Over a decade on from the launch of Shinzo Abe’s economic reforms, Japan is presenting fantastic valuations with rewards for stockpickers prepared to do their homework, argues Rob Perrone at Orbis Investments.

A lot has happened in Japan over the last 30 years. Post World War Two Japan was the ‘economic miracle’ – never before had a country industrialised and become so technologically sophisticated and wealthy so quickly. By the late 1980s this growth had developed into a huge asset bubble. The stock market hit record highs, and by some accounts the land near the Imperial Palace in Tokyo was valued more highly than all the real estate in California. In 1990, the bubble burst, and Japan suffered through two ‘lost decades’ of poor economic and stock market performance.

Japan still faces a tough economic backdrop. It has an aging and declining population and has struggled for decades with persistent deflation, while earnings growth at Japanese corporates lagged that of companies in other markets. Some of that was self-inflicted. Japanese companies have not been good at allocating capital and have tended to hoard too much cash on their balance sheets, depressing potential returns on capital. The urge to save for a rainy day is understandable in a country where earthquakes regularly wipe out whole towns, but Japanese management teams have taken this to excess. So why should investors consider investing Japan?

Firstly, Japanese companies are improving their capital allocation. When Shinzo Abe became prime minister in 2013, he announced a three-pronged economic plan: monetary stimulus, which continues to this day, fiscal stimulus, and structural reform. For companies, this meant a new corporate governance code, a new stewardship code, new listing criteria for Japanese stock exchanges, and increased openness to activist investors.

Today, looking back over the years since Abenomics came to the fore, Japanese companies have narrowed the gap in profitability with businesses elsewhere. And—excitingly from an investor’s perspective—this improvement in profitability has not yet been reflected in the valuations of Japanese stocks. On a price to book basis, Japan trades at roughly half the valuation of other developed markets, which previously was justified because companies generated such low returns on their book values.

As profitability has improved, however, Japanese stocks are now cheap on a price to earnings basis as well. In the current environment other developed markets, particularly the US, continue to look expensive while Japan is relatively cheap. And as Japanese companies are now paying out more of the excess cash on their balance sheets, these companies also offer a higher dividend yield than shares in other developed markets.

And while Japan has been a rough environment for passive investors for the last 35 years, it has been fantastic for active stockpickers, particularly those favouring value. In fact, Japanese value stocks have outperformed growth stocks by 4% p.a. – much better than globally, where value stocks have outperformed growth by an average of around 1%. (This chart shows that) If you strip Japan out from the rest of the world, you strip out almost all the value outperformance since 1975.

The composition of the market is a big reason why value has worked so well in Japan. A third of the market cap in Japan is in capital-intensive, cyclical sectors like capital goods, autos and parts, and tech hardware. Comparatively, a third of the US market is in intangible secular growth and cyclical sectors: software, pharma, media, and e-commerce. Cyclical markets create more opportunities for people to get excessively greedy at the top of the cycle, and excessively fearful at the bottom. The greater cyclicality of Japan’s market has made it a more rewarding environment for value investing.

Bottom-up stockpicking has worked even better than a simple value style.

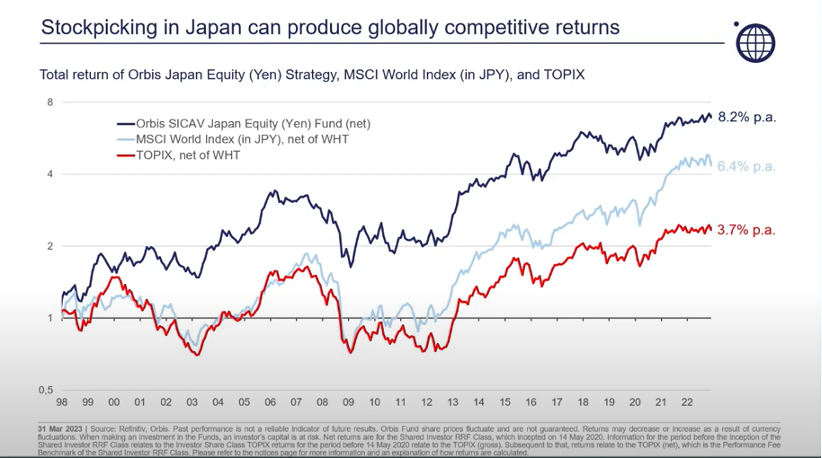

The chart below shows the returns of the Japanese market compared against MSCI World Index in Yen since 1998. While Japan as a whole has significantly lagged the rest of the world, delivering about 3.5% versus 6.5%– an actively managed Japan strategy – such as that run by Orbis, has managed to beat the MSCI World Index after fees. The opportunities within value sectors, have been there all along.

To summarise, we believe Japanese stocks remain cheap compared to elsewhere in the world, even as capital efficiency improves. A value approach has worked better in Japan than elsewhere, and active stockpicking has worked better still. Both active and passive work better when valuation spreads are wide. Today they are near the widest levels we have seen in 30 years, providing an extraordinarily attractive setup for active investors.

Orbis Japan Strategy is not available to UK Retail investors.