Lofty U.S. stock valuations call for a renewed focus on risk assessment and portfolio diversification.

As U.S. equity valuations hover near historical highs, it’s a good time for investors to evaluate the sustainability of stock gains and to revisit the fundamental benefits of portfolio diversification.

Asset prices are “elevated by many metrics right now,” Federal Reserve Chair Jerome Powell said at a 29 January policy press conference. Two days earlier, a front-page story in The Wall Street Journal, titled “Premium for Owning Stocks Vs. Bonds Disappears,” noted that the equity risk premium – defined as the gap between the S&P 500’s earnings yield and the 10-year Treasury yield – had turned negative for the first time since 2002.

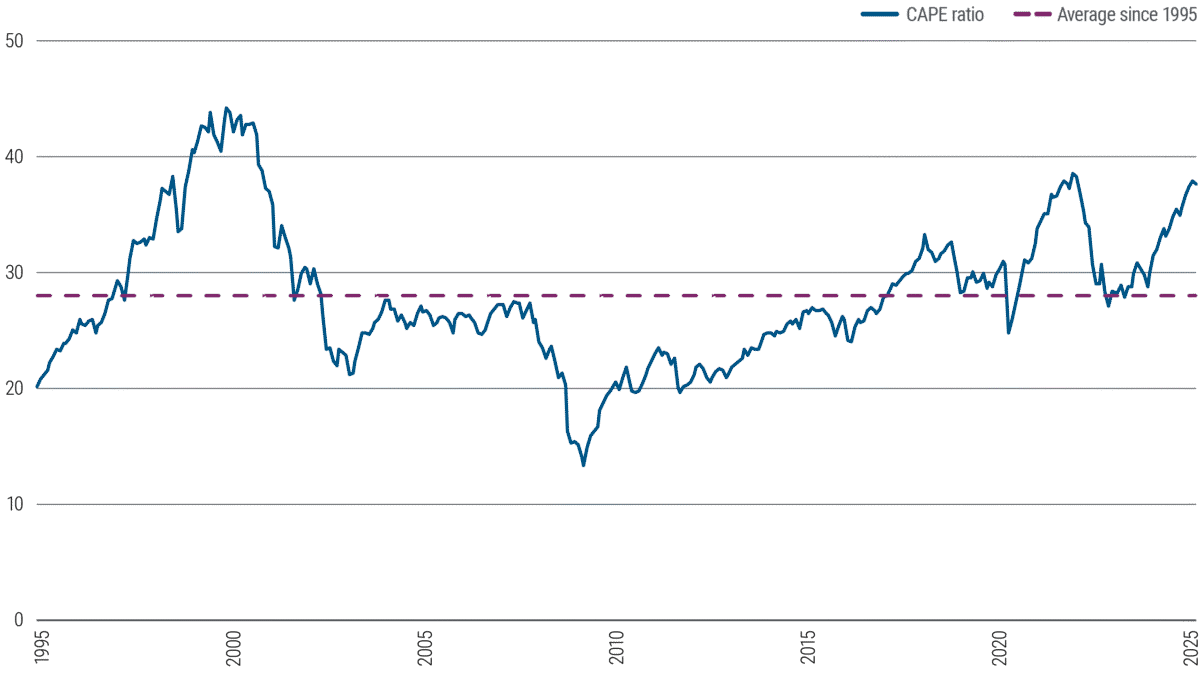

Another common equity gauge, the cyclically adjusted price-to-earnings (CAPE) ratio, has climbed to levels previously seen only twice in the past three decades: during the dot-com bubble and the post-pandemic recovery (see Figure 1). Those prior CAPE peaks occurred when Fed projections and consensus market forecasts called for U.S. growth of 3.5% to 4.7% annually. Today, however, growth is forecast to be only about 2% for 2025.

Figure 1: CAPE ratio is near peak levels

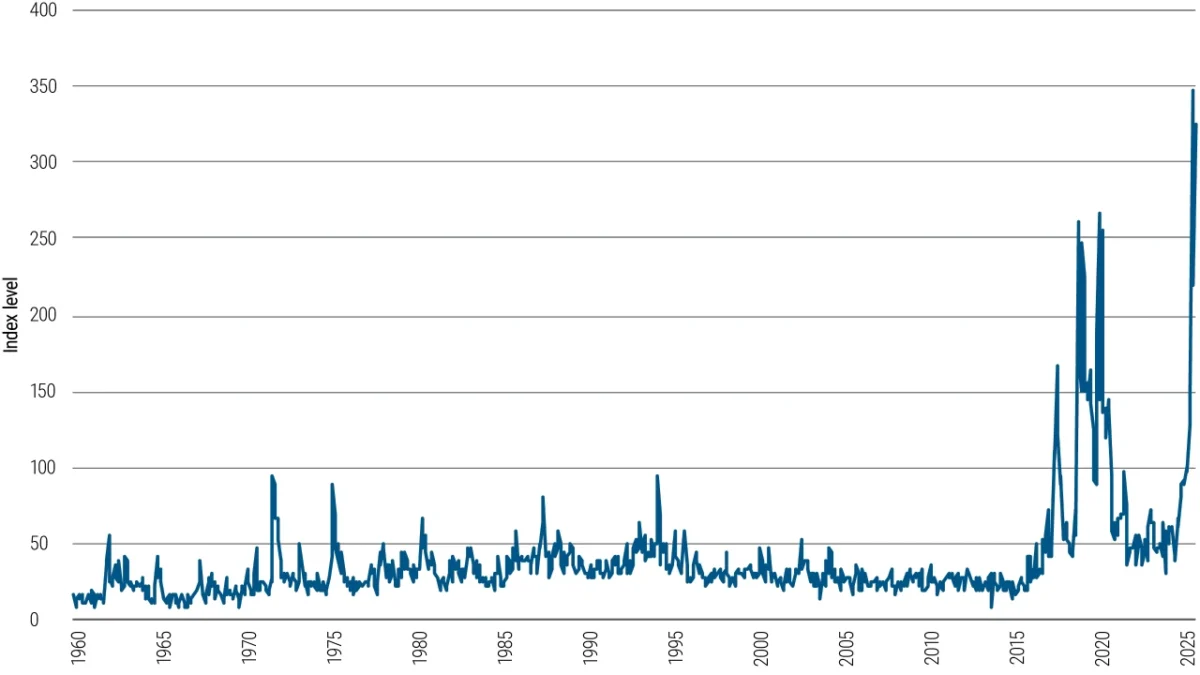

It seems especially concerning that valuations are so stretched when uncertainty is so high (see Figure 2), with U.S. tariff policies set to reshape the global economic landscape (for more, see our latest Cyclical Outlook, “Uncertainty Is Certain”).

Figure 2: Trade policy uncertainty has surged

The Trade Policy Uncertainty (TPU) Index is constructed by staff in the International Finance Division of the Federal Reserve Board and measures media attention to news related to trade policy uncertainty. The index reflects automated text-search results of the electronic archives of seven leading newspapers: Boston Globe, Chicago Tribune, Guardian, Los Angeles Times, New York Times, Wall Street Journal, and Washington Post (accessed through ProQuest Historical Newspapers and ProQuest Newsstream). The index is scaled so that 100 indicates that 1% of news articles contain references to TPU. For details on the TPU Index, see “The economic effects of trade policy uncertainty,” by Dario Caldara, Matteo Iacoviello, Patrick Molligo, Andrea Prestipino, and Andrea Raffo, Journal of Monetary Economics, Elsevier, vol. 109(C), 2020.

The case for continued U.S. stock market gains appears to rely on two key assumptions: that “this time is different,” and that U.S. economic exceptionalism – outperformance versus the rest of the world – will endure. These assumptions were tested in late January when fears about the durability of artificial intelligence investments, amid rising competition from China, sparked a sell-off. Such volatility could become more common, and a negative equity risk premium may not provide adequate compensation.

Diversification is essential

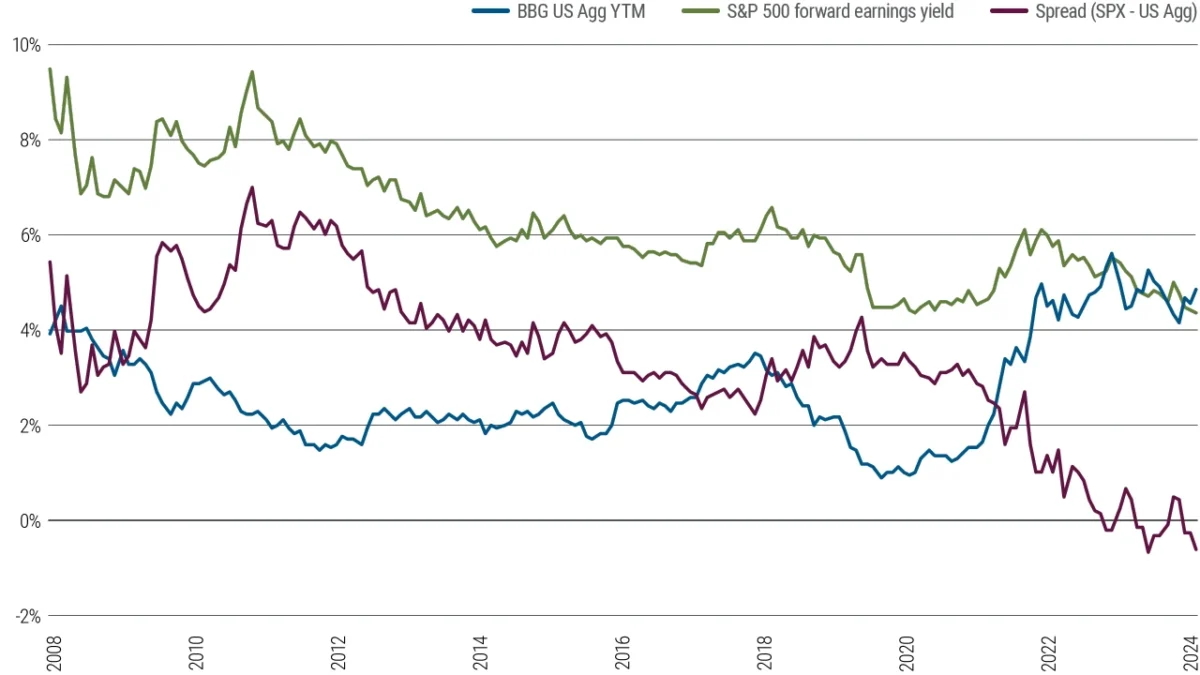

Investors should revisit a time-tested strategy: diversification. The equity risk premium has turned negative partly because bond yields have reached the most attractive levels in years (see Figure 3).

Figure 3: Bond yields have risen above S&P earnings yield

The recent reemergence of the traditional negative correlation between stocks and bonds further enhances bonds as a counterbalance to equity exposure (for more, see our November 2024 publication, “Negative Correlations, Positive Allocations”).

Over the long term, U.S. equities are essential components of any investment portfolio. Equity investments have helped power the growth of the U.S. economy while creating wealth and retirement security for millions of investors. However, periods of elevated valuations have tended to heighten shorter-term risks to the equity outlook.

As Fed Chair Powell also noted on 29 January, it’s human nature to underestimate tail risks. Following outsize stock market gains in recent years, which may have tilted portfolio allocations even further toward equities, investors should evaluate the risks related to valuations and remember the importance of bonds in a balanced portfolio. Given the historical tendency for valuations to revert to the mean, it could be a mistake to assume that today’s exceptional conditions will last indefinitely.