begun to “talk about talking about” tapering its asset purchases. The next two reference points are likely to be the next Federal Open Market Committee (FOMC) meeting in late July and the Jackson Hole Economic Symposium in late August. We expect that the FOMC will begin discussing tapering scenarios at its next meeting, but that any details will have to wait until August at the earliest. It is a close call in our view whether actual tapering begins in December or January next year.

While all of this speculation around tapering is interesting, and maybe even entertaining for some, the near-term and longer-term implications of eventual tapering are very different. In the near term, central banks continue to buy large quantities of government bonds at sharply negative real yields. This significant buying continues to be problematic for investors and speculators that had reduced sovereign bond holdings earlier this year in anticipation of reduced QE purchases. This short positioning is being pressured in the near term by the relentless buying activity of central banks. However, in the longer term the tapering of official purchases will require greater participation from other investors. This will again become problematic, but in a different direction, as the same sharply negative real yields that have not deterred central banks will be deemed unattractive by other investors, leading to another potentially sharp reversal towards higher and steeper yield curves.

Conviction views on defensive assets

- IG credit still offers attractive carry: High grade credit spreads are historically tight, but credit quality continues to improve, and the extra yield should be maintained in this environment.

Process

In-house research to understand the key drivers of return: